China’s tea market has a long history, with exports dating back to the Northern and Southern Dynasties. Today, China stands as the largest tea market globally, serving as both the biggest consumer and producer of tea. In 2024, domestic tea sales in China reached 2.4 million tons, accounting for around 69% of the country’s total tea production. This figure underscores the industry’s self-sufficiency and strong emphasis on domestic consumption. However, tea alone is not enough to drive consumption among Chinese consumers today. Instead, distinct, fresh, cultural, and wellness-driven experiences are what drive people toward certain brands.

Download our China’s F&B industry white paper

Segments in China’s tea industry

China’s tea industry primarily consists of three segments:

- Traditional loose-leaf tea dominates in volume and value, with major subtypes such as green, oolong, black, and pu’er tea.

- Ready-to-drink bottled tea continues to experience robust growth, driven by convenience and innovation, particularly among urban youth.

- New-style tea (新茶饮) has emerged as a runaway success, disrupting consumption channels and shaping taste preferences.

Youth in emerging-tier cities as the core growth engine

Across city tiers, the fastest growth in tea consumption is coming from emerging-tier cities and younger consumers, especially within the new-style and freshly made tea segment. In 2023, retail sales of new-style tea shops in third-tier and lower-tier cities exceeded RMB 96 billion, compared to approximately RMB 34 billion in first-tier cities, and are projected to grow faster than higher-tier markets over the next five years. Consumers in tiers 3-5 (home to over 70% of China’s population) are driving a wave of “accessible indulgence,” where affordable tea drinks at RMB 5-15 become a daily emotional reward for younger consumers.

Core drivers of tea consumption in China

Tea is closely linked to “health” in the Chinese context, often prioritized above coffee as a functional beverage. Buzzwords like “zero sugar, zero calories” and traditional Chinese medicine concepts, such as combating internal dampness, resonate strongly with younger consumers seeking guilt-free refreshment.

Beyond product novelty, new-style tea succeeds because it taps into a uniquely “experiential consumption” space that coffee and other beverages cannot fully replicate. Tea carries strong cultural associations with comfort, balance, and wellness. Younger consumers interpret tea as a lighter and more versatile alternative. This flexibility allows tea to serve both daily refreshment and emotional reward needs, making it naturally suited to high-frequency consumption.

Moreover, storytelling and cultural collaborations drive young consumers toward certain brands. Given China’s very competitive tea industry, products alone are not enough to capture consumer attention. Instead, brands compete through unique experiences. They use limited-edition releases tied to Chinese festivals, intangible cultural heritage, or local artists to express tea’s cultural depth in contemporary forms. These campaigns help young consumers experience tea as something meaningful and rooted in identity, while still being fun and easy to consume.

Why health-minded youth still prefer new-style tea over traditional loose-leaf

Although traditional loose-leaf tea is often regarded as a healthier option, many young consumers find it inconvenient and difficult to incorporate into their daily lives. Loose-leaf tea often requires specialized equipment, brewing knowledge, and a slower, more ceremonial preparation process that does not align with their fast-paced routines.

New-style tea offers a more accessible entry point. It comes in ready-made formats and customizable options that feel both healthier and more fun. The rise of lower-sugar and sugar-free innovations also helps these drinks fit youth wellness priorities. Additionally, sugar-free ready-to-drink brands, such as Oriental Leaf and Genki Forest, have reinforced this perception by promoting clean-label teas through highly visible digital channels.

As a result, young Chinese consumers associate new-style and ready-to-drink teas with a more accessible form of “healthy indulgence,” which better aligns with their lifestyles than traditional loose-leaf tea.

Premium tea’s growth and its structural weak spots

China’s traditional loose-leaf tea market continues to expand steadily across all price segments, with total market size rising by 12.8% from 2020 to 2024. Traditional loose-leaf tea in China’s tea market shows distinct tiered segmentation, categorized by price into mass-market tea (below RMB 300/kg), mid-range tea (RMB 300-700/kg), and premium tea (above RMB 700/kg), catering respectively to daily consumption, value-for-money demands, and high-end business scenarios.

While premium tea accounted for roughly 30% of the total market from 2020 to 2024, it’s growing the fastest in absolute value. This reflects rising demand for higher-quality products and gifting occasions, while mass-market tea remains the largest segment due to its everyday use and broad consumer base. Mid-range tea shows stable but slower growth, suggesting that consumers are gradually polarizing toward either affordable daily-drinking options or more premium offerings.

