Olive oil in China has long been called “liquid gold.” It is cold-pressed directly from fresh olives without heating or chemical processing, preserving its natural nutrients. Olive oil is considered one of the most nutritionally beneficial fats discovered to date. Primarily because it is rich in oleic acid, a monounsaturated fatty acid, which accounts for 71% of its total fat content. This component has been demonstrated in several large-scale scientific studies to possess anti-inflammatory properties. Thereby promoting heart and vascular health and even reducing the risk of type 2 diabetes. These health benefits have prompted consumers in the Chinese market to gradually experiment with alternatives to traditionally sourced, locally produced, low-cost peanut oil.

Download our China F&B White Paper

Consumption of olive oil in China

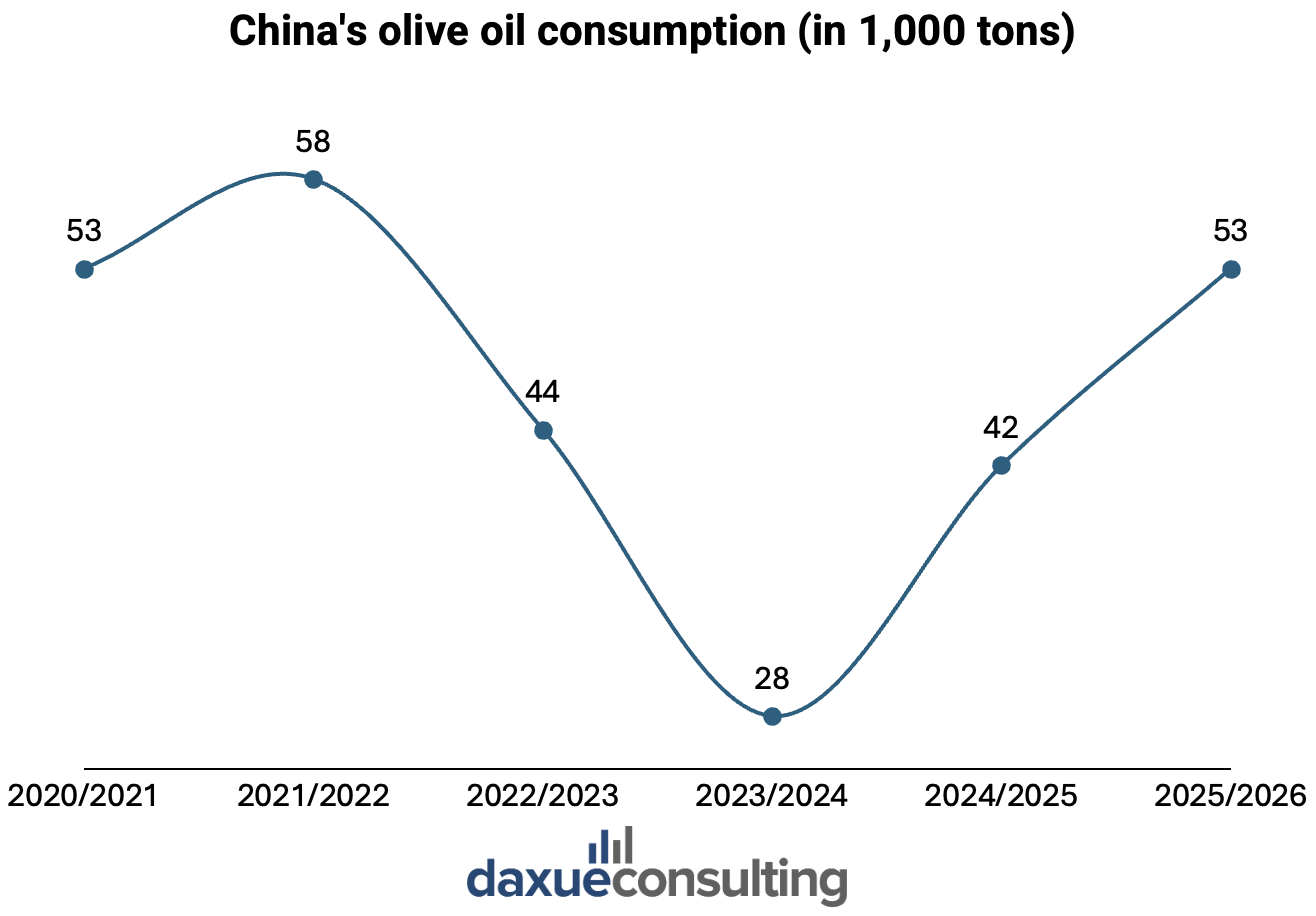

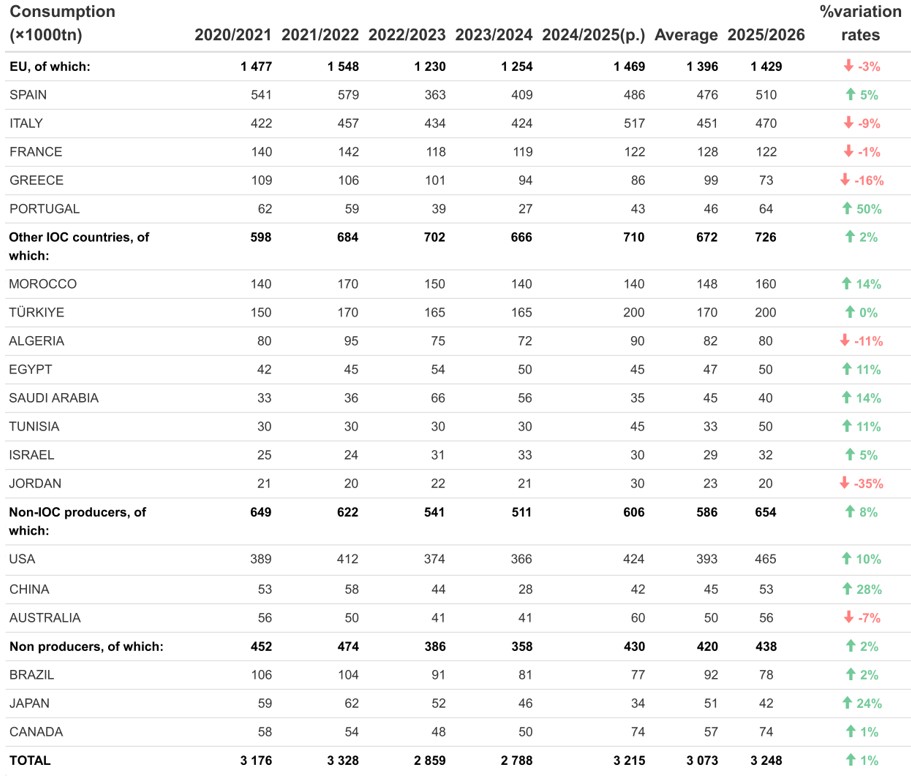

In the 2025/2026 crop year, the International Olive Council (IOC) estimated that China’s olive oil consumption reached 53,000 metric tons, an increase of 28% from the previous year. This figure is an estimate because the IOC uses the crop year as its measurement standard rather than the conventional calendar year. The final actual figure may fluctuate slightly. The olive oil market in China is projected to grow at a compound annual growth rate (CAGR) of 6.5% by 2030.

According to data from the Ministry of Agriculture and Rural Affairs, annual residential consumption of edible vegetable oils in China exceeds 34 million metric tons, indicating that olive oil still holds a very small share of the overall market. Peanut oil has long dominated the Chinese market for several reasons. On one hand, China is a major producer of peanuts with substantial domestic output. On the other hand, Chinese households frequently employ high-heat cooking methods such as stir-frying and deep-frying. Peanut oil is exceptionally well-suited due to its rich aroma and high smoke point. In this scenario, if olive oil consumption is calculated on a 1% share of the total market, it can still reach 340,000 metric tons, indicating significant room for growth.

Why does China’s low per capita olive oil consumption signal huge potential?

When comparing China’s market size to other non-IOC countries and non-olive oil-producing nations, it becomes apparent that while China lags slightly behind highly mature markets like the United States, the absolute market value gap is not substantial. However, total market size alone does not fully capture the maturity of olive oil consumption in China.

