A young consumer in China buying a gold bracelet today is not necessarily preparing for marriage or investment. Instead, the purchase may be driven by something less tangible: a sense of identity, a desire for self-expression, or even the belief that a small charm can bring good fortune. The meaning attached to jewelry is becoming more personal and less tied to traditional milestones. This subtle shift reflects a broader transformation in consumer behavior where emotional value and everyday expression are becoming increasingly important.

The Chinese jewelry market remains large and steadily growing within the global landscape

The Chinese jewelry market reached USD 94.1 billion in 2025. It is projected to grow to USD 144.8 billion by 2033, reflecting a CAGR of 5.7% over the period. In the same year, China accounted for 24.7% of the global jewelry market. This secures its position as one of the largest contributors to global industry revenue. Compared with China’s expected long-term GDP growth of around 4–5%, the jewelry market’s projected expansion indicates that the category is broadly keeping pace with, and in some cases slightly outpacing, overall economic growth.

In comparison with other major markets, where jewelry demand tends to grow at a slower rate due to higher maturity, China’s 5.7% CAGR reflects a relatively stable expansion trajectory. The combination of large market size and continued growth suggests that China remains a key driver of global jewelry demand, while ongoing expansion indicates that the market has not yet reached saturation.

A highly concentrated material structure alongside diversified product preferences

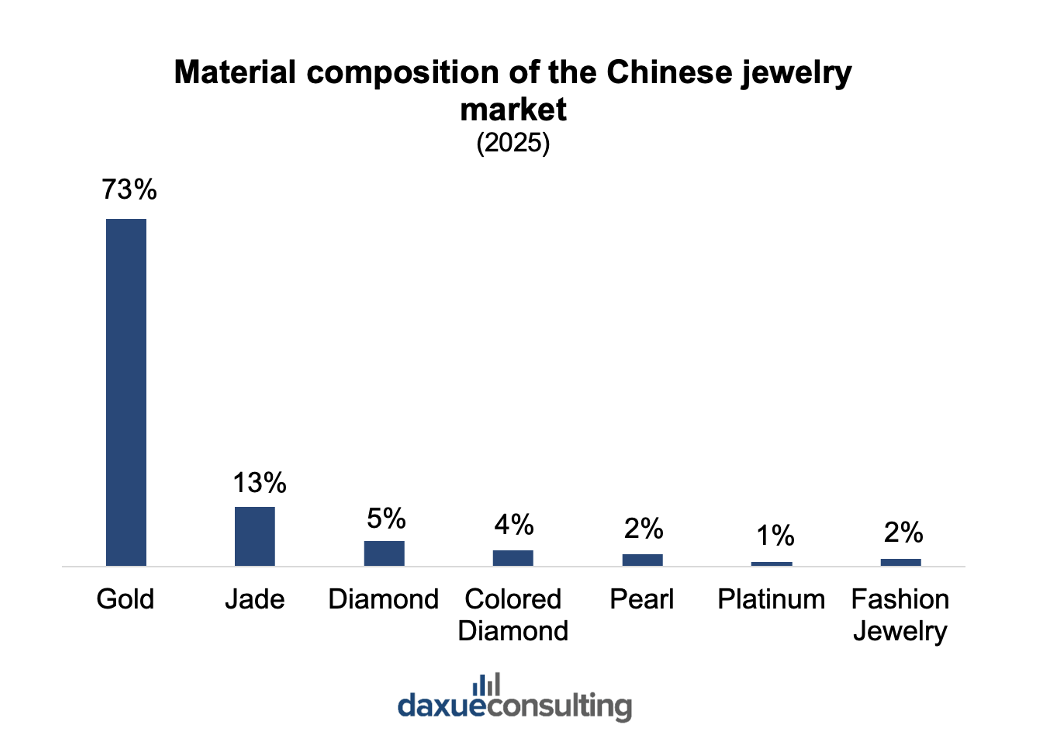

From a material perspective, the Chinese jewelry market is highly concentrated in gold. Gold products account for approximately RMB 568.8 billion, or 73.0% of the total market. This far exceeds other categories such as jade (12.6%) and diamonds (5.5%). Other segments, such as colored gemstones, pearls, and platinum/silver, each contribute less than 4%, with fashion jewelry and other categories making up around 1.7%.

This dominance reflects both cultural preference and financial considerations. In China, gold jewelry is not only worn for decoration but also viewed as a form of asset preservation, as it can be resold and tends to retain value better than other materials. At the same time, the presence of smaller categories suggests that demand is gradually diversifying. Consumers are showing increasing interest in non-gold materials despite their relatively limited share.

