As the country’s consumers are placing greater emphasis on self-care and long-term health maintenance, China’s eye-support supplements market is becoming a more visible part of the country’s preventive-wellness landscape. These supplements are positioned as a daily nutritional support for a range of eye-health needs. The category was expected to reach USD 97.3 million in 2025 and USD 149.2 million by 2030, reflecting a CAGR of 9.1%.

Eye-health pressure in China is becoming a cross-generational issue

China’s eye-health burden is becoming a cross-generational issue. A 2026 modeling study estimated that 32.42 million people aged 40 to 89 in China were living with age-related macular degeneration in 2020, with that number projected to rise to 40.4 million by 2030. Eye diseases progressively impair central vision and lack a definitive cure. As a result, early prevention is becoming more attractive to China’s aging consumers. This is especially true as eye health becomes increasingly tied to quality of life and independence in later years.

Additionally, digital saturation has contributed to a parallel rise in eye discomfort. Recent 2025 data indicate that asthenopia, or visual fatigue, affects 35.2% of Chinese adults. Meanwhile, dry eye disease, which is highly correlated with prolonged screen exposure, affects nearly one-third of the population. For working-age and middle-aged consumers, chronic eye strain is no longer a peripheral health issue, but a routine byproduct of screen-intensive daily life.

Transcending across ages: How eye issues affect children

Notably, this pressure is also extending to the youth in China. Under the country’s high-stakes education system, eyesight is closely linked to study performance. This makes visual health a household concern from an early age. However, a 2024 study of adolescents in eastern China found that 20.3% suffered from symptomatic dry eye. Compared with the 5.5% to 23.1% range reported in international pediatric dry-eye reviews, this places China near the upper end of the global spectrum. Taken together, these developments suggest that eye-health pressure in China has moved well beyond the boundaries of geriatric disease and is now becoming an everyday issue across all age groups.

China’s prevention agenda is supporting the demand

The rise of eye-support supplements in China is being driven by both top-down policy direction and an increasing consumer focus on personal wellness. Notably, China’s healthcare agenda has shifted toward prevention and daily health management. At the center of this shift is the renowned Healthy China 2030 framework, which shifted public health priorities from a purely treatment-centered model to a long-term maintenance model. This mandate is further reinforced by the 14th Five-Year National Eye Health Plan (2021–2025) and the Comprehensive Plan to Prevent and Control Myopia in Children and Adolescents. Both of which have raised the awareness of vision health protection as a proactive, lifelong responsibility rather than a reactive medical concern. Against this backdrop, eye-support supplements are gaining traction as a more systemic, “from-within” approach to eye care that aligns with consumers’ growing focus on long-term health maintenance.

