Explosive commercial growth ushers in a new era of the consumer experience in Shenzhen

Shenzhen(深圳), China’s first special economic zone (SEZ) founded in 1980, is one of the fastest-growing city with the highest GDP per capita[1] in 2015. Located in southern China, Shenzhen’s total sales of customer goods raked in over ¥551.3 billion in 2016, with an annual growth of 8.1%, according to the Shenzhen statistics bureau. As an important part of the retail economy, shopping malls in Shenzhen are expanding rapidly and faced with constant innovation challenges.

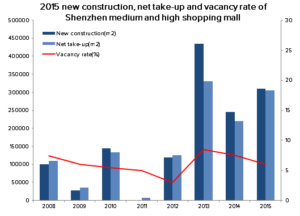

The shopping mall in Shenzhen is booming from 2013

According to Evelyn Chen, senior project manager at Daxue Consulting, after a slowdown in 2008 – 2012, construction of new medium and high-end shopping malls helped lift Shenzhen out of the slump. In 2013, Shenzhen net take-up doubled from 2012 to 2013. The vacancy rate also decreased from around 8% in 2013 to 6% in 2015.

Since 2015, over 30,000 square meters of medium and high-end shopping malls have been in construction. Thus far, that area has given rise to 14 new shopping centers as of 2016. With Shenzhen’s shopping industry showing promising growth, it hopes to bring in even more firms, both foreign and domestic to maintain it.

Source: Daxue consulting. Note: Net take-up is a measurement of gross leasing activity for a given period of time. Vacancy rate is the percentage of all available units in a rental property.

Currently, around 75% of shopping centers are occupied by shopping malls since department stores declined in popularity[1], and many plan to convert into shopping malls in the near future. For example, Maoye department store (茂业百货), one of the most famous department stores in Shenzhen in Huaqiang North (华强北), made the switch to HuaqiangMaoyeTiandi shopping mall (华强茂业天地) in July of 2015.

According to the 2016 Shenzhen Retail Business Customer Satisfaction Report[2], the average time consumers spend shopping per trip reached 108 minutes in 2016. The average time for shopping malls specifically was the longest, where consumers spent over two hours.

Recent changes in average shopping time are a product of the changing design of Shenzhen’s shopping centers. Normally, there are more than 9 floors in the department stores of Shenzhen. For shopping malls, there are usually around six floors, but the surface area of each is relatively much larger than those of department stores. The larger space of each floor exposes consumers to more brands per floor, thus increasing average shopping times.

In the report’s evaluation index of customer perception and experience, Shenzhen residents are particularly concerned with the scale and comfort of the leisure areas in a shopping area. Compared with department stores, customers’ demand of leisure offerings is much more be easily addressed by full-fledged shopping malls. For instance, a quarter of COCO Park (one of the most popular shopping malls in the Futian(福田)districts) is dedicated to leisure. It provides activities and services such as ice skating, nail care, skin care, and others. But for department stores, like Maoye, leisure services are minimal or non-existent.

Malls also have the distinct advantage of offering more unique customer experiences. Many stores and brands open their concept stores in shopping malls to display their brand culture, attract new customers, and in some cases, offer a VIP experience. For example, HEYTEA (喜茶), the popular Chinese cheese tea brand which created a buzz earlier this year, opened its concept store “HEYTEA BLACK” (喜茶黑金店), at the beginning of January 2017 in MIXC (万象城). The concept-store utilized a zen theme, in addition to offering some special drinks only available in this unique store.

These theme exhibitions in shopping malls are gaining traction in China, especially those that offer consumers an interactive experience. In December of 2016, COASTAL CITY (海岸城),the largest shopping mall in Nanshan (南山) districts, held the “ZOMAKE Creator Cube” exhibition, which used popular animated images from across social media platforms as the theme and offered a series of related activities.

The “ZOMAKE Creator Cube” exhibition held in COASTAL CITY (海岸城) shopping mall in December 2016. Source: Weibo.

Exhibits like this effectively get consumers to engage with a brand’s culture and products free of charge. Of course, many of those products also were sold at the exhibition. With ZOMAKE Creator Cube, products and goods inspired by the social media highlights were made available to participants at the exhibit. By giving consumers a firsthand taste of their brand, these firms are both driving sales and brand awareness.

Enhanced shopping experiences are a major force behind the shopping complex takeover in Shenzhen. With shopping malls offering more engagement through leisure services, interactive shopping experiences, and massive brand exposure, they are quickly becoming the premier shopping destinations for Shenzhen residents.

Increasing demand promotes new business centers to gather in different districts

As a result of large construction projects in across the city, Shenzhen is striving for a multi-center pattern. Almost half of incoming shopping complexes will be built in the Bao’an(宝安) and Longgang(龙岗)districts, running parallel to urbanization in those areas.

Shopping malls in rural areas have also begun to develop into major business centers. Source: Daxue Consulting

Currently, Futian (福田) and Luohu(罗湖)are two main business areas in Shenzhen with lots of shopping malls and business plazas. However, according to a 2016 report from the Shenzhen Bureau of Statistics, Bao’an and Longgang have relatively higher growth in retail sales of customer goods. The sales volume growth rates are 8.1% and 8.3% respectively, providing ample opportunity for investment.

According to SOHU (搜狐), one of the leading company of new media in China, there will be at least 22 new shopping malls beginning operations in 2017. The Longhua and Bao’an districts will play host to a majority of them, and while they may not have the same infrastructure as more developed districts like Luohu, they are rapidly expanding all the same.

New coming shopping centers in the Longhua and Bao’an districts will have larger leisure space, which caters more to contemporary customer demands. This is in part due to the fact these districts hold the two largest populations among the ten districts, according to the Shenzhen Bureau of Statistics. In this case, shopping malls in those three areas will be a key indicator of the success of the highly-demanded, large-scale leisure areas.