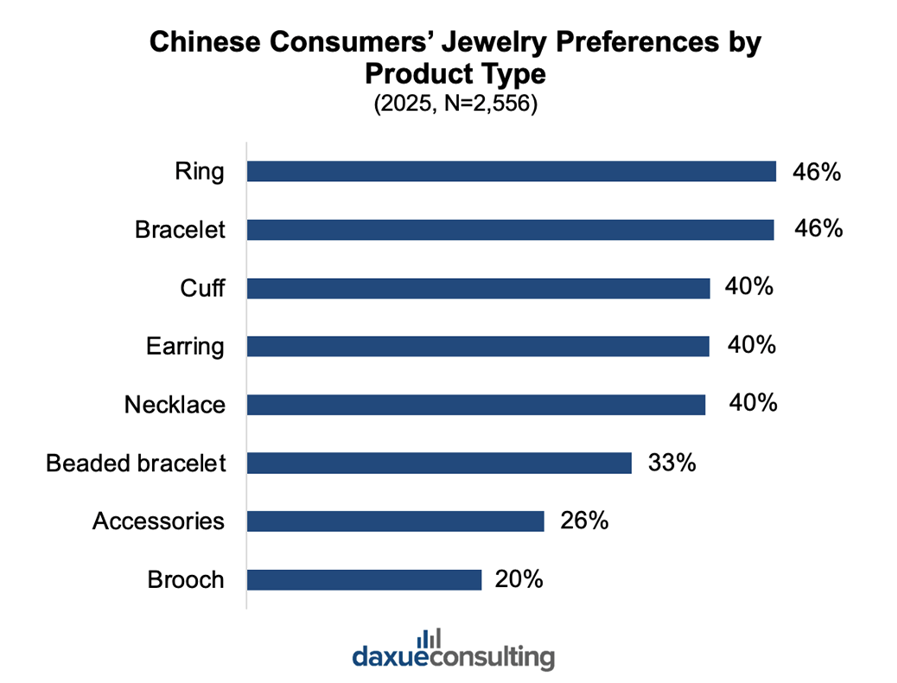

According to a survey in 2025 (N=2556), purchases are more evenly distributed across categories from a product type perspective. Rings (45.85%) and bracelets (45.62%) lead, followed closely by necklaces (40.14%) and earrings (40.06%), with pendants at 39.75%. Other categories, such as brooches and anklets, remain below 30%.

The relatively small differences across major product types indicate that jewelry consumption is not concentrated around a single category or occasion. While rings show a slightly higher share, the overall balanced distribution suggests that jewelry is increasingly used for everyday styling and personal expression. It was no longer primarily tied to weddings or relationship-related purchases.

Functional preferences and market structure together shape Chinese jewelry consumption

Consumer decision-making in the Chinese jewelry market reflects increasingly diverse and individualized preferences. In 2025, 39.75% of consumers (N=2556) cited alignment with personal style as the most important factor. It was followed by material (37.95%) and design (36.93%). Price (36.54%) and quality (34.90%) remain key considerations. However, craftsmanship (33.65%) and brand (31.69%) play a secondary role. This distribution suggests that purchasing decisions are not driven by a single dominant factor, but rather by a combination of personal preference and product attributes. The emphasis on style and design indicates that jewelry is increasingly selected for self-consumption. As such, individual expression and everyday wear matter more than traditional functions such as gifting or investment.

At the same time, the competitive structure of the market reinforces these dynamics. The Chinese jewelry market remains highly fragmented. The top five companies accounted for only 30.3% of the total market share in 2024. Leading players such as Chow Tai Fook, Lao Feng Xiang, Shanghai Laomiao Gold, Chow Sang Sang, and Mengjinyuan are all domestic brands. Due to design preference, local jewelry companies have consistently dominated both the CR5 and the majority of the CR10 in recent years. Compared with more mature markets such as Japan and the UK, where industry concentration is higher, China’s lower level of consolidation suggests a more competitive and less saturated landscape.

Taken together, the diversity in consumer preferences and the fragmented market structure indicate that there is still considerable room for new entrants. In particular, the growing importance of design and styling highlights opportunities for brands. Successful brands differentiate through product aesthetics and positioning, rather than relying solely on material value or brand heritage.

Gen Z is redefining jewelry consumption through emotional value and cultural meaning

Building on this shift toward self-driven and design-oriented consumption, Gen Z has emerged as a key force further shaping the market. Consumers under the age of 35 now account for more than 55% of total demand. Over 60% of purchases are made for self-consumption. This reinforces the transition from jewelry as a ceremonial or investment product to one that is embedded in everyday life and personal expression. Compared with previous generations, Gen Z consumers are more likely to associate jewelry with identity, emotion, and daily styling rather than specific life events.

This shift is closely reflected in design preferences. In 2025, symbolic and text-based elements ranked as the most popular design category, selected by 45.23% of consumers. This was followed by abstract patterns (41.86%) and natural elements (41.47%). Compared with purely decorative or IP-driven designs, these categories allow for greater interpretation and personalization. At the same time, more than half of Gen Z consumers report that Chinese-style designs better reflect their personal values. This reinforces the growing relevance of culturally embedded aesthetics. Traditional motifs such as gourds, Pixiu, zodiac signs, and lotus patterns have gained popularity as they carry associations with luck, prosperity, and protection.

These trends highlight the increasing importance of emotional value in jewelry consumption. Around 86% of Gen Z consumers consider the symbolic or “energy” meaning of jewelry when making purchasing decisions. This suggests that products are evaluated not only for their visual appeal but also for the meanings they convey. In this context, jewelry functions as a medium for emotional expression and psychological reassurance. The cultural symbols and design elements serve as a way for consumers to project personal beliefs and narratives into everyday consumption.

From value to meaning: How Chinese consumers are redefining jewelry

- Jewelry in China is increasingly purchased as a form of personal expression. This reflects identity and individual taste rather than traditional expectations.

- Consumption is becoming more everyday-oriented. Buyers are integrating jewelry into daily styling instead of reserving it for special occasions.

- Emotional and symbolic value play a growing role. Chinese consumers associate jewelry pieces with luck, beliefs, or personal narratives.

- Preferences are spread across multiple product types, suggesting no single dominant category and a more versatile usage pattern.

- Overall demand is shaped by a mix of aesthetic appeal and personal relevance, highlighting a shift toward more individualized consumption.