Before talking about Chinese kitchen appliances, it is worth tracing identifying what kitchens mean today for Chinese consumers. For Chinese people, food is an integral part of daily life. Eating together and enjoying good food are considered to bring harmony and connections to family and relationships in China. Consequently, as an area where food is stored, cooked, and prepared, the kitchen is one of the most important rooms in a house.

The evolution of kitchen in China

During ancient China, feng-shui had a significant impact when it came to deciding kitchen doors and hearth’s orientation.

Chinese kitchens witnessed a fast development following the foundation of the PRC and the launch of economic reforms in 1978. Since the ’90s, housing has evolved into a consumer good, and emphasis has been drawn to its functional features. Consequently, the design of kitchens began to take on different forms.

Meanwhile, saving time became of major importance for Chinese people. the government introduced standardized kitchen layouts, which set fundamental specifications for kitchen and associated housing equipment.

With economic development, the function of the kitchen has changed from that of a cooking area to that of a complete living environment. Modern kitchen designs are taking into account ways to increase kitchen efficiency and make cooking more attractive in order to adapt to the numerous food options in light of nowadays’ fast-paced lifestyle.

All you need to know about Chinese kitchen layouts and trends

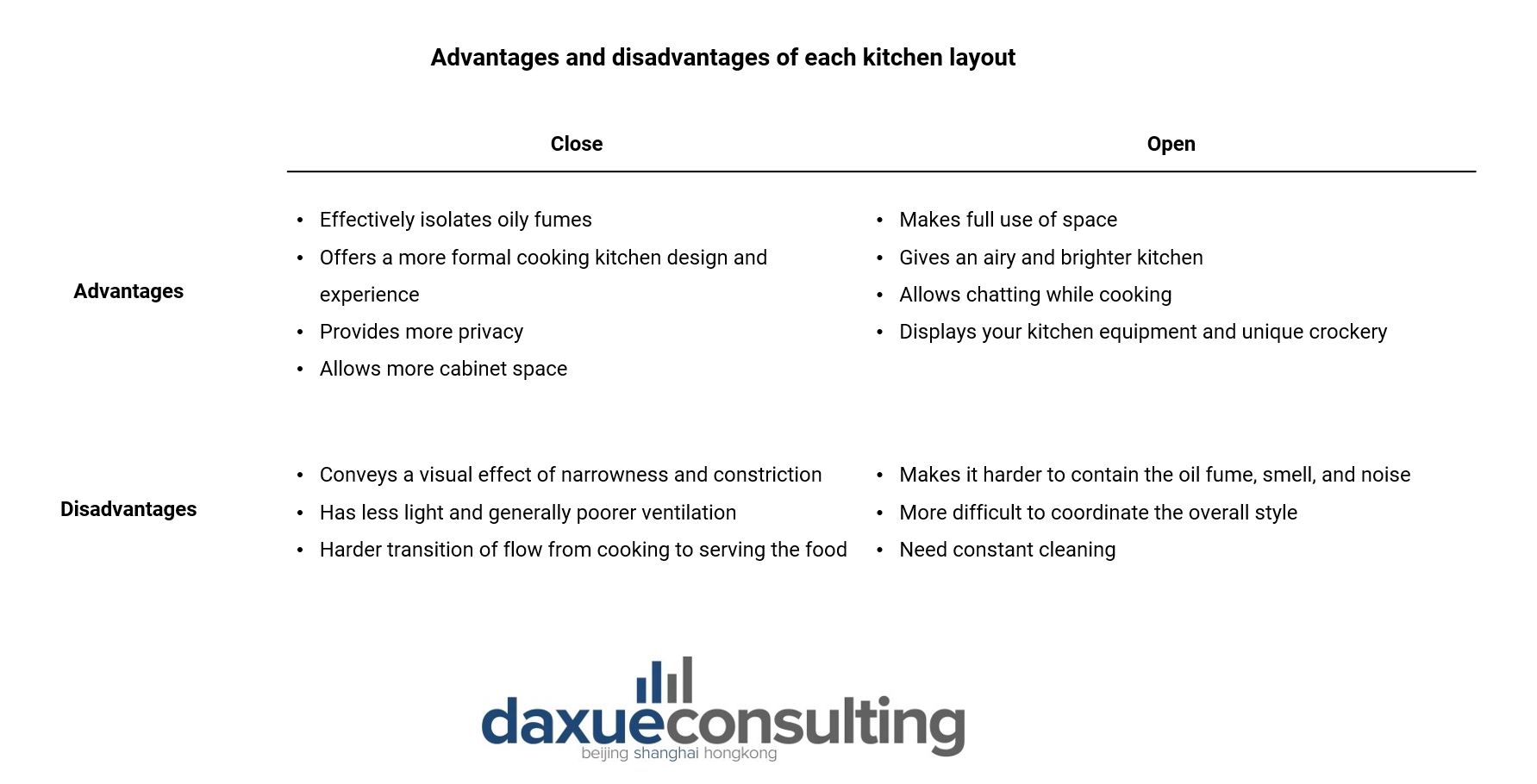

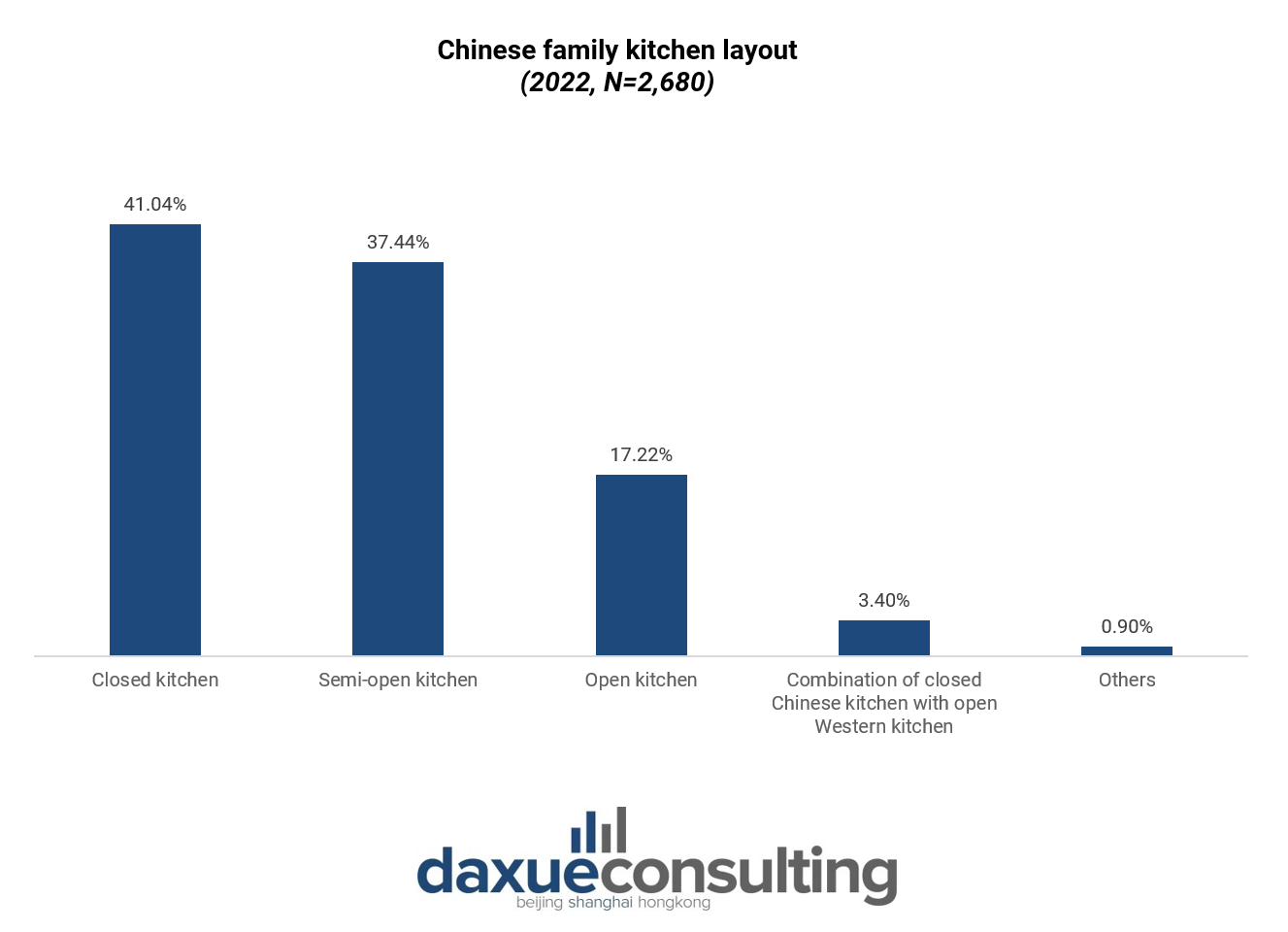

Chinese food is often associated with stir-frying which causes a lot of fumes. Therefore, most Chinese kitchens adopt a closed, or semi-closed, layout. A closed kitchen essentially means that there is a separator between the dining room and the kitchen. In China, this layout is meant to prevent cooking fumes from spreading into the rest of the house.

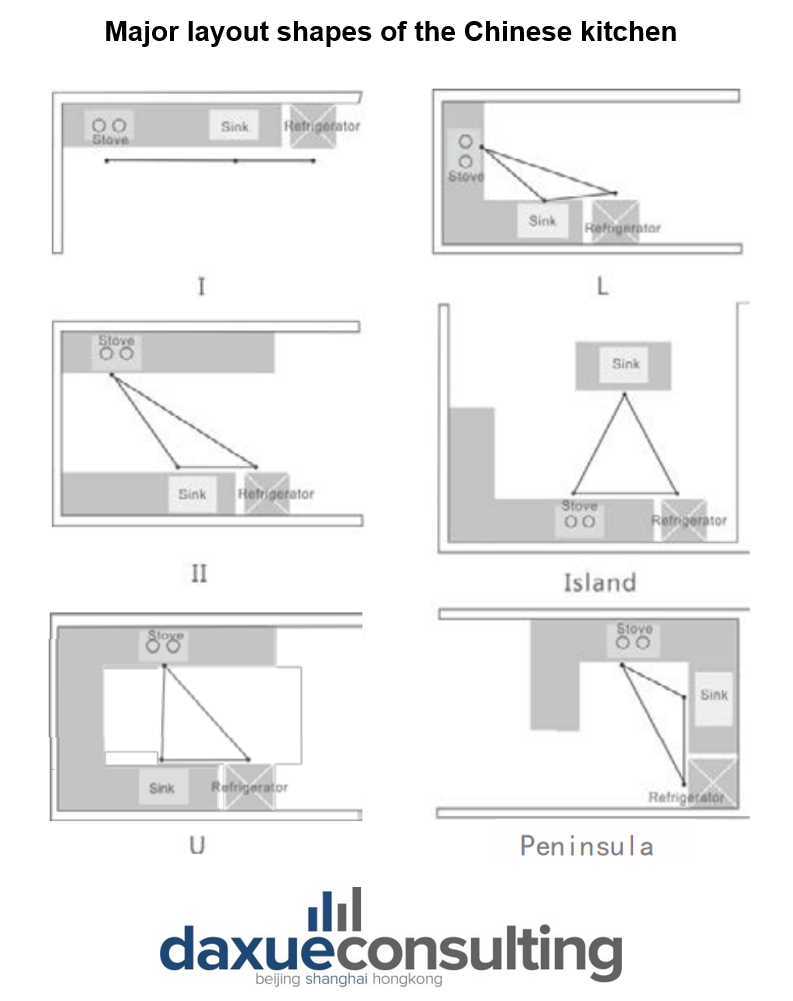

There are six major layout shapes of the kitchen in China. These kitchen layouts were created using the work triangle from the cooking process: store (refrigerator), wash (sink), and cook (stove) with L-, I-, and U-shaped kitchens being the most widely used.