As a non-standardized agricultural product, tea imposes high learning costs on consumers. Branding has become crucial for reducing trust costs. However, the midstream of the industry remains highly fragmented, with over 70,000 tea enterprises nationwide, most of them small, scattered workshops. In 2024, the concentration ratio of the top five players in the high-end tea market stood at only 5.6%, highlighting a pronounced “heavy emphasis on production origin, light emphasis on brand” phenomenon.

Limited youth engagement

Premium tea brands often fail to resonate strongly with younger consumers. Chinese Gen Z participates most actively in new-style tea experiences. Premium tea’s focus on traditional formats and ceremonies doesn’t always appeal to this group’s lifestyle or purchasing habits. Additionally, the focus on gifting makes premium tea less relevant for spontaneous purchases and casual enjoyment, often discouraging trial among those who value functional benefits or digital engagement over ceremonial consumption.

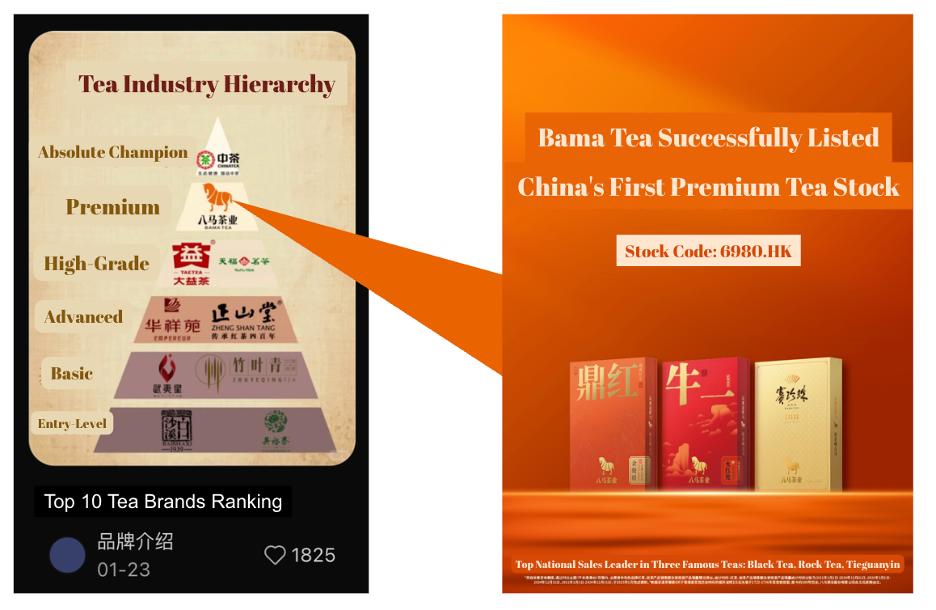

The nationwide expansion of Bama Tea, a leading Chinese premium tea

Bama Tea launched its IPO on the Hong Kong Exchange, signaling a new chapter for both the brand and the broader industry—one where strong branding finally rivals strong categories. It represents the modernization of China’s premium loose-leaf tea segment because it brings together strong origin credibility, category leadership, and a scalable national brand, something rare in China’s tea market, which is still dominated by small regional workshops. Its core products are positioned well above mid-range tea pricing, and its consistent quality has helped Bama establish a nationwide presence that few premium tea brands have achieved.

Expansion beyond tier-1 cities

From 2,613 stores in 2022 to 3,633 in 2025, Bama’s chain expansion is most pronounced in tier-2 and tier-3 cities, affirming that deep-seated tea culture and rising middle-class aspirations extend well beyond China’s megacities. This decentralization of growth highlights tea’s integral role in everyday Chinese life and points to new regional opportunities.

Key takeaways in China’s tea market:

- China’s tea market is driven by strong domestic demand and self-sufficiency, with ongoing growth led by new-style tea innovation and premiumization.

- Premium tea is expanding rapidly, but faces challenges from market fragmentation, weak youth engagement, and the limitations of traditional gifting-driven business models. Stronger branding and digital engagement are critical for future success.

- New-style tea brands thrive by pairing product innovation with collaborative storytelling, using cultural tie-ins, seasonal releases, and interactive marketing to win over younger, urban consumers. Health-driven preferences, regional identity, and convenience define the fastest-growing segments.

- Winning brands blend tradition and modernity, adapting formats and experiences for China’s diverse city tiers.

- The next wave of growth will depend on companies that balance deep tea heritage with contemporary branding, digital agility, and inclusive experiences across all age groups and regions.