Premium ingredients and new formats are reshaping category growth

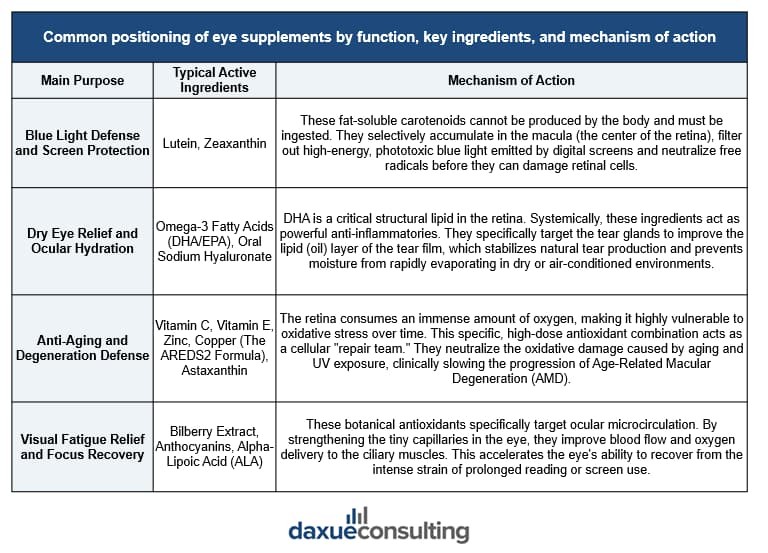

However, as the category gains broader acceptance, the growth of China’s eye-support supplement market is no longer accruing evenly across all products. Instead, competition is shifting toward formulations and formats that offer clearer differentiation. While traditional staples like lutein and blueberry maintain the highest consumer mindshare—capturing 47.5% and 26.1% of social mentions, respectively. This recognition no longer converts to sales. By the end of 2025, lutein sales had plummeted 21.6% compared to 2024, while blueberry-based products fell 28.7%. Such a decline signals that repeated ingredient claims are losing traction.

Notably, the growth engine has shifted toward premium anthocyanins and lifestyle-centric formats. Bilberry has emerged as the frontrunner, reaching RMB 300 million in sales (up 19.6%). The brand also command a RMB 159 average price point, a 50% premium over the market average. Meanwhile, this “value over volume” trend is mirrored in the “snackification” of the category. With traditional tablets declining, lutein gummies alone have already exceeded RMB 1.5 billion. Meanwhile, ready-to-drink formats have surged 87% by the end of 2025. Ultimately, the data signals a market prioritizing superior ingredient purity paired with low-friction, lifestyle-friendly delivery.

Translating formulation into familiarity

In China’s eye-support supplement market, the efficacy of products is difficult for consumers to verify immediately. Success, therefore, hinges on a brand’s ability to translate abstract ingredients into credible trust signals and tangible usage scenarios.

Swisse: Wellness as a Ritual

International leader Swisse leverages a premium, science-backed image to pivot eye care toward a lifestyle-oriented positioning that resonates with the modern consumer. Its lutein gummies exemplify this shift by prioritizing a frictionless user experience. By adopting a star-shaped, snack-like format and a pleasant taste, Swisse successfully transforms a clinical supplement into an indulgent “self-care ritual.” By merging functionality with high aesthetic appeal, Swisse has created a social-media-friendly “hero product” tailored for urban youth who demand emotional “premiumness” and a seamless fit into their daily digital lives.

BY-HEALTH: Wellness as a Result

Conversely, domestic giant BY-HEALTH (汤臣倍健) commands the market through local familiarity and a strategy rooted in direct functional authority. The brand builds rigorous consumer trust by foregrounding official regulatory approvals and translating complex technical specifications into intuitive, benefit-driven promises. A key element of this success is simplified education: by branding lutein esters as a “blue light filter.” The brand also highlights that its bilberry anthocyanin levels are “three to four times higher than ordinary berries.” As such, these marketing claims demystify technical formulations. This strategy connects scientific efficacy to tangible everyday concerns like visual fatigue and prolonged screen time, making the product’s value proposition feel concrete and dependable to a broad consumer base.

Taken together, competition within China’s eye-support supplement market is no longer just an “ingredient arms race.” While Swisse wins through lifestyle-led premiumization and emotional resonance, BY-HEALTH dominates through regulatory trust and benefit-oriented education. In both cases, the manufacturer sells the product as a “convincing explanation.” It links chemical compounds to the specific daily routines of the Chinese consumer.

How China’s eye-support supplement market is gaining ground

- China’s eye-support supplements market is gaining visibility as consumers pay more attention to self-care and long-term health maintenance.

- Demand is no longer driven only by aging-related concerns. It was also caused by screen fatigue, dry eye, and study-related visual stress affecting adults and younger consumers.

- Policy and public-health messaging are reinforcing prevention-focused demand.

- Although lutein and blueberries still have strong recognition, repeated claims are losing momentum as consumers look for more distinctive products.

- Bilberry, gummies, and ready-to-drink products show how the category is moving toward higher-value and more lifestyle-friendly propositions.

- Growth is increasingly shaped by clearer differentiation, stronger everyday relevance, and products that fit naturally into daily wellness habits.