Comparing the kitchen in China to its western counterpart

Kitchens in western countries typically feature an open kitchen layout since western cooking methods tend to produce less fumes. In addition, they are usually larger than Chinese kitchens and have almost no doors. As people tend to entertain guests while they are cooking, the entire kitchen works as a social hub.

The open kitchen concept is gaining popularity

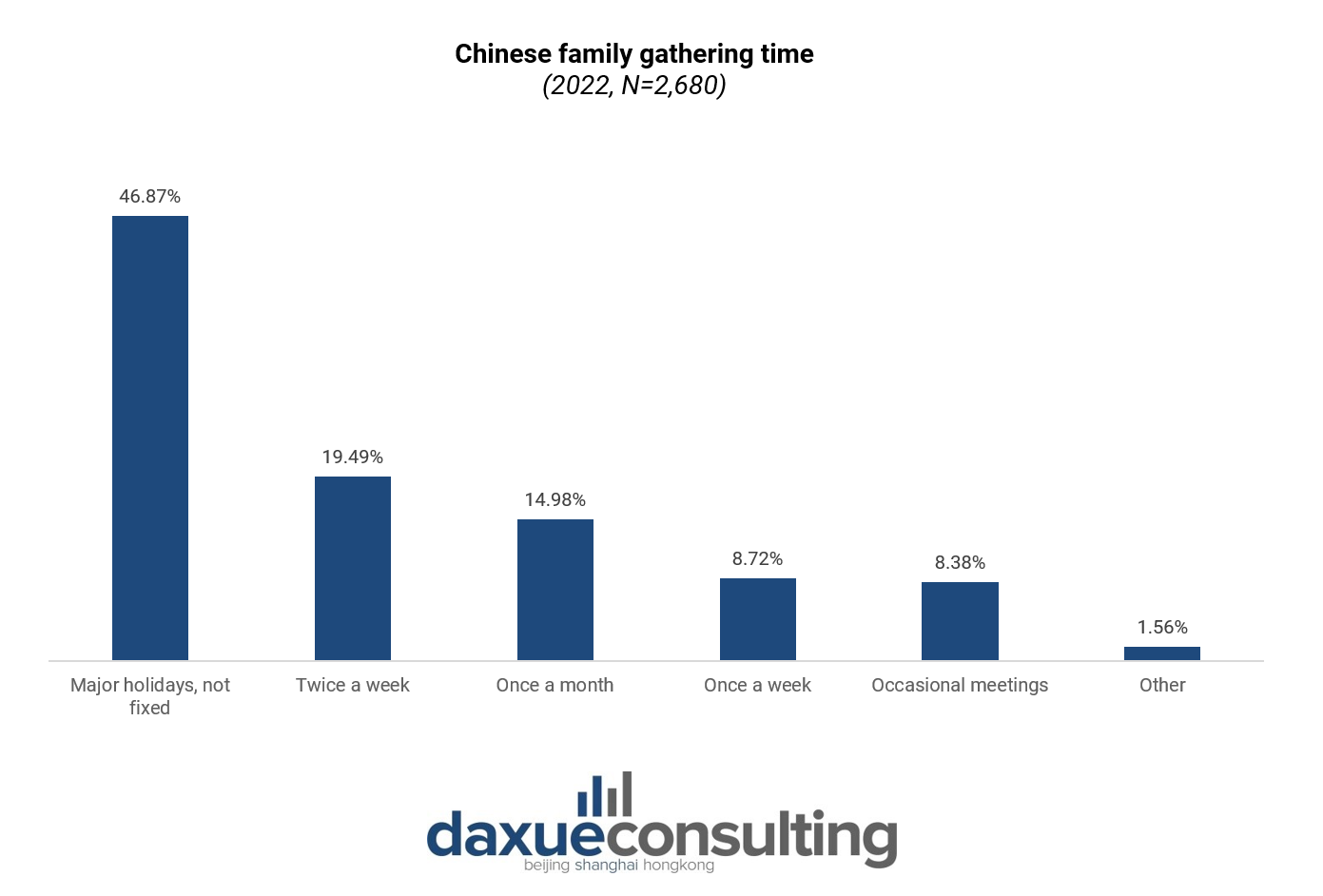

As society changes, kitchens design and functions change as well. Due to the pandemic, Chinese kitchens become a social hub. According to China’s home grid survey, nearly half of respondents would choose to gather with relatives and friends at home during major holidays.

