According to Syntun, total online sales across all e-commerce platforms during the 2026 618 Shopping Festival totaled RMB 934 billion from May 13th to June 18th, representing slowed growth of 4% year-over-year. This shift is also evident in how brands are approaching the festival. Unlike in past years, major e-commerce platforms have generally stopped disclosing their total transaction volume and have instead begun disclosing structural metrics. Similarly, JD.com, the pioneer of the 618 Shopping Festival, has also canceled its June 18th promotional launch event, which has been held annually for many years.

Consumer sentiment also reflected the quieter atmosphere. The mention rate of “impulse buying driven by the atmosphere of major sales events” on social media dropped sharply from 21% to 7%. As a result, the 2026 618 Shopping Festival was described as “the most low-key and uneventful one in 16 years” (16年来最低调, 最平淡的一届). This transition is signaling a maturing market – one that values quality, efficiency, and consumer trust – driving brands to adopt winning strategies that look different from those of the past few years.

A quiet festival but not necessarily bad news

Although this was the quietest 618 Shopping Festival yet, consumer enthusiasm remained. During the festival, the average Daily Active Users (DAU) reached 700 million and reached a high of about 714 million during the peak June 16th to 18th period. Both were higher than the levels for the same period last year, suggesting that consumers remain engaged during the festival.

