Semiconductors are the brains of all electronic devices, from microwaves to mobile phones and from drones to automobiles. They are essential components that allow the development of technologies crucial for economic growth, national safety, and global competitiveness. Therefore, countries are competing to win the semiconductor industry race and gain a competitive edge. However, due to geopolitics, China’s semiconductor industry is speeding up efforts to innovate and be self-reliant in semiconductors, aiming to boost its chip industry.

Inside the semiconductor supply chain: Roles and specialization

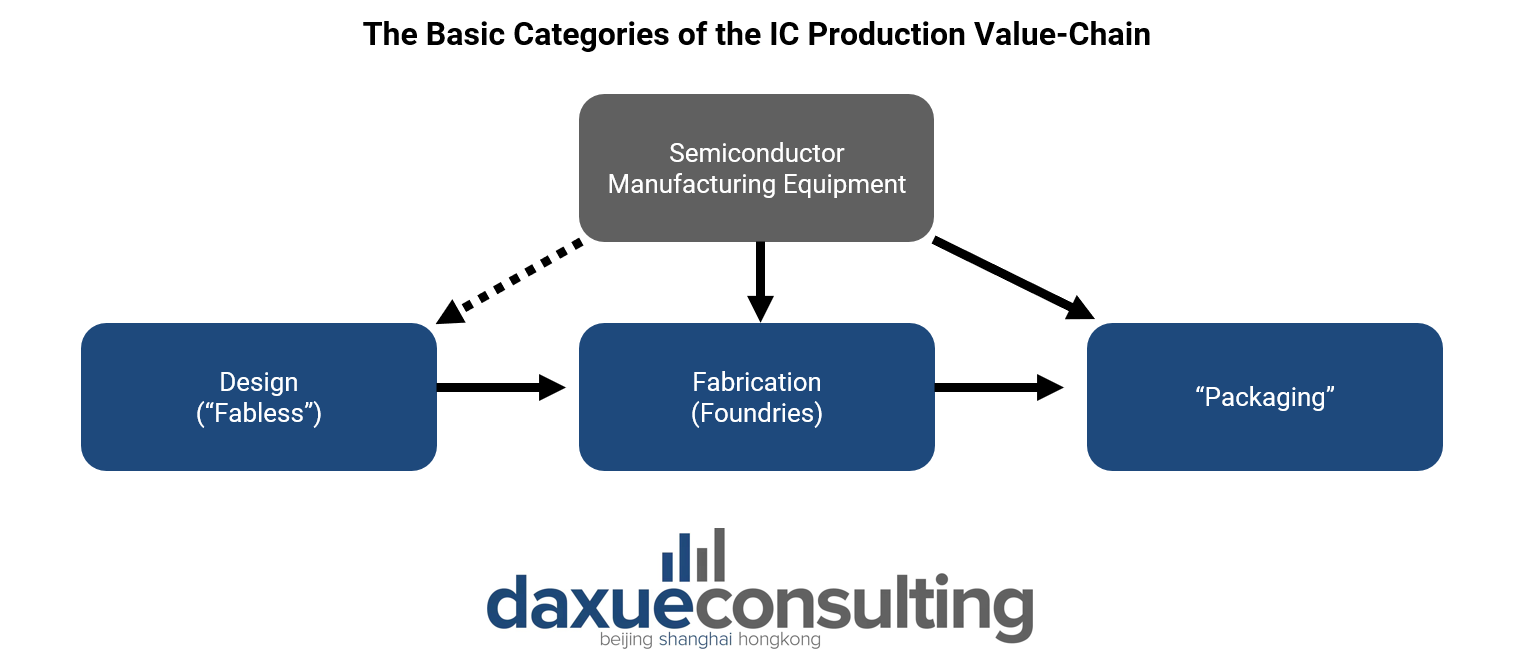

Essentially, semiconductors are created through three steps: design, manufacturing, and assembly. We can also divide the companies in the semiconductor industry into four major segments based on their role in the value chain:

- Design: design integrated circuits (ICs) for a specific purpose.

- Manufacturing: fabricate the ICs.

- Assembly/Packaging/Test (APT): assemble the ICs into a chip, which is then integrated into electronic devices by product manufacturers.

