China’s jewelry market is undergoing a significant transformation as younger consumers and low-tier cities are emerging as key drivers of growth. Millennials and Gen-Zs are reshaping the local jewelry market by showing a strong preference for gold jewelry over traditional silver and diamond options. This shift in consumer behavior has prompted established jewelry brands to revamp their product lines and marketing strategies to cater to the evolving tastes and preferences of this new generation of consumers.

Additionally, the growing prosperity of China’s lower-tier cities has opened up new opportunities for jewelry brands to expand their reach and tap into previously untapped markets. As a result, understanding the changing dynamics of the Chinese jewelry market has become crucial for both established brands and emerging players seeking to capitalize on this fast-evolving market.

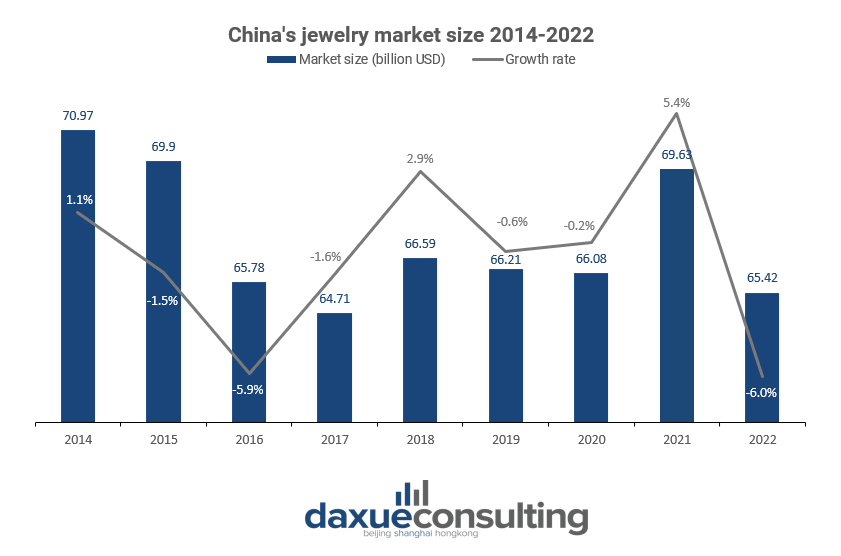

In 2021, China had the largest jewelry market in the world, accounting for 27.2% of the global share. Jewelry sales in China mostly followed the household disposable income which has been growing relentlessly since 2010, leading the best-off class to increase elevenfold between 2010 and 2020.

Three players in the jewelry market in China

There are three distinct players in China’s jewelry market: world-renowned brands, Hong Kong brands and Chinese mainland brands. Foreign companies like Cartier, Swarovski and Van Cleef & Arpels dominate the premium high-end market in higher-tier cities, with prices generally higher than those of domestic brands. Hong Kong and mainland brands, on the other hand, compete in the high and medium-end markets. While Chinese domestic jewelry companies are younger than their international counterparts, typically with no more than a hundred years of history, they offer more affordable prices.

Leading companies like the Chow Tai Fook Group implement a multi-brand strategy to build a high-end jewelry brand image. Jewelria, for example, is a brand of the Chow Tai Fook group which targets high-income people and only has stores in a few first-tier cities. Meanwhile, new domestic brands, such as YIN, I Do and Qeelin, are gaining ground by targeting previously overlooked customer segments, particularly younger demographics. However, branded jewelry still only accounts for 15% of the Chinese jewelry market, indicating plenty of room for new players to enter the market.

China’s jewelry market in first, second, and third-tier cities

As the Chinese jewelry market reaches maturity in first- and second-tier cities, jewelry companies are turning to third-tier cities as the key engine of growth. The population growth rate in low tier-cities has doubled over the last 10 years and the total population in third-tier cities is five times larger than in first-tier cities. The increasing purchasing power of second- and third-tier cities is driving demand for jewelry in China and prompting store expansion in these areas.

Lukfook and Chow Tai Fook have the largest number of stores in mainland China, with Lukfook opening about 280 new stores in lower-tier cities between 2013 and 2017, while Chow Tai Fook focused on second-tier cities with around 500 new stores. Foreign brands like Cartier are also expanding in second-tier cities.

However, the market in first-tier cities remains significant, and jewelry houses continue to invest in upgrading their positioning and branding strategies to meet the needs of their most sophisticated customers.

