China’s pet market is experiencing rapid growth, surpassing RMB 593 billion in 2023, a 20% year-over-year growth and a compound annual growth rate of 25% from 2015. At the heart of this expansion lies the pet food market, which accounted for 52% the total pet market spending. Once considered a niche, the pet food market has rapidly grown, fueled by urbanization, rising disposable incomes, and shifting lifestyle preferences. Today, pets are seen not just as companions but as integral parts of modern living, driving demand for premium nutrition, innovation, and tailored experiences in the pet food market.

Download our report on China’s Pet Economy

Treating pets like family is transforming China’s pet food market

Once seen primarily as utilitarian, pets are now embraced as family members, companions, and even child substitutes. This shift has led pet owners to invest more in their care, with pet food receiving the same level of attention as their own meals.

Food is the dominant segment in the pet market, occupying approximately 52% of total pet-related spending. The pet food market alone reached RMB 227.2 billion in 2024, a 9.2% year-over-year increase. As families get smaller and people seek emotional connection, pets increasingly take on central roles in households. With that, the demand for high-quality, nutritious pet food continues to rise, reflecting a deeper cultural investment in animal well-being.

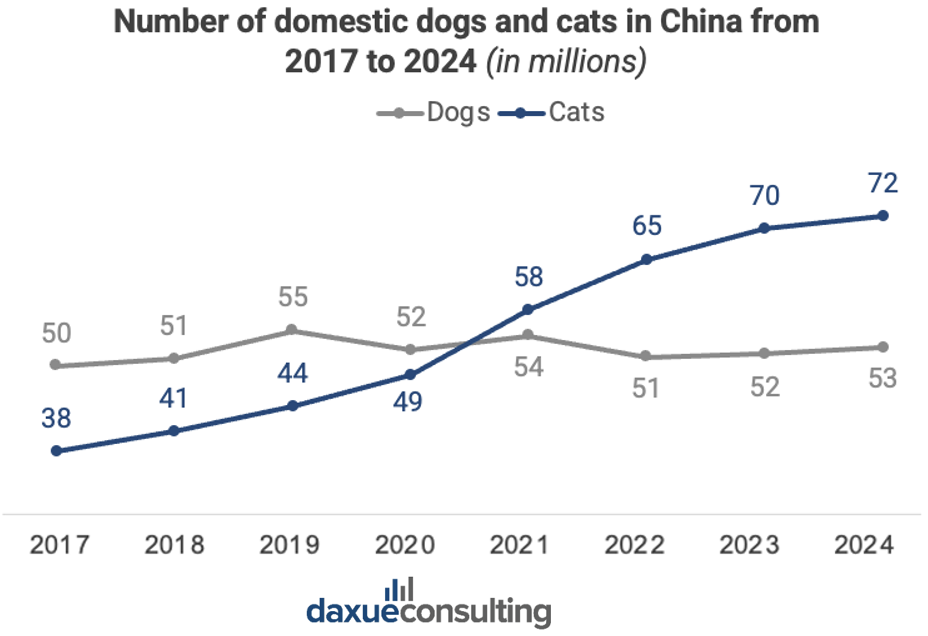

Cats take the lead: Shifting pet food demand

With dogs and cats representing the two largest consumer groups in 2023, the combined market size for dog and cat food reached RMB 144 billion. While dog food once dominated the segment, recent years have seen a notable shift: cat food consumption has now surpassed dog food.

This change mirrors broader pet ownership trends. In 2021, the number of domestic cats in China exceeded that of dogs for the first time, a turning point driven by urban lifestyles that favor lower-maintenance pets suited to smaller living spaces. By 2023, the cat food market reached RMB 74.8 billion with a year-over-year growth rate of 7.6%, outpacing dog food at RMB 71 billion and a 3.9% growth rate.

Notably, the annual spending per cat growth also exceeded that per dog for the first time: 2,020 RMB per cat, a 4.9% increase from 2023, compared to 2,961 RMB per dog, a 3% increase. This higher per-animal spending reflects greater attention to premium products, personalized nutrition, and functional foods that enhance feline health.

Domestic pet food companies are rapidly emerging and gradually taking the lead

Chinese brands are making notable gains in pet food. Brand loyalty is increasingly fluid: in 2024, nearly half of Chinese pet owners (47% dog owners, 48% cat owners) reported no strong brand preference. Crucially, a growing segment now exclusively chooses domestic brands (27% dog owners, 28% cat owners), surpassing those who exclusively buy foreign products (18% and 19%, respectively). Domestic brands are catching up with the quality of foreign brands and even more, they’re more affordable. Not only are domestic brands matching foreign quality—they also offer more competitive prices.

Many domestic companies are building competitive proprietary brands by utilizing experience gained from contract manufacturing and sustained R&D investments. In 2023, the market concentration among China’s top 20 pet food brands exceeded 30%, and among these top 20 brands, domestic brands accounted for approximately 55%, indicating further advancement in localization efforts.

Imported brands are gradually losing consumer trust due to price hikes and supply chain instability. Meanwhile, domestic premium products are closing the quality gap with imported counterparts—and even surpassing them—by leveraging scientific formulations and economies of scale to reduce costs, attracting more budget-conscious consumers.