Open and semi-open kitchen concepts are also becoming a trend. For example, Forbes reported that over 50% of surveyed consumers think that it is necessary to build an open kitchen, 92% prefer to chat while cooking and that kitchens can be used as an important place for parent-child moments.

Understanding the market demand for kitchen appliances in China

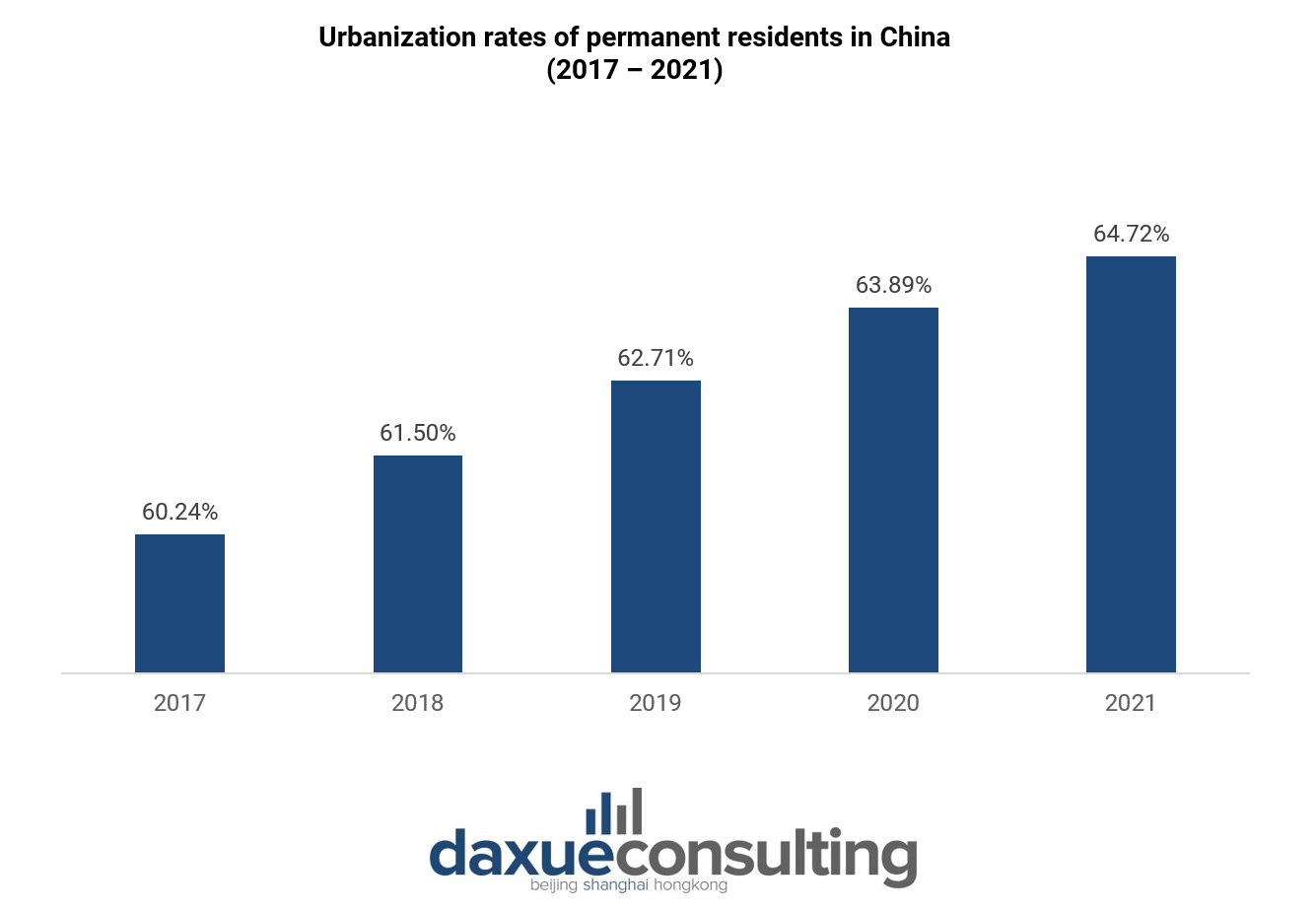

One factor influencing the demand for kitchen appliances in China is the urbanization rate. The urbanization rate of permanent residents in China increased steadily over the last decades: it jumped from 60.24% at the end of 2017 to 64.72% in 2021, driving demand for both household and kitchen appliances. Indeed, a market study found that urbanites possessed twice as many range hoods and microwaves per person as people living in rural areas.

The real estate sector also influences China’s kitchen appliances market as more people mean a greater need for kitchen and other domestic appliances. China’s tighter real estate market policy has been considerably affected the performance of the home appliance market in China since 2018, and especially the kitchen appliance sector. However, attempts are being made to modernize outdated communities. 40,300 old urban residential communities in China’s cities and towns were renovated in 2020, benefiting nearly 7.36 million households. The number even grew larger in 2021 to 55,600. This will boost the kitchen appliances industry in China.

Chinese kitchen appliances market is expected to be the largest in the world by 2022

China’s market for kitchen electrical equipment was estimated by All View Cloud (AVC) to be worth RMB152.8 billion in 2021. Appliance sales decreased by 12% from their pre-pandemic level in 2019 and by 6% annually. However, retail sales revenue climbed by 7% as most product prices rose by roughly 10% as a result of higher raw material costs.