Given China’s large population base, per capita consumption offers a more revealing measure of how deeply olive oil has penetrated everyday dietary habits. It is noteworthy that China’s per capita olive oil consumption remains exceptionally low relative to its population size. Japan’s annual per capita consumption is approximately 0.4 kilograms, while Australia’s is approximately 1.9 kilograms per person. In contrast, China’s per capita olive oil consumption for the 2025/26 crop year is projected to be only about 0.038 kilograms per capita (based on China’s population of 1.408 billion). This relatively low per capita figure indicates that olive oil is still a long way from becoming a mainstream cooking oil in China and that it still possesses substantial room for growth.

How China is reducing reliance on imported olive oil

This is primarily because olive oil is not a traditional edible oil category in China. The industry’s origins trace back to 1964, when Zhou Enlai, then Premier of the State Council, personally planted an olive sapling imported from Albania. To this day, China’s olive oil consumption remains heavily reliant on imports. According to the latest customs data for 2025, China imported 40,000 metric tons of olive oil, a year-on-year increase of approximately 54% over 2024. Spain is the largest source of imports, accounting for 82%, while Italy contributes 13%.

This heavy import dependency has also led to supply chain instability. Spain, which supplies half of the world’s olive crop, experienced a severe drought in 2023, leading to a sharp decline in production. In the same year, China’s olive oil consumption stood at just 28,000 metric tons. The nation’s largest olive grove base is currently located in Longnan City, Gansu Province. During the 2024-2025 crop year, China produced a record 12,200 metric tons of olive oil, with Longnan accounting for 9,000 of that total. Overall, China is expected to gradually reduce its reliance on imported olive oil.

Olive oil consumption scenarios

The typical consumption scenario for olive oil is household health consumption, used to meet the health needs of specific groups. For household consumption, olive oil is typically used in two ways: cold applications and light heat cooking. Cold applications include salads, cold dishes, dipping bread, and light seasoning, while light-heat cooking includes stir-frying, medium-low-heat cooking, pasta preparation, soup making, and creating Western-style home-cooked meals. This is partly due to cultural perceptions.