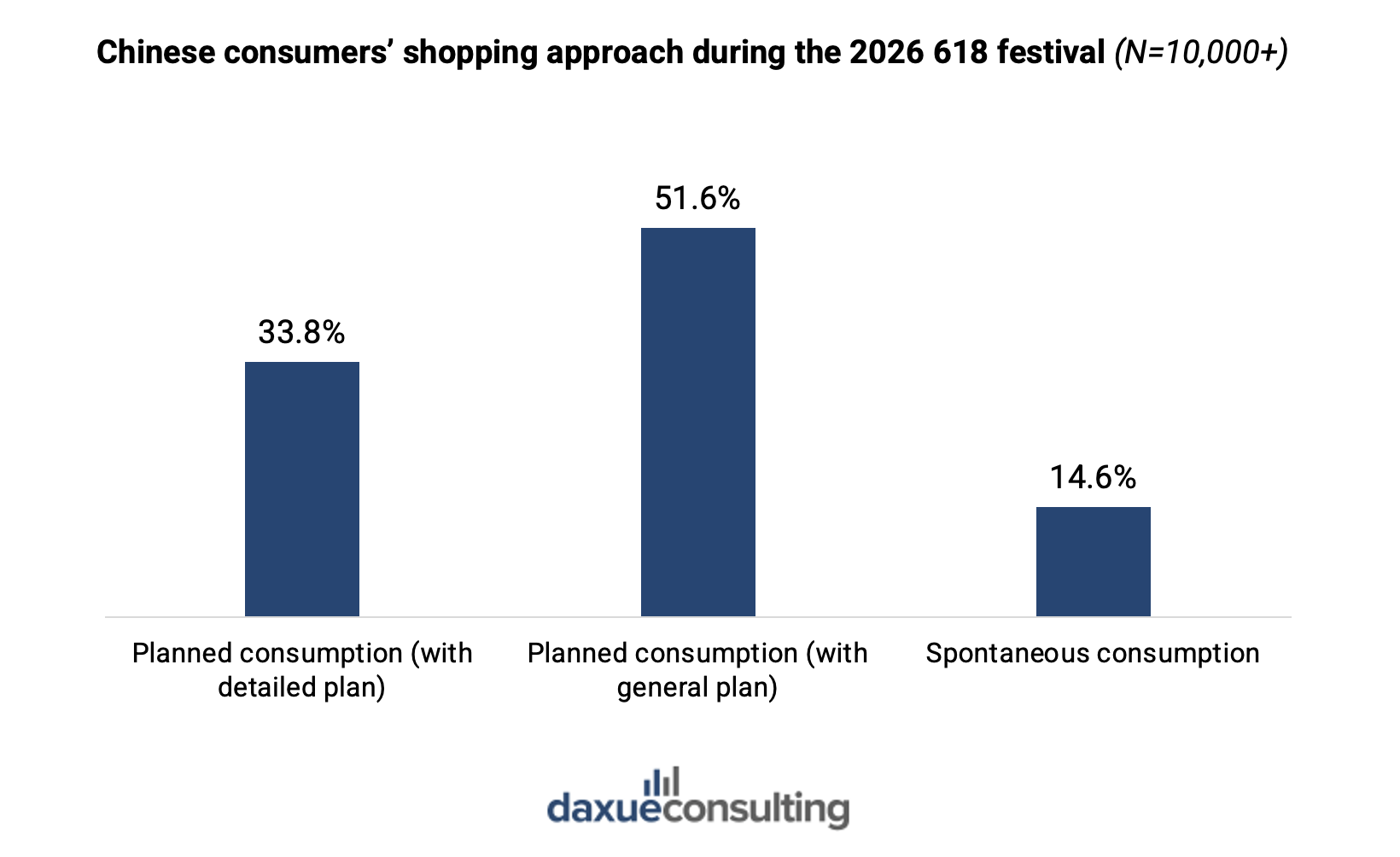

At the same time, consumers are becoming increasingly rational. Their consumption patterns are shifting from a simple pursuit of cost-effectiveness to a balance of quality and emotional value. According to a survey by the Daily Economic News among more than 10,000 respondents, 85.4% of consumers said they planned to make purchases in advance during the 618 Shopping Festival. 33.8% had a detailed shopping list, while some had a general shopping plan.

End of price wars and start of “value” wars

Platforms and brands are staying away from heavy discounts and focusing on profits. This shift is reinforced at the policy level: measures to combat unhealthy competition have curbed aggressive subsidy competition from the supply side. On June 11th, 2026, the Beijing Municipal Market Regulation Bureau conducted a meeting with five platforms, including Taobao, Tmall, JD.com, PDD, and Douyin, to discuss issues such as non-compliant promotional rules. This crackdown may be good news for foreign brands. They can compete more on brand equity and quality, areas where they often have a natural advantage, rather than purely on price.

The logistics sector was equally active. During the major sales event, nationwide express delivery pickups and deliveries increased by approximately 8% YoY. With penetration rates exceeding 87.8%, the industry’s room for growth has become extremely limited, and the focus of competition among platforms has shifted entirely from acquiring new customers to intensively managing the engagement and repeat purchase rates of existing users. This also explains why the e-commerce industry is undergoing a profound shift from pursuing sales volume to pursuing long-term customer value.

The top-performing categories during the 618 shopping festival in 2026

In 2026, the top products during the festival included the big-ticket items like home appliances. This was followed by beauty and skincare, personal care and household cleaning, food staples, cooking oils, and seasonings, nutrition and health supplements, fragrance and cosmetics, snacks, and pet food.

Despite ranking first, the home appliance category was also the primary drag on the overall festival’s growth. During China’s 618 2025, sales of home appliances were exceptionally strong thanks to the government’s trade-in subsidy policy, driving a significant 53% YoY increase in retail sales of home appliances and audio-visual equipment in May 2025. However, by May 2026, this category had declined by 15.6% year-over-year. Under pressure from a high base, the home appliance category struggled to maintain growth, which directly dragged down the overall performance of the major sales event, where home appliances were the core product category.

Beauty led by local and global brands, particularly in the prestige segment

Within the beauty and skincare segment, skincare sales totaled RMB 42.5 billion, RMB 24.2 billion in personal care, and RMB 13.6 billion in fragrance and color cosmetics.

The rankings were dominated by both local and global brands, especially those in the prestige segment. Top global brands included the long-time beauty leaders such as Estée Lauder, Lancôme, Helena Rubinstein, and La Mer.

Another brand that did well – especially compared to 2025 – was SkinCeuticals, known for its clinically backed formulations. The success of these brands highlights Chinese consumers’ demand for proven efficacy over brand heritage or price alone.

Rapidly growing demand for experiences

In addition to products, service consumption grew, increasing 10.7 percentage points faster than physical goods. The strongest performing category was online entertainment, with online retail sales increasing 55.9% year-over-year. This suggests that spending priorities are shifting away from material goods toward experiences, leisure, and quality of life.

