The Chinese cosmetic market is a global powerhouse, accounting for approximately 20–25% of the total global industry value. Building on earlier observations of rising interest in domestic brands among younger consumers, the market has now shifted. While international heritage brands once dominated, domestic “C-beauty” players have successfully converted early consumer curiosity into sustained market leadership, fundamentally reshaping China’s competitive landscape.

Download the 2026 China Beauty Report here

Chinese cosmetic market growth and category dynamics

The Chinese cosmetic market has demonstrated steady and resilient growth, reinforcing its role as a core pillar of the national consumer economy. Market value expanded from USD 542.3 billion in 2018 to USD 694.2 billion in 2024. This growth is not merely cyclical, but structural: cosmetics’ share of total consumer retail sales increased from 1.5% in 2015 to 2.5% in 2024, signaling that beauty and personal care have transitioned from discretionary spending to everyday necessities.

Within this expanding market, category composition reveals a maturing and increasingly sophisticated structure. Skincare remains the largest segment, accounting for roughly 50% of total market value. However, makeup (color cosmetics) has emerged as the fastest-growing category. Although it represents only 18% of the market, makeup recorded a CAGR of 5.5% from 2018 to 2024, the highest among all product types. This growth reflects rising demand for personalization, self-expression, and trend responsiveness among younger consumers.

Most notably, domestic brands have moved from challengers to leaders. By 2024, C-beauty brands accounted for 55.2% of the total market share. This was driven by stronger cultural resonance, improving functional performance, and sharper alignment with underserved consumer segments.

The strategic importance of lower-tier markets

A critical driver of this shift is the growing importance of China’s lower-tier cities. Historically overlooked by global, especially luxury-brands, these regions collectively represent over 50% of China’s population. In 2024, counties, towns, and rural areas contributed38.8% of national consumer-goods retail sales, creating a substantial but underpenetrated opportunity.

Domestic brands have capitalized on this structural imbalance by tailoring products and pricing to local purchasing power. Consumers in lower-tier markets also exhibit higher loyalty toward domestic brands, influenced by lower exposure to globalization and stronger nationalist education. As a result, domestic players enjoy both pricing flexibility and emotional affinity advantages.

Pricing comparisons illustrate this divergence clearly. Domestic brands such as Timage (彩棠), Flower Knows (花知晓), and Judydoll (橘朵) typically price cushion foundations between USD 15 and 30, while comparable products from Dior, Estée Lauder, and L’Oréal often range from USD 45 to 85. Although exceptions exist where Mao Geping(毛戈平) is poised at the premium end, the broader trend remains consistent: domestic brands dominate the value segment and treat lower-tier markets as core growth engines, while global brands largely position them as secondary.

Consumer demographics and market segmentation

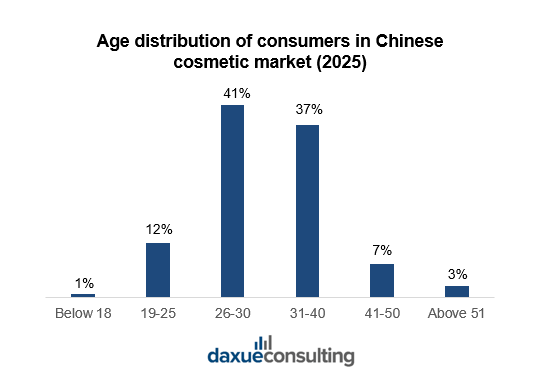

Demographic structure further reinforces these dynamics. Consumers aged 26–30 (41.0%) and 31–40 (36.8%) dominate cosmetic consumption, reflecting stable income levels and a growing emphasis on functionality and brand credibility. Meanwhile, younger consumers aged 19–25, though smaller in share (11.6%), display higher experimentation rates and stronger sensitivity to design and trend aesthetics.

