Since 2024, China’s hotel market’s post-pandemic recovery-driven growth has come to a complete end, with the country returning to pre-2020 market levels.

Demand remains strong, but revenue growth stagnates

China’s hotel demand has largely recovered, but revenue growth has stagnated. Domestic trips grew 16% year-on-year in 2024, and nationwide occupancy returned to around 65–70%, close to pre-pandemic levels. However, average revenue per room has fallen 9.7% year-on-year to RMB 118 in 2024. This signals a widening gap between hotel occupancy and actual revenue generation.

Despite consistent travel volume, hotels are experiencing declining pricing power. The Average Daily Rate (ADR) dropped 5.8% in 2024. This reflects a shift toward “rational spending” among Chinese consumers, who now compare prices across Xiecheng, Meituan, Fliggy, and social platforms before making a booking. They remain price-sensitive and will not accept rate increases unless the property offers tangible upgrades in design, amenities, or service quality.

Competition has intensified across the market. More than 23,000 new hotels opened in China in the first half of 2024, surpassing pre-pandemic expansion levels. This rapid supply growth has pushed major cities toward saturation, while price sensitivity in lower-tier markets has triggered discount-driven competition among midscale brands.

Fewer hotels, bigger properties, and more chains

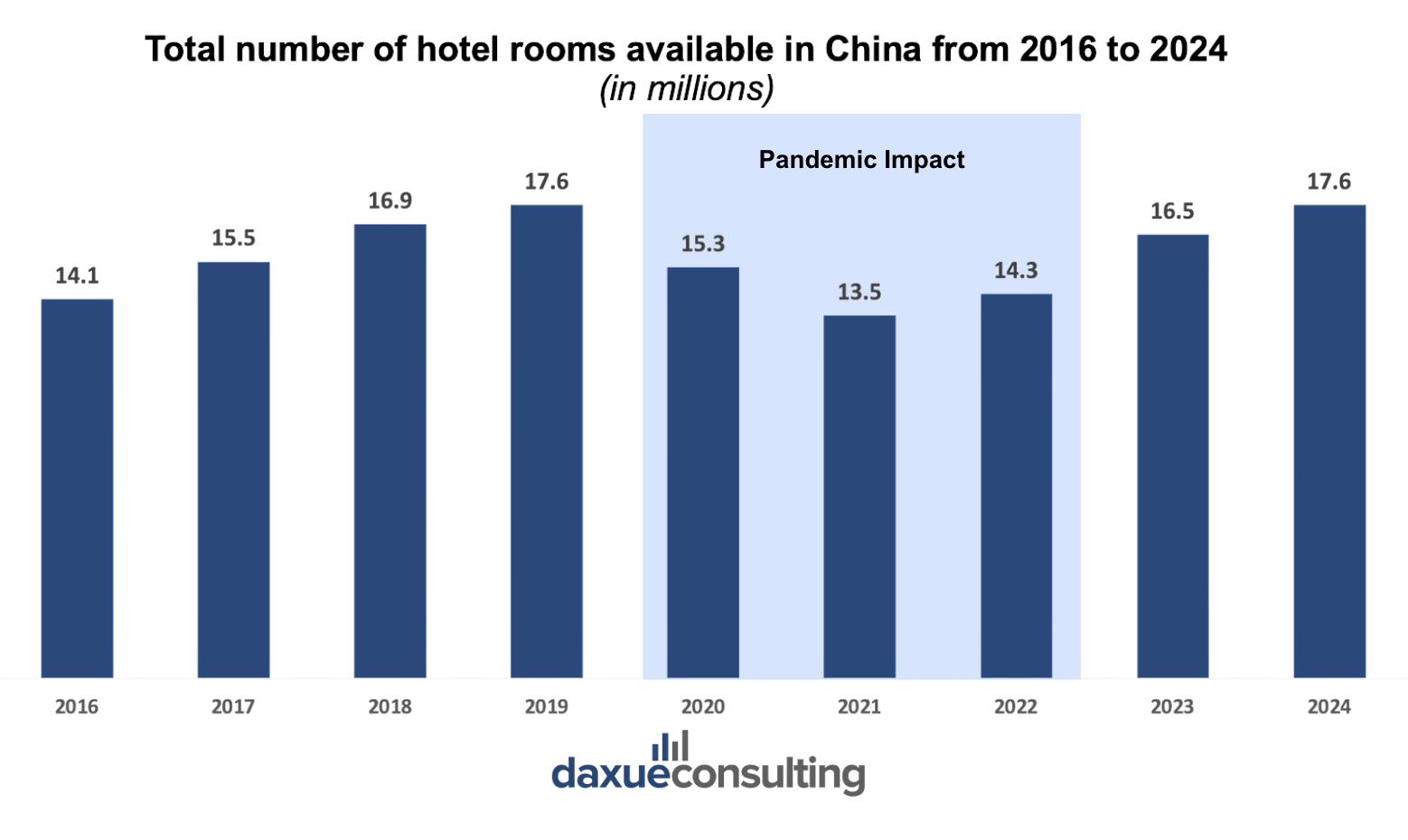

While the market has matured, its structure has undergone a transformation. According to the China Hotel White Paper 2025, the total number of hotels in China has declined since 2019; however, the total number of available rooms continues to grow. This reflects a strategic shift toward larger-scale developments with stronger operating efficiency. Full-service independent hotels are losing market share due to cost pressures, operational inefficiencies, and a lack of branding power.

| 2024 | Compared to 2019 | |

| Total Number of Hotels in China | 586,000 | +12.3% |

| Total Number of Hotel Rooms in China | 17.6 million | +18.7% 46% of additions are mid-to-high-end rooms |

| Hotel Chain Penetration | 41% | +13% |

Source: China Hotel White Paper 2025, designed by Daxue Consulting. The data shows the total number of hotels, rooms, and industry chain penetration in China as of 2024, with comparisons to 2019.