- Semiconductor manufacturing equipment: Manufacture capital goods used to automate functions in other semiconductor segments.

In recent decades, semiconductor companies transitioned from the Integrated Device Manufacturers (IDM) model. It combines design, fabrication, and packaging functions, specializing in one of the four supply chain segments:

- Pure-play design companies (Fabless) –purely focus on creating software and intellectual property.

- Pure-play manufacturing companies (Foundry) –manufacture chips for Fabless.

- OSAT (Outsourced Semiconductor Assembly and Test) companies –specialize in the APT segment of semiconductor manufacturing.

- Equipment manufacturing companies

Tracking progress: China’s semiconductor industry’s rise in 2022

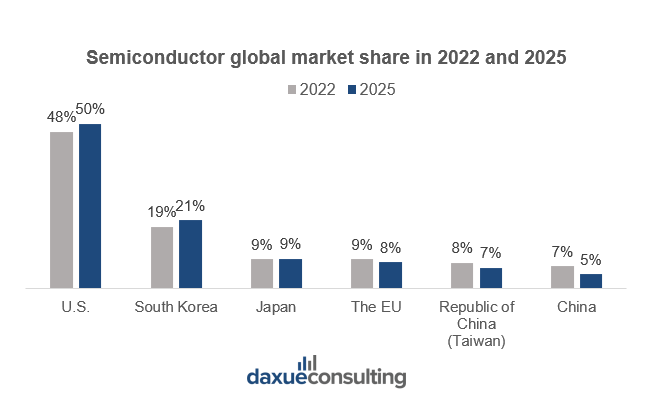

Globally, 1.15 trillion units of semiconductors were distributed in 2021, around 146 units for every person on Earth. When it comes to market share, the US semiconductor industry is at the forefront with a 48% market share in 2022. On the other hand, China’s semiconductor industry is lagging far behind with a 5% market share. As compared to 2022, the Chinese semiconductor industry’s market share shrank by 2%.

Taking a closer look at who the frontrunners are of each segment, we have the US semiconductor industry in the fabless segment, and the Republic of China (Taiwan) in the foundry segment. Meanwhile, Japan, the Netherlands, and the US are sharing the lead in the manufacturing equipment segment.

China’s semiconductor industry: A 55% contributor to APAC and 31% globally

Starting in 2001, the Asia Pacific became the leading region in semiconductor sales due to the shift in electronic equipment production. The market’s remarkable growth is evident, soaring from USD39.8 billion in 2001 to over USD330.9 billion in 2022. China is the largest country market, contributing 55% to the regional APAC market and 31% globally. In 2020, China’s semiconductor industry consumed nearly a quarter, 24%, of the global semiconductor-enabled electronic devices.

Escalating trade controls had taken a toll on China’s semiconductor industry

After the conflict between Russia and Ukraine broke out, the US government spearheaded the banning of advanced technology exports to Russia to impede its economic and military development. The country then extended the export ban to China.

In October 2023, the Biden administration further restricted American companies from selling certain types of semiconductors to China. The reinforcing controls, which banned the export of artificial intelligence (AI) computing chips to China, specifically Nvidia Corp’s and Advanced Micro Devices Inc.’s (AMD) chips, are still in force. These measures aimed to prevent potential military applications in China and close regulatory loopholes. The move has escalated tensions, with Beijing accusing Washington of weaponizing trade and tech issues.

China’s AI industry heavily relies on Nvidia and AMD, making the ban on these companies the initial chokepoint in the semiconductor supply chain. This significant control over crucial links creates potential bottlenecks and disruptions, particularly impacting both China’s AI industry and the semiconductor sector.

Global restrictions tighten: Japan and the Netherlands join

Following the US, Japan implemented restrictions on semiconductor manufacturing equipment exports to China from July 2023, and the Netherlands from September 2023. These measures pose additional hurdles for China in its quest to develop independent chip manufacturing capabilities and attain self-sufficiency.

China’s other chokepoint is TSMC, the largest foundry in the world. Over 90% of highly developed nodes and 50% of global semiconductors are produced by TSMC. The Chinese semiconductor industry relies heavily on TSMC. In the first half of 2022 alone, China imported ICs from Taiwan (China), with a total value of USD 79.4 billion, accounting for almost 38% of the country’s total such imports during the period. Thus, unlike other sectors, China does not impose sanctions on chip imports from the Formosa Island even amidst the growing tension in the Strait, specifically after the visit of the Speaker of the United States House of Representatives, Nancy Pelosi, in August 2022.