Gender diversification is also reshaping the market. Men’s cosmetics demand has surged, particularly on Douyin, where men’s beauty sales exceeded USD 140 million in 2023, representing a 235% year-over-year increase. Rather than offering generic products, brands are responding by targeting specific functional needs and usage scenarios. For example, Make Sense(理然) offers simplified all-in-one skincare solutions for males, while Judydoll(橘朵) has developed performance-oriented makeup for outdoor and sports use. This focus on specialized functions and use cases highlights how precise segmentation is driving brand success.

The marketing and sales ecosystem: A closed-loop model

China’s beauty consumer journey is overwhelmingly digital. By 2025, online channels accounted for 54.1% of total cosmetic sales and are expected to grow at an 11.1% CAGR through 2031. However, the digital ecosystem extends far beyond the transaction itself.

Social platforms such as Douyin and RED function as discovery engines, where influencer seeding and short-form content generate demand, while final purchases are typically completed on Taobao, Tmall, and JD.com—platforms valued for reliability, logistics, and price competitiveness. This creates a dual-platform dynamic in which social media drives desire and traditional e-commerce executes conversion.

As consumers grow more skeptical of purely digital claims, offline experiences have become a key differentiator. Brands use physical touchpoints to enable firsthand product verification: Mao Geping (毛戈平) offers high-touch professional consultations through department store counters, while Perfect Diary (完美日记) combines experience stores with pop-up events. These interactions not only drive in-store sales but also generate user-generated content on RED, reinforcing trust and converting online consumers through digital word-of-mouth.

The rise of the domestic brands and the fall of the global brands

As previously discussed, a historic transition is underway in the Chinese cosmetic market, with domestic brands now surpassing international players in market share. This shift is primarily driven by two reinforcing forces: ingredient sophistication and cultural resonance. 58.8% of Chinese consumers now rank ingredients as their top purchasing criterion, signaling the rise of “skintellectuals” who prioritize scientific efficacy over brand heritage. Domestic brands such as Pechoin(百雀羚), Biohyalux (润百颜), and Quadha (夸迪) have capitalized on this trend through R&D-driven formulations and modernized applications of traditional ingredients.

At the same time, Eastern aesthetics has emerged as a powerful emotional differentiator. Brands including Florasis(花西子), Catkin(卡婷), and Mao Geping(毛戈平) embed cultural symbolism directly into product design, aligning with the Guochao movement and pairing it with formulas tailored to Asian facial features and preferences for natural, low-saturation looks—an area where standardized global designs often fall short.

This structural realignment has placed mounting pressure on global brands. Sephora, for example, reduced its China workforce by approximately 10% amid slowing offline traffic. Industry observers note that as domestic brands maintained aggressive engagement on Chinese social platforms during market disruptions, many Western brands failed to adapt at a comparable speed, resulting in declining visibility and lost momentum.

Domestic success and foreign implications

Domestic brands have succeeded by pivoting toward a science-first and culture-led strategy. By prioritizing ingredient transparency and R&D-backed efficacy, local players have captured the “skintellectual” consumer, while integrating Eastern aesthetics into product design to foster emotional resonance. Furthermore, their mastery of a digitally integrated, closed-loop ecosystem has set a new benchmark for consumer engagement.

For foreign brands, these developments imply that “one-size-fits-all” global strategies are no longer sufficient. To remain competitive, international players must move beyond brand heritage to balance technical precision with deep, localized cultural relevance, ensuring products are as dynamic and segmented as the Chinese consumer base itself.

From localization to ecosystem fit: Why domestic brands succeed

- The Chinese cosmetic market has entered a structural inflection point, with domestic C-beauty brands surpassing global players by aligning more closely with local consumers.

- Lower-tier cities have become a core growth engine, allowing domestic brands to outperform through accessible pricing, higher loyalty, and targeted distribution.

- Consumer demand is increasingly segmented, driven by functionality, personalization, and emerging categories such as men’s grooming.

- The beauty purchase journey operates as a closed-loop system, where social media drives discovery, e-commerce executes conversion, and offline experiences build trust and amplify digital word-of-mouth.

- Foreign brands must localize deeply to compete, defining a clear differentiation while adapting products, positioning, and go-to-market strategies to China’s unique ecosystem.