Many Chinese still perceive olive oil primarily as a salad or cold-dish ingredient, rather than as suitable for stir-frying. This sentiment is echoed on Chinese social media platforms such as RedNote (Xiaohongshu). There are numerous posts that advise against using olive oil for stir-frying, claiming it may compromise flavor and degrade the oil’s nutritional value. This stems from a fundamental misunderstanding of oil properties. In reality, extra virgin olive oil has a smoke point of approximately 210°C (414°F). This makes it perfectly suitable for everyday stir-frying temperatures. Moreover, olive oil exhibits strong thermal stability. Its high content of monounsaturated fatty acids provides greater heat resistance than polyunsaturated fats. As such, olive oil is more tolerant of high temperatures. While some nutrient loss does occur during cooking, the degree of reduction is not particularly significant.

Price positioning of olive oil vs mainstream oils

On the other hand, olive oil also symbolizes a premium lifestyle. According to China’s 2024 import data, extra virgin olive oil imports amounted to approximately USD 145.1 million, with a volume of 15.1 million kilograms. Meanwhile, non-extra virgin olive oil imports totaled roughly USD 62.9 million, with a volume of 8.5 million kilograms. This translates to a pre-retail markup CIF import price of approximately USD 9.6 per kilogram (approx. RMB 66.24) for extra-virgin olive oil and USD 7.4 per kilogram (approx. RMB 51.06) for non-extra-virgin olive oil. Compared to peanut oil, China’s mainstream household cooking oil, these prices are significantly higher.

According to the U.S. Department of Agriculture’s Foreign Agricultural Service (USDA FAS) report, the wholesale market price for peanut oil in China during the 2024/25 crop year is RMB 15,500-17,000 per metric ton. This translates to a price of approximately RMB 15.5-17 per kilogram before accounting for retail markups, packaging costs, and distribution channel premiums. Soybean oil, another major household cooking oil, costs approximately RMB 12.4 per liter. It is evident that olive oil commands a significantly higher price than other mainstream cooking oils in the Chinese market.

Consumer perception of olive oil

Data indicates that among the edible oils selected by Chinese consumers in 2025, peanut oil leads with a 64.07% share, underscoring its foundational role in cooking. Soybean oil follows closely with a 46.29% share. Olive oil, representing the health-conscious segment, ranks third with a 36.45% share. Peanut oil remains popular among consumers due to its distinctive flavor and versatile culinary applications. The growing popularity of oils with clear health benefits, such as olive oil, reflects consumers’ increasing focus on dietary nutrition and wellness.

Which brands do Chinese consumers trust?

Olive oil faces a significant trust barrier in China, primarily manifested in adulteration, misleading “extra virgin” claims, and ambiguous labeling. A report revealed that during a 2025 anti-counterfeiting operation, 12 sampled products labeled “extra virgin” contained far less virgin olive oil than stated. Some low-priced items were blends of refined olive, canola, or sunflower oil. By sourcing inexpensive local refined oils and blending in minimal virgin oil upon return, this “one-drop-of-olive-oil” formula reduces costs to one-third of authentic virgin olive oil. As olive oil is a premium imported product, many Chinese consumers lack a full understanding of the distinctions among extra-virgin olive oil, virgin olive oil, refined olive oil, olive pomace oil, and blended oils. This gap between consumer perception and product reality makes it easier for low-cost sellers to exploit.

Several consumer websites list the most reputable brands currently available in China, including Olivoila (欧丽薇兰), Betis (贝蒂斯), Mueloliva (穆罗利瓦), Borges (伯爵/百格仕), Filippo Berio (翡丽百瑞), Bellina (蓓琳娜), Carbonell (康宝娜), Andalus (安达露西), Xiangyu(祥宇), and AGRIC (阿格利司). Olivoila is considered a leading brand in China for its import, sales, retail channels, and distribution points. Although most brands on the list are foreign, Olivoila is operated and distributed in the Chinese market by the local conglomerate Yihai Kerry. Consequently, it possesses robust local channel coverage and marketing capabilities. Yet, its product narrative still relies on Mediterranean ingredients, an imported brand image, or international olive oil standards.

What to know about China’s olive oil market?

- China’s olive oil consumption reached an estimated 53,000 metric tons in the 2025/26 crop year. However, it still represents only a very small share of China’s overall edible-oil market.

- The market still has strong upside because per capita olive oil consumption in China remains extremely low, well below that of mature markets such as Japan and Australia.

- Olive oil in China is primarily positioned as a health-focused, premium product, used in cold dishes, light cooking, and lifestyle-oriented household consumption. Due to its stable heat resistance, it is not unsuitable for stir-frying as rumored.

- China remains highly dependent on imports, especially from Spain and Italy. Meanwhile, domestic production in places like Longnan, Gansu, is gradually expanding.

- Despite rising consumer interest, the category still faces trust issues around adulteration, misleading “extra virgin” claims, and confusing labeling, which makes brand credibility especially important.

{kind=link}