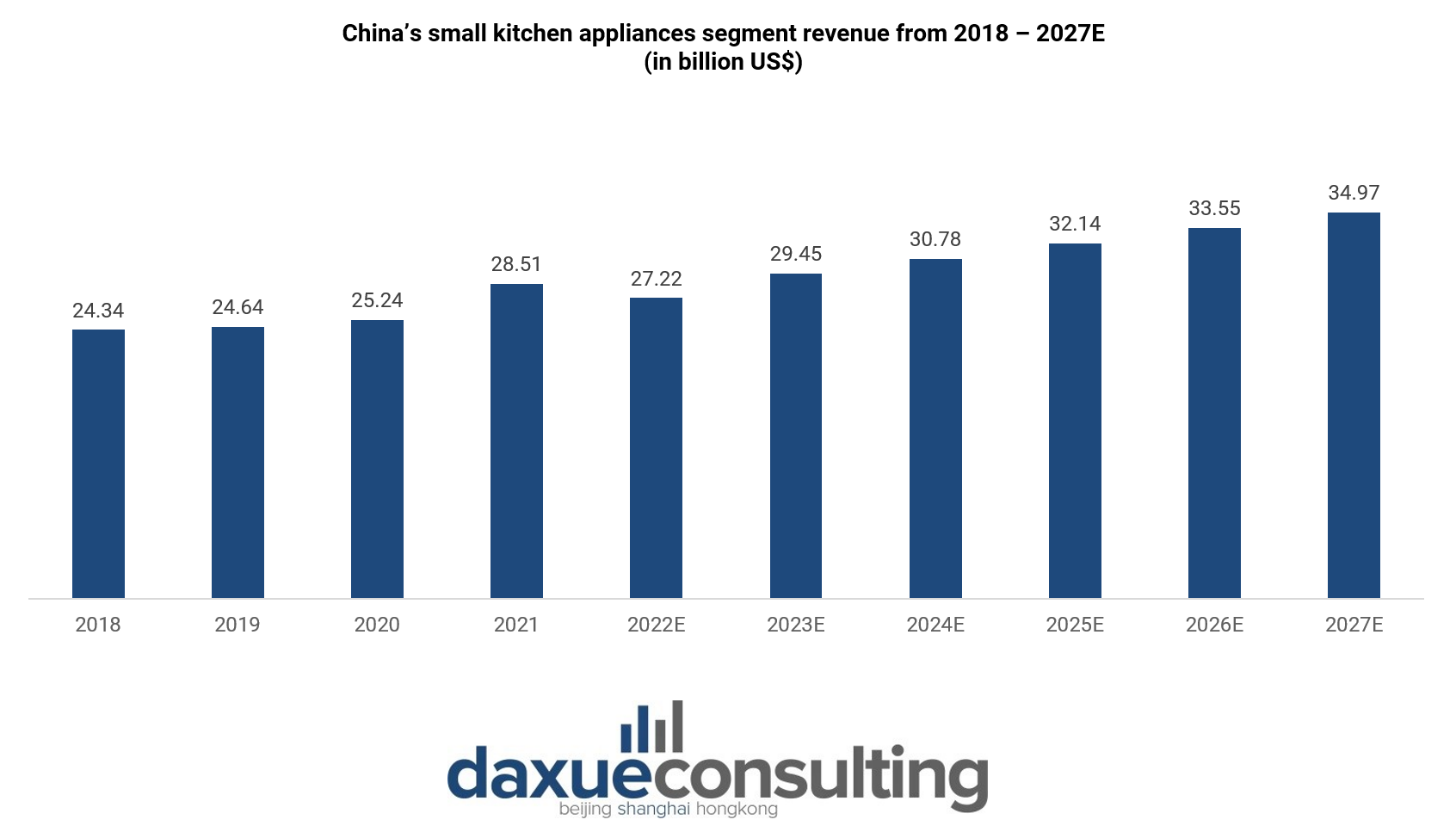

When it comes to small kitchen appliances specifically, the market is expected to generate around US$27.22 billion (RMB189.75 billion) in revenue in 2022. The market is anticipated to further grow by a CAGR of 5.14% from 2022 to 2027. Simply defined, the small kitchen appliances segment encompasses any electrical kitchen devices that are not too big to move such as blenders, rice cookers, microwaves, etc.

New trends shaping Chinese kitchen appliances market: innovation, health, and aesthetics

Smart home appliances, including kitchen appliances, have been trending lately. The primary driver behind kitchen appliances in China is the desire to enjoy a high-end quality of life. The technological development of kitchen appliances is in line with the needs of different types of consumers. They are also designed with efficient cooking in mind, allowing users to prepare meals quickly and easily with the least effort. As a result, over 90% of young people in China claims wanting smarter kitchen appliances.

Health awareness among Chinese citizens has increased recently due to the rise in living standards and the pandemic, which has induced more and more consumers to pay greater attention to their own and their family members’ food-related health issues. 80% of consumers declared that after the pandemic, they pay more attention to home cleaning and sanitation, and are most concerned with the disinfection of tableware. Moreover, over 70% of consumers prefer environmentally friendly kitchen appliances.

Aesthetic is also deemed important in the pursuit of high-quality life. For Chinese consumers, the pursuit of smart and health-oriented appliances must ultimately be realized through a combination of functionality, experience, and beauty. One way to reach such goal when it comes to furnishing the kitchen is by purchasing a complete set of appliances. Hence, it is not surprising that 72% of consumers in first-tier cities claimed considering buying a complete set of kitchen appliances.

Popular appliances and key players in the Chinese kitchen appliances industry

Kitchen appliances related to health and time efficiency are gaining momentum

Beyond rice cookers, microwaves, and refrigerators, some other kitchen appliances are gaining popularity in mainland China. One of them is air fryers. From January to May 2022, air fryer sales increased significantly by 185% as a result of the health-awareness trend. In 2021, the air fryer market in China was worth RMB4.38 billion, or 29% of all sales worldwide. By 2026, that market is projected to generate RMB8.26 billion.

Dishwashers are becoming more and more common among young families due to the smart home trend and the rise of the “lazy economy“. 1.95 million dishwashers were sold in 2021, generating around RMB9.96 billion, amounting to a 14.4% increase from the previous year. At the moment, first- and second-tier cities account for most of the dishwasher sales, but there is potential in third- and fourth-tier cities as well.