What’s new on China’s diamond market

According to the Gems & Jewelry Trade Association of China, China’s diamond jewelry market reached 12.4 billion USD in 2021. China has steadily held the position as the world’s second-largest diamond market for over a decade, preceded only by the US. According to diamonds.net, between 2002 and 2018, the import of net polished diamonds through the Shanghai Diamond Exchange recorded an astonishing annual increase of about 27%. As younger generations impose themselves as the main drivers of national consumption, China’s diamond market boasts great potential for growth —according to both McKinsey and Bain, China will account for roughly half of all global luxury spending by 2025.

Although diamond jewels are increasing their share in the bridal market, as Gen-Z consumers become the main group of newlyweds and domestic marriage rate declines, the non-bridal segment is bound to play a major role in boosting the demand for jewelry goods. Thus, brands like I Do are now attempting to widen their audience, conveying the idea that diamonds are not just for weddings.

Single women, men and children: long overlooked consumer groups steal the spotlight

Highly educated women in higher-tier cities are a significant consumer group in the jewelry market in China. Unlike Westerners, Chinese men also show great appetite for diamonds and jewelry in China. In fact, according to a 2019 survey by the Hong Kong Trade Development council, 67% of Chinese male consumers aged 30-44 expressed a desire to own diamonds.

In accordance with Chinese traditions, people give longevity locks, bracelets, and necklaces to children as lucky charms as well as a way of wishing them a healthy and happy life. In particular, gold jewelry items are the top choice among parents concerned about family’s future financial situation due to their inflation-proof value. Many companies have launched children’s collections, such as Chow Tai Fook’s collaboration with Disney and Marvel for its baby gift sets.

Smart jewelry in China’s jewelry market

Smart jewelry is a growing trend in China’s jewelry market. With the rise of wearable technology, consumers are increasingly interested in jewelry that serves a dual purpose – not only as an accessory but also as a smart device. Smart jewelry can track fitness goals, monitor health, and even provide notifications from your phone. Domestic brands such as Ringo and Unicmi have already entered the market with their own smart jewelry products, while international brands like Swarovski and Misfit are also tapping into this emerging market. The potential for smart jewelry in China is vast, with consumers looking for innovative and convenient ways to incorporate technology into their everyday lives.

E-commerce and O2O interaction keep on reshaping the industry

In China, the digital world has become an integral part of the luxury consumer’s journey. McKinsey reports that around 60% of touchpoints are digital in China, but customers still prefer to gather information online then purchase them in physical stores, which include display counters in shopping malls, specialty stores and experiential stores. Nevertheless, independent shops, chain stores and e-commerce are gradually gaining ground.

E-commerce players such as Zbird display sample products in their physical stores and keep limited inventory, while customers can place orders via in-store tablets, their own mobile devices, or store clerks. Retailers keep their most expensive items in physical stores, as customers prefer to see and try them before spending large amounts of money on jewelry in China.

Social media as efficient channels to engage with customers

Most major players in China have their own Tmall and JD flagship stores, while WeChat and VIP are the most popular social-media platforms where users can have access to jewelry products. WeChat maintains its position as the most popular Chinese social media platform with 1.3 billion monthly active users in 2022.

Jewelry houses rely on Tencent’s multifunctional app for their O2O strategy in China, with Cartier being the first luxury jewelry brand to use WeChat moments ads. For 2023 Valentine’s Day, the brand launched a limited-edition red gift box on its WeChat store, containing rings, perfume, accessories, and handbags. With over 300k views on the gift box social media posts, Cartier increased Chinese consumer desire for its products and its luxury limited-edition presentation.

Besides WeChat, Weibo and Douyin are also witnessing a major increase in the number of jewelry brands running a flagship store on the platforms. As of March 2023, domestic jewelry brand I DO boasts 300k fans on Douyin, making it one of the most popular national jewelry houses on the platform. Some of I DO’s most popular Douyin posts with over 2 million views are of romantic wedding proposals with a I DO ring.

Moreover, live-streaming sales has become increasingly popular for all major jewelry brands. Jewelry was the top category in terms of live-streaming seller transaction volume in 2021.

Jewels have a great story to tell

The jewelry market in China is constantly evolving to meet the needs of younger, customization-demanding consumers. Key players are enhancing their O2O strategy by integrating online and offline features to improve the customer experience. For instance, LVMH-owned Chaumet allows customers to measure their finger sizes in 360 degrees on their mini program, while Cartier offers tailor-made services like engraving, gift-wrapping, and white-glove delivery services via Tmall.