Additionally, the government encourages enterprises to increase R&D investment and enhance product quality through policy guidance and technical support, thereby accelerating the development of domestic pet food brands. It has strengthened standardization efforts and feed supervision in the pet food sector, providing institutional safeguards for industry-wide quality improvement.

Decision-making process for pet food has become more complex

With increasingly diverse consumer demands and behaviors, the decision-making process for pet owners has become more complex. When selecting main meals for pets, nutritional balance, ingredient composition, and brand recognition remain the top three factors influencing their choices, accounting for 59.3%, 49.2%, and 29%, respectively. This also reflects that pet owners are increasingly prioritizing a product’s actual effectiveness, transparency, and cost-effectiveness when selecting their main pet food.

A taste for change among China’s pet owners

Chinese brands are making notable gains in pet food. Brand loyalty is increasingly fluid: in 2024, nearly half of Chinese pet owners (47% dog owners, 48% cat owners) report no strong brand preference. Crucially, a growing segment now exclusively chooses domestic brands (27% dog owners, 28% cat owners), surpassing those who exclusively buy foreign products (18% and 19%, respectively). Domestic brands are catching up with the quality of foreign brands and even more, they’re more affordable. Not only are domestic brands matching foreign quality—they also offer more competitive prices.

Consumer product preferences reflect a growing appetite for premium quality and specialization. Among cat owners in 2024, freeze-dried food was the most popular staple choice (49.7%), followed by baked dry food (43.7%) and extruded food (40.5%). Dog owners showed similar trends, with 43.8% preferring extruded food and 42.3% choosing freeze-dried options. These preferences underscore rising demand for high-quality, premium, and functional pet foods.

Beyond premium quality, consumers are also in search of innovative products that enhance their pets’ quality of life. For brands, this presents an opportunity to stand out in a saturated market. In 2023, several major players introduced cutting-edge offerings, Clearlake Capital Group launched a new line of supplements aimed at supporting dogs’ daily health, while ADM opened a new probiotics facility to boost the nutritional value of pet food.

The digital shift with e-commerce dominates sales channels

The way Chinese consumers shop for pet food is also shifting rapidly. In 2024, the total online sales of pet products across all platforms reached RMB 50.23 billion, marking a 10.0% year-on-year increase. Online channels have become the primary sales channel for pet food. Leveraging their significant advantages, large comprehensive e-commerce platforms have emerged as the top choice for pet owners, with a preference rate of 68.1% and live stream sales accounting for 18.9%. Pet owners now increasingly favor online shopping for its speed, convenience, and reduced physical effort.

Major platforms like JD.com and Tmall lead in online sales, while social commerce giants like Douyin are reshaping consumer engagement. During the 2024 Double 11 shopping festival, Tmall/Taobao’s pet category saw both total transaction volume and buyer numbers grow by over 50% year-on-year. Transaction volume for cat and dog food surged by more than 40%, while JD.com’s pet category recorded over 37% year-on-year growth in products exceeding one million orders. These two platforms captured 85% and 52.2% of consumer preference, respectively. Other major platforms like PDD, Douyin, and Xiaohongshu accounted for 32%, 25%, and 16.6% respectively.

Consumers turn to live stream shopping

Live stream shopping, emerging as a new e-commerce trend, has become a significant consumption method among pet owners in recent years. More than 50 live streams recorded sales exceeding RMB 1 million, and over 200 saw year-on-year growth rates above 100%. Data reveals that in 2024, Douyin topped the list with a preference rate of 78.6%, becoming the most favored live stream shopping channel for pet owners. Taobao Live followed with a preference rate of 64.7%, while JD Live ranked third at 37.9%. Consumers heavily depend on “authentic pet care share” and review videos from platforms like Xiaohongshu and Douyin to make decisions, forming a closed loop of “discovering, searching, and purchasing.”

Offline channels also contribute unique advantages to support the pet food market

Offline channels mainly include convenience stores, supermarkets, and specialty stores. The growth of these channels’ performance stems primarily from their precise targeting of consumer demands for immediacy, certainty, and expertise.

Although online platforms have taken on the primary purchasing function due to their convenience, extensive selection, and ease of price comparison, the value of offline pet stores or clinics lies in providing irreplaceable “professional services” and “immediate experiences” such as on-site consultations, physical examinations, and grooming. These are crucial for building a brand’s professional image and deepening engagement with high-value customers.

Insights that define China’s pet food momentum

- China’s pet food market is the largest and fastest-growing segment, accounting for over half of total pet-related spending in 2024. It’s no longer just about feeding pets, it’s about wellness, functionality, and lifestyle alignment.

- For the first time, cat food has overtaken dog food in both sales and growth. Urban living, smaller homes, and lifestyle preferences are pushing more consumers toward cat ownership and with that, feline-focused nutrition.

- Owners are seeking premium, functional, and health-enhancing pet food, especially freeze-dried, probiotic-rich, grain-free, and customized formulas. Innovation is key to capturing consumer attention.

- Nearly half of pet owners show no strong brand loyalty, signaling a more experimental market where product quality, ingredients, and innovation drive decisions more than legacy branding.

- Despite its growth, China’s pet food industry is still young compared to developed countries. This leaves room for rapid development, brand building, and long-term transformation.

- Although pet owners primarily purchase pet food through online channels and live streaming in China, offline channels continue to leverage their unique advantages to support China’s pet food market