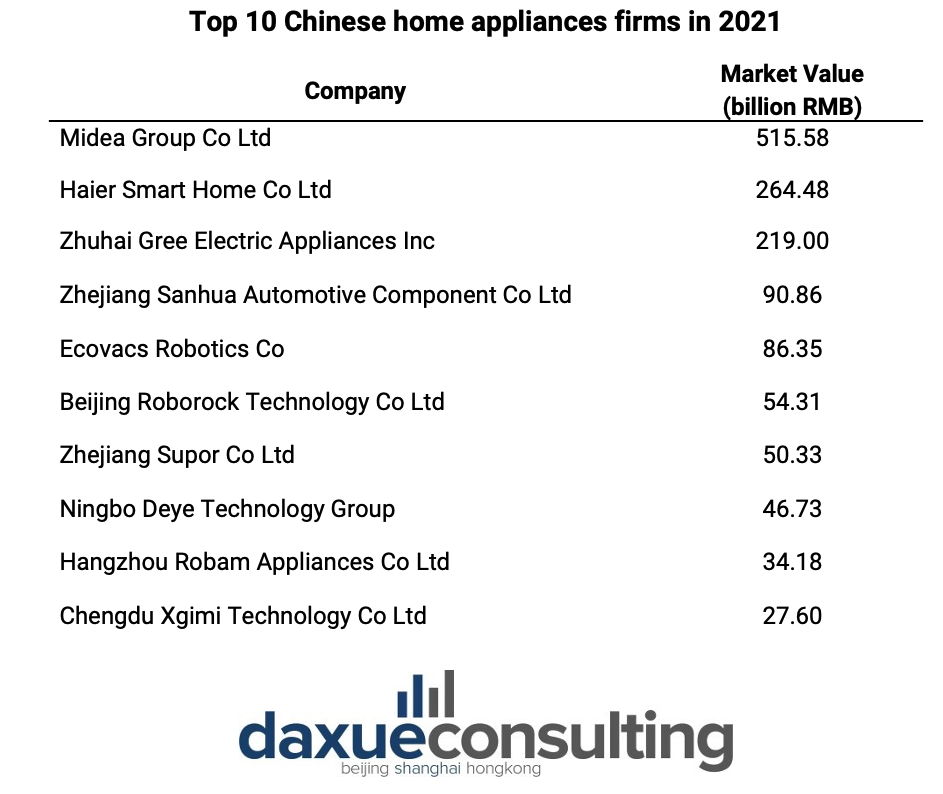

Midea, Haier, and Gree are leading Chinese kitchen appliances industry

In China, there were 86 industrial parks for small kitchen electrical equipment as of mid-June 2022, with Guangdong serving as a significant hub for manufacturing range hoods, microwaves, and refrigerators. The small home appliances industry is thriving in Lianjiang, a city in Guangdong, counting more than 1,100 small appliance manufacturers boasting a production output of around RMB2.7 billion. The manufacturers include 220 rice cooker manufacturers, 90 electric kettle manufacturers, and manufacturers of other accessories. Midea, Haier, and Gree take a significant portion of Chinese home appliances’ market value in 2021.

Other than the obvious factors such as the price and function of the products, service experience is vital for consumers when it comes to kitchen appliances in China. Therefore, after sales and customer service has developed into a competitive edge for brands to gain consumer loyalty.

What to know about kitchen appliances in China:

- The kitchen in China has evolved in terms of layout and design. A closed-concept kitchen is the common Chinese kitchen layout. However, open kitchens are now gaining popularity, especially after the pandemic.

- Chinese kitchen appliances market is growing and is influenced by both the urbanization rate and real estate dynamics.

- Since the COVID-19 outbreak, people are increasingly more interested in smart kitchen appliances which can help them cut down labor time, as well as in devices that can promote health. Aesthetic also plays a vital role.

- Small home appliance industrial parks are concentrated in Guangdong and Zhejiang. Midea, Haier, and Gree are holding the lion’s share in home appliances in China.

- Consumers in China not only consider the price and function of the kitchen appliances but also the after-sales services the brand can offer.

Author: Regina Sukwanto