Recent developments in China’s semiconductor industry

China has achieved a significant degree of localization for mature nodes (≥28nm). This was due to the expansion of SMIC and Huahong’s capacity. This had increased China’s global market share of mature-node production from 19% (2015) to 33% (2023). As China focuses on volume and price competition in mature markets, it has resulted in overcapacity. This has led to intense price wars and diminished profitability.

However, for leading-edge nodes (<14nm), China’s capabilities remain limited and lag two to three generations behind global leaders such as TSMC and Samsung. The prevailing challenges lie in yield rates and building effective high-volume capacity in advanced nodes. Moreover, there is a gap in high-end semiconductor engineers, particularly for advanced R&D and IP design. The problem is compounded by a “brain drain,” where top talent is poached by private firms or foreign companies offering higher salaries. To truly compete at the forefront, China would need to make breakthroughs in alternative chip architectures such as chiplet design, RISC-V, and other niche technologies, all while solving its high-end talent shortage.

Global restrictions tighten: Japan and the Netherlands join

Following the US, Japan implemented restrictions on semiconductor manufacturing equipment exports to China from July 2023, and the Netherlands from September 2023. These measures pose additional hurdles for China in its quest to develop independent chip manufacturing capabilities and attain self-sufficiency.

China’s other chokepoint is TSMC, the largest foundry in the world. Over 90% of highly developed nodes and 50% of global semiconductors are produced by TSMC. The Chinese semiconductor industry relies heavily on TSMC. In the first half of 2022 alone, China imported ICs from Taiwan (China), with a total value of USD 79.4 billion, accounting for almost 38% of the country’s total such imports during the period. Thus, unlike other sectors, China does not impose sanctions on chip imports from the Formosa Island even amidst the growing tension in the Strait, specifically after the visit of the Speaker of the United States House of Representatives, Nancy Pelosi, in August 2022.

Driving self-sufficiency: China’s semiconductor industry journey since 2014

China has prioritized semiconductor development as a key part of its government agenda to grow its in-house IC industry. Since 2014, China has been working towards self-sufficiency in the semiconductor industry, notably through initiatives like “Made in China 2025.” Recent acceleration in this journey can be attributed to the US-China trade war from 2018 and Huawei’s blacklisting.

Moreover, to support these efforts, the Chinese government introduced new income tax exemptions and import duty exemptions for advanced technology nodes. The “Big Fund,” a state investment fund exceeding USD 50 billion for chips, was reinstated. Additionally, a new National Science & Technology Commission was established to coordinate industry efforts.

In July 2025, China introduced a 10% tax credit for foreign investors who reinvest profits domestically. The policy is effective from January 2025 to December 2028. This policy aims to encourage sustained foreign investment in critical sectors, including semiconductors. Furthermore, according to SEMI, a microelectronics industry association, there are 18 new semiconductor fabs that are scheduled to start construction in 2025. The Americas and Japan lead with four projects each, followed by China and Europe with three each. As such, China continues to lead in global capacity expansion, with installed wafer fab capacity projected to surpass 42.5 million wafers per quarter (300mm equivalent) in Q1 2025, which is a 7% year-on-year increase.

Chinese semiconductor industry: Challenges and opportunities

- In 2022, the US led with a 48% market share, while China lagged at 7%, though it increased by 2% from 2020, and was a major contributor to the Asia-Pacific market, accounting for 55%.

- Intensified tensions led to trade controls, export bans, and disruptions, impacting China’s AI industry and semiconductor sector.

- Following the US, Japan, and the Netherlands’ restricted semiconductor manufacturing equipment exports to China, this adds challenges to its quest for self-sufficiency.

- The PRC is a net importer of microchips, recording a notable increase in semiconductor equipment imports from the Netherlands, even with the implemented export restrictions.

- Prioritizing development since 2014, China accelerated efforts with initiatives like “Made in China 2025,” tax exemptions, and substantial investments, aiming for self-sufficiency amidst global trade tensions.