The rise of the senior generation during the 618 shopping festival

As interest among younger generations approaches saturation or even begins to decline, the rise of the seniors in China has provided the industry with a rare source of new growth. Continuing on the 2025 618 shopping festival momentum, the senior generation has become the core growth segment for this year’s 618, with their engagement with 618 content rising to 25.2%. At the same time, interest among young people in small towns and the broader youth demographic, who have traditionally been considered the main drivers of the 618 shopping festival, fell to 37.8% and 29.2%, respectively.

Retailers face the dilemma of scale but no profits

Although the government has issued warnings to major e-commerce platforms, three major challenges, including automatic price matching, cross-platform price comparisons, and mandatory minimum pricing, continue to squeeze retailers’ profit margins. High advertising costs and persistently high return rates have further exacerbated losses. Return rates for women’s clothing during major sales events typically reach as high as 80% to 90% , a figure that has persisted for several years, continuing to erode margins. Also, in beauty cosmetic live stream sales, it has become the norm for influencers’ commissions to account for 30% to 50% of a brand’s sales. Compounded by high advertising costs and high return rates, many brands have found themselves in a dilemma where “the more they sell, the more they lose.”

As a result, faced with steadily rising advertising costs, more and more brands are beginning to cut back on their advertising budgets. Meanwhile, retailers are gradually realizing that high repurchase rates and low return rates are the foundation for achieving reasonable profits and sustainable operations on e-commerce platforms. The beauty brand Marumi Bio has shifted its focus entirely toward profitability, prioritizing stable growth in its high-margin e-commerce platform business while scaling back loss-making segments in its content-driven e-commerce operations.

The shift in retailers’ business mindset toward prioritizing profits has directly led to a realignment of their channel strategies. A growing number of brands are shifting back from content-driven e-commerce to shelf-based e-commerce. During the 618 shopping festival in 2026, some leading brands increased their budgets for shelf-based e-commerce platforms like JD.com by 5% to 15% compared to 2025. For example, the laundry and personal care brand Blue Moon and the skincare brand KANS proactively cut back on their investments in influencer live streaming in China and redirected more of their budget to e-commerce platforms.

618 extends beyond China

Overseas markets are showing unprecedented enthusiasm for this Chinese shopping festival. During the 2026 618 shopping festival, AliExpress, Alibaba’s cross-border e-commerce platform, focused its efforts on overseas markets. AliExpress partnered with more than 100 international influencers in 14 countries, including Spain, France, Italy, Germany, and the United States, to host over 100 live streaming events for more than 60 Chinese brands. JD.com Global also experienced explosive growth during the 2026 618 shopping festival. Within 52 hours of the event’s launch, the platform’s total overseas order volume doubled YoY, while overseas orders from third-party retailers on the platform more than tripled YoY. Orders surged in popular overseas markets such as Singapore, Malaysia, and Vietnam, with YoY growth exceeding 200% in many regions.

In addition, ahead of this year’s 618 shopping festival, more than 600 new overseas brands from 29 countries and regions around the world opened their first stores on Tmall Global, with the United States, South Korea, Japan, France, and Australia ranking as the top five countries in terms of the number of new brands joining the platform. At the same time, Weverse Shop, a South Korean platform for selling K-pop celebrity merchandise, held its first-ever 618 shopping festival promotion in China, becoming a pioneer among overseas platforms participating in the 618 shopping festival.

What the 2026 618 shopping festival shows about Chinese consumers

- During the 2026 618 shopping festival, sales across all e-commerce platforms totaled RMB 934 billion, a 4% year-over-year growth. Despite being described as “the quietest one in 16 years,” consumers continued to show engagement – just less impulsively.

- Chinese consumers are making more rational, planned purchases. 85.4% of consumers said they planned to make planned purchases during the 618 Shopping Festival instead of buying out of impulse.

- The Chinese silver generation is emerging as an untapped key source of growth.

- Scale doesn’t guarantee profit. Retailers face margin-crushing pressure from price-matching rules, pushing brands to reallocate their budget away from influencer-driven content commerce to traditional e-commerce platforms.

- Overseas markets are also heating up, and the global impact of the 618 shopping festival is becoming evident.

Author: Sory Park