China’s food delivery market size reached RMB 1.64 trillion (USD 229 billion) in 2024 and is projected to reach RMB 1.96 trillion in 2027. As of June 2024, the active users of online food delivery services in China amounted to 553 million, accounting for 50.3% of China’s internet user population. This secures China as the world’s largest food delivery market.

Download our report on young consumers in China

The three major players in China’s food delivery market: Meituan, Taobao Flash Buy, and JD

Takeout food in China began with foreign fast-food chains like McDonald’s, known as McDelivery (麦乐送) in the 1990s, followed by local eateries. Homegrown local restaurants followed suit then. The real surge came with the rise of online food delivery platforms, marking the rapid growth of China’s O2O delivery market.

China’s food delivery market is dominated by Chinese tech giants Alibaba and Tencent, who own 淘宝闪购/饿了么 (Ele.me) and 美团 (Meituan) respectively. In 2025, these two delivery apps controlled 90% of the country’s food delivery market. Due to the significant market share, it is not a surprise that there is a high barrier to entry into the food delivery industry in China. However, JD.com, another major e-commerce platform, entered the food delivery and local services market in 2025. Liu Qiangdong, the founder and chairman of JD, personally delivered a few meal orders as a publicity stunt for the new service.

Who are China’s food delivery industry’s consumers?

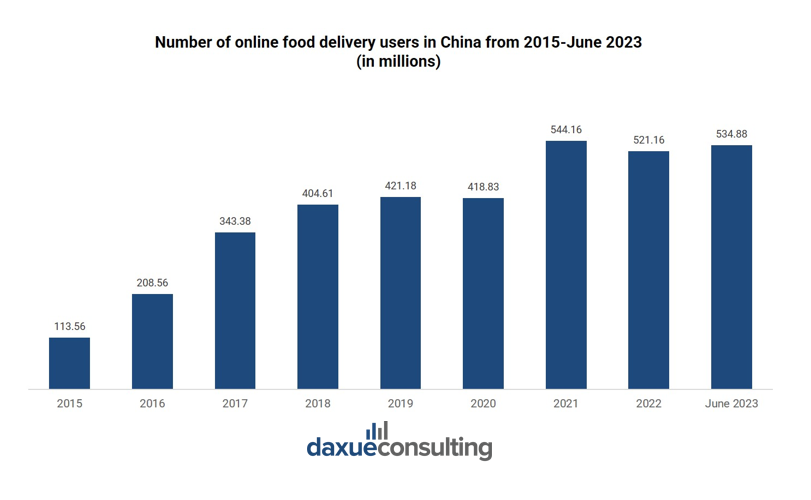

China’s food delivery services have witnessed remarkable growth, surging by approximately 371% from 2015 to June 2023. In 2015, there were just 113.6 million users of food delivery services in China. However, by June 2023, this figure had skyrocketed to an astonishing 534.88 million, showcasing the rapid adoption of delivery platforms in the country.

Online food delivery service users primarily consist of white-collar workers and skew toward the younger demographic

China’s online food delivery user base underwent a significant transformation. In 2015, 63% of users were white-collar workers, and 30.5% were students. By 2019, this shifted dramatically, with 83% being white-collar workers and only 10% students, illustrating a notable change in the industry’s consumer demographic.

Additionally, women constitute 51% of food delivery app users, and a substantial 85% of users fall between the ages of 18 and 40, indicating a predominantly young customer base. Particularly noteworthy is the nearly 20% increase in online food delivery orders from individuals born in the 2000s in 2021, underscoring their growing importance as a customer segment.

Top-tier cities are the main customers of China’s food delivery services

While more than half of Chinese online food delivery users, accounting for 53.9%, reside in top-tier cities (1st and 2nd tier) as of 2021, the real growth and potential are found in lower-tier cities. This is primarily due to the already high penetration of online food delivery services in top-tier cities, leaving room for smaller cities to flourish. Yet, according to Meituan’s April 2023 report, Shenzhen, Beijing, and Shanghai still stood out as cities with the highest vitality in online food delivery. This was supported by factors like delivery volume, user activity, restaurant delivery rates, and operating hours.

Convenience meets affordability: The reasons behind the popularity of food delivery in China

Food delivery services are exceptionally popular in China, surpassing their Western counterparts. There are several reasons to explain the disparity, such as the low cost and convenience of food delivery in the increasingly busy urban lifestyles in China.

Dining deals are due to high competition in China’s food delivery market

Chinese consumers are highly price-sensitive. In Greater China, food delivery costs are significantly lower, equaling just 10 to 20% of US prices, thanks to intense competition among providers like Ele.me and Meituan. The fierce market competition has led to aggressive price wars, with customers frequently enjoying generous discounts and coupons. These discounts, coupled with economies of scale, have made online food orders substantially more affordable than dining out. While the coupons are not as substantial as before, this strategy has transformed the dining habits of millions, making food delivery an exceptionally attractive and budget-friendly choice for the Chinese population.