Moreover, jewelry houses rely on storytelling to stand out from the crowd and catch consumers’ attention. Foreign brands emphasize their long history and deep-rooted legacy, while Chinese brands focus on design, social commitment, quality of raw materials, and cost-effectiveness. Additionally, classic pieces from big names are seen as ever-green and versatile, while domestic brands provide younger, more fashion-forward jewelry to target Gen-Z consumers, as seen with WBJ and YIN.

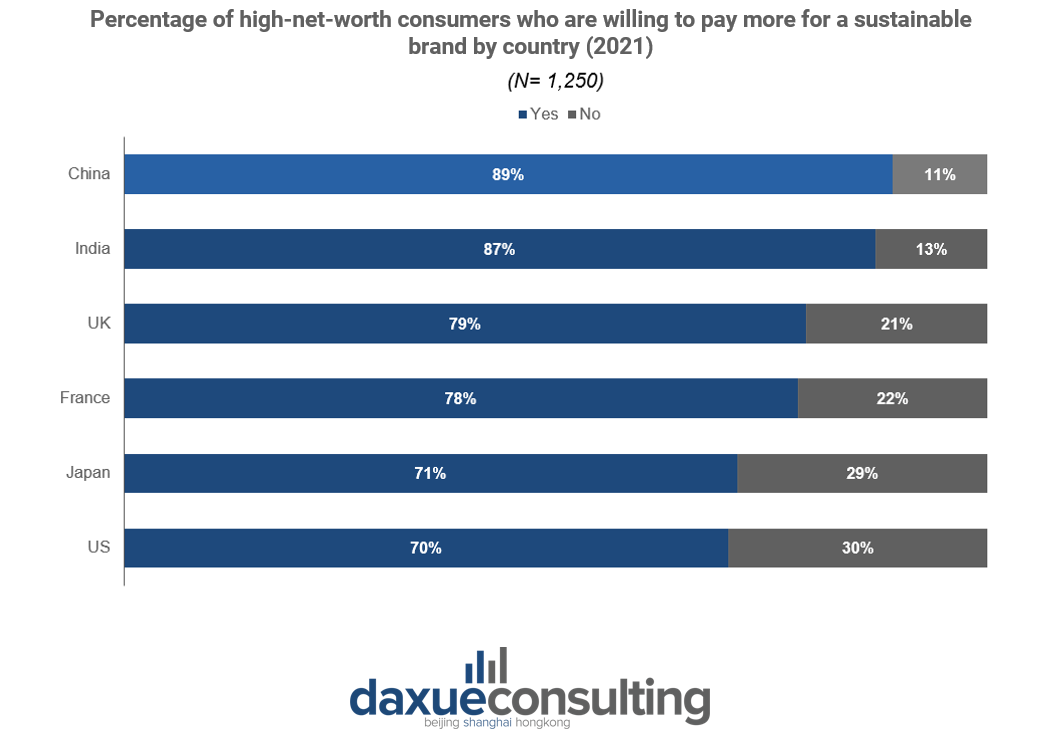

Sustainability is also a growing concern for high-end luxury consumers in China. A study by Agility TrendLens 2021 found that 88% of Chinese high-end jewelry consumers take brands’ social responsibility seriously when purchasing luxury goods, with 89% willing to pay a premium for sustainable and eco-friendly products. This trend extends to China’s diamond market, with 56% of respondents open to paying between 10% and 20% more for a sustainable diamond.

While there is still a bias against artificial diamonds, moissanite diamonds are becoming increasingly popular among Chinese Gen-Z consumers. This is because young couples are looking for more cost-effective options for their weddings, and lab-grown gems offer a more affordable choice. The pandemic has accelerated this trend, as couples prefer to allocate their money to other commodities.

Today’s Chinese jewelry market trends and future outlook

- Due to their differences, foreign and domestic brands target distinctive market segments and adopt different strategies. However, branded jewelry only accounts for 15% of China’s jewelry market so far, illustrating that there is still room for new players to enter the market.

- Lower-tier cities, non-bridal, self-purchasing, and smart jewelry are keywords in today’s jewelry market in China.

- In order to conquer the hearts of Chinese young consumers, jewelry houses need to develop a strong digital and social media strategy aimed at enhancing customer experience by integrating online and offline features.

- Chinese high-income consumers prioritize brands’ social responsibility and sustainability efforts when making luxury purchases and are willing to pay more for eco-friendly products.

Author: Hannah Wu

Learn more about China’s beauty market