Shenzhen shopping malls seek to differentiate

The average sizes of shopping centers in Shenzhen are expanding aggressively, according to 2016 CBRE report. According to the report, Shenzhen has the most square acreage of under-construction shopping centers in the world. Rapid development is not without its obstacles though, as many shopping malls are struggling with homogenization. Recent research shows that lots of shopping malls have very similar brands, such as H&M, Muji, ONLY, VERO MODA and so on, which is aesthetically dull for frequent customers. This is also why newer shopping malls have stressed introducing more undiscovered brands.

A forum held by Shenzhen Retail Business Association and Shenzhen Chain Store & Franchise Association in 2016 also attempted to address the issue. Managers in attendance concurred that diversifying brands was not enough. The key competitive force of any shopping mall should be its unique shopping experiences. In this case, the design of shopping malls, clear marketing, as well as attractive themes will be the major determinants of unique individuality and diversification.

COCO Park has successfully distinguished itself from other shopping malls in this area. It boasts the first indoor walking trails inside a shopping mall in China. The brands inside COCO Park also have relatively short tenures. According to Winshang (The No.1 Commercial Real Estate Portal in China), 15% of brands in COCO Park has been changed or swapped out for different stores in 2016. Between 2014 and 2016, COCO Park made almost 50 of these adjustments. Among those brands, 80% of them are clothing or food and beverage brands. For clothing brands, the newly introduced brands targeted the middle-class consumer in Shenzhen. For food and beverage brands, there are two main types, new-comers, and popular specialty restaurants.

The size of the rural business districts such as in Longgang and Longhua New District nearly rival those in the heart of Shenzhen, despite lower consumer traffic.However, these rural districts will have more opportunity to expand in the near future, and thus will welcome the increased competition.

For this to happen, the chairman of Shenzhen Retail Association has indicated that shopping malls in Shenzhen still have not reached maturity yet, at least with respect to Shenzhen residents’ consumption capacity. Malls with poor performance are now adopting complex-wide themes, in order bolster turnout from a niche or select market segments, such as with children or women-focused designs.

The position of business determines future success of shopping mall in Shenzhen

Daxue Consulting has found the that the most successful industry in Shenzhen shopping centers is clothing, following closely by food and beverages.

With the rising influence of digital stores and online shopping, most traditional brick and mortar retailers are losing market share. Some industries, however, remain partially resilient to these forces. By and large, high-end clothing stores and restaurants will not be replaced by digital stores, as trying on expensive clothes and dining out cannot be digitized. For high-end clothing consumers, most are very price inelastic and enjoy the very process of going out to shop. With dining, more and more Chinese citizens are opting to go out with their friends and family as a fashion lifestyle. Ultimately, the in-person nature of high-end clothing shopping and dining out will keep those industries prosperous in Shenzhen, despite technology advancements that facilitate consumer spending in other areas.

In a city with a large youth and young adult population, some of Shenzhen’s shopping malls have started modeling their aesthetic with that in mind. For instance, the “1234 space” in Shenzhen has been a hit among the post-80s and 90s generations. 1234 space’s target demographic has been younger, middle-class citizens. Most of 1234’s stores are commonly associated with and frequented by this demographic, and stores that fall under the “fast fashion” brands label like Zara and H&M are highly prevalent. Smaller stores at the mall are also trend-conscious, such as bookstores with coffee, hand-made goods workshops, music tutorial and painting corners, which are very popular among young adults in China. Energetic and eye-catching designs cover the outermost Window panes to further convey the atmosphere of youthful spirit. All these strategies have contributed to the high popularity of “1234 space” in Shenzhen.

The outside look of “1234space” is covered with fashion and energy

There could be several future trends for shopping malls in Shenzhen:

- Future shopping malls in Shenzhen will be an integrated center for people to relax and enjoy social activities, combining catering, entertainment, arts, and unique offline experience rather than just exclusively shopping. These shopping malls could eventually foster and develop a new lifestyle for young consumers, and be more competitive with expanding digital stores.

- For the brick and mortar stores, more restaurants and medium to high-end clothing stores will continue to enter the market and maintain a majority share. Other boutique brick and mortar stores may serve to help portray or establish a shopping complex’s identity or target market.

- Shopping malls may begin organizing some interesting activities related to their area and cooperate with their existing stores to attract target customers and generate excitement about their mall.

Conclusion:

Following an economic trough in 2012, Shenzhen invested in large commercial projects, specifically shopping centers, to reinvigorate the city’s growth. As these shopping centers grew steadily and began contributing to the city’s economy, Shenzhen has started to form a multi-center pattern throughout its different districts. There are two major problems for shopping malls right now how to handle the stronger competition and distinguish themselves from an increasingly homogenized market. The critical solution could be to differentiate brands and target specific customer segments. In the future, it is very likely that shopping malls in Shenzhen, but also in Shanghai, Guangzhou, and Beijing, will become integrated entertainment centers with many amenities and diverse shopping experiences.

Case Study: Shopping malls in Shenzhen

A consulting company was doing a research about shopping mall in Shenzhen. The client’s company is involved in the luxury research business. Base on their request, Daxue Consulting conducted the retail analysis and demography analysis about shopping malls in Shenzhen for completing their research. Daxue Consulting provided them with perspicacious analysis through social listening and competitor analysis.

Feature image credit: ”宝能all city” – the first shopping mall in Shenzhen bay area, built in 2012. Source: Winshang (赢盛中国)

To know more about the Shopping Malls in Shenzhen, contact our dedicated project managers by email at dx@daxueconsulting.com