Food delivery in China is widely embraced for its time-saving convenience

China has a demanding work culture, exemplified by the pervasive “996” schedule.

Additionally, a rising phenomenon known as “lazy cancer (懒癌)” reflects a prevalent sense of laziness that has diminished the appeal of cooking meals from scratch. About 67% of the 7,220 Chinese food delivery users surveyed cited laziness as the reason for ordering instead of dining out, as per a survey in March 2020.

Short video platforms entered the food delivery market

Kuaishou and Douyin, which are prominent short video platforms in China, are making a foray into the food delivery sector. These services were done by integrating ordering functions into their apps. Unlike traditional delivery services, these platforms do not manage logistics directly. Instead, merchants handle deliveries while the platforms drive traffic to their pages.

Short video platforms collaborate with established logistics players in order to facilitate operations. Kuaishou has partnered with Meituan, utilizing its logistics network, whereas Douyin collaborates with SF Express and Dada. Despite entering the market later, both platforms are leveraging their vast user bases to challenge established players like Meituan and Ele.me.

Kuaishou aims to enhance local services and revenue, while Douyin is striving to meet its 2023 GMV targets, having faced difficulties in this area. For both, food delivery represents a crucial opportunity for revenue diversification and growth, positioning them as new competitors to the sector’s main players.

2025 Food delivery war in China

In 2025, China’s online retail giants, Alibaba (through Taobao Instant Commerce & Eleme), and JD.com, engaged in a high-stakes price war in the food delivery market. The conflict brought heavily subsidized food deliveries that reshaped both the food & beverage and food delivery markets. It eventually drew direct government intervention.

The core trigger was JD’s aggressive market entry, which directly challenged the food delivery duopoly’s dominance. However, the deeper cause was a strategic battle beyond food delivery itself. The platforms were fighting to become the indispensable “everyday app” for Chinese consumers, using low-margin food delivery as a critical gateway to capture users for their broader retail, grocery, and local services, such as 30-minute delivery.

Immediate impact: Billions in losses and market turmoil

The subsidy war led to staggering financial losses. Combined, the giants spent over RMB 100 billion (approx. USD14 billion) on consumer discounts in 2025. Meituan posted its first quarterly loss in three years, while Alibaba’s profits plunged. Investors grew wary, and share prices fell. While consumers enjoyed steep discounts initially, merchants suffered. Many F&B operators reported squeezed profits and operational chaos from unpredictable, high-volume orders.

Regulation and unsustainable models

The war had two major implications. First, it prompted direct regulatory intervention. Chinese authorities summoned the companies, condemning the “irrational competition” and forcing a truce by mid-year, signaling a clear stance against market-distorting subsidies. Second, it exposed the limits of a pure subsidy-driven growth model. The “race-to-the-bottom” was proven financially unsustainable for even the largest tech firms, forcing a strategic re-evaluation towards healthier, service-oriented competition. The episode served as a cautionary tale on the perils of unchecked competition in China’s digital economy.

The future of China’s food delivery industry: A growing online grocery segment

Despite having gone from prosperity to decline in terms of its performance in the financing market in the late 10s, China’s grocery delivery industry is reaping the benefits of the stay-at-home economy that the COVID-19 pandemic has stimulated in China. The pandemic has introduced older demographics into the market. For the younger demographic, online grocery platforms provide a convenient solution to their busy lives. By allowing them to order groceries online, they can save valuable time and effort, adapting to their hectic schedules. On the other hand, for the elderly, who may find it challenging to venture out for fresh products, online grocery shopping offers a lifeline.

Major players in China’s online grocery segment include Alibaba, Tencent, JD, Meituan, and Pinduoduo. These platforms bridge the accessibility gap by delivering groceries directly to their doorstep, ensuring they have access to essential items without the physical strain of traditional shopping.

Evolving competition and future shift of China’s food delivery market space

- China is the world’s largest food delivery market (RMB 1.64 trillion in 2024), serving over 550 million users. It has long been a duopoly controlled by Meituan and Alibaba’s Ele.me, creating significant barriers to entry.

- The market’s explosive growth is fueled by a young, urban, white-collar user base. Key drivers are extreme price sensitivity (enabled by heavy discounts) and the time-saving convenience it offers within China’s demanding urban work culture.

- The market’s stability was disrupted in 2025 by JD.com’s aggressive entry, challenging the duopoly. This sparked a brutal subsidy war as platforms fought to become the essential “everyday app” for consumers, using food delivery as a loss-leading gateway.

- The price war caused over RMB 100 billion in losses for the giants, hurt merchant profits, and led to direct government intervention.

- The competitive landscape is expanding with short-video platforms (Douyin, Kuaishou) entering via partnerships. The future growth focus is shifting toward the online grocery segment, leveraging the infrastructure and consumer habits built by food delivery services.