Although the market has recovered in terms of room nights and occupancy, profitability has not followed the same upward curve.

Heavy fixed costs keep margins thin

Hotels in China operate under a heavy fixed-cost structure, which limits profitability even when occupancy is strong. Rent is the largest burden, typically consuming around 30% of operating revenue for chain hotels. In Tier 1 cities, monthly commercial leases can reach 150–200 RMB per square meter, meaning a five-star hotel room of 50 square meters incurs 7,500–10,000 RMB in rent per month before labor or utilities are even considered.

Labor costs account for another 30% on average, driven by rising service expectations and intense hiring competition. Utilities add approximately 10%. With 70% of revenue locked into fixed expenses, most hotels in China must maintain occupancy above 65% just to break even—a fragile business model during periods of fluctuating demand.

As a result, asset-heavy hotel models are losing ground to franchise and management-light models that improve cash resilience and reduce operational risk.

OTA dependency affects revenue

At the same time, most Chinese hotels rely heavily on online travel agencies (OTAs) for bookings, often as their main source of demand. While OTAs provide traffic, they charge commissions that reach as high as 22% in some categories. Hotels cannot easily reduce OTA dependence without sacrificing occupancy, yet they cannot afford long-term revenue leakage through commissions.

These pressures have triggered heavy price competition. Operators frequently resort to discount wars to secure online visibility, but this only accelerates commoditization. Chinese travelers now expect to compare prices across platforms before booking, which weakens loyalty and makes it difficult for hotels to maintain price integrity.

The new consumer mindset affecting China’s hotel market

Most Chinese travelers now compare hotels across OTAs, Douyin, Xiaohongshu, and Meituan before booking. Search behavior shows that consumers compare design style, hygiene consistency, sleep quality, amenities, and overall brand personality. At the same time, consumers are increasingly seeking experiences with local relevance. Generic business hotels struggle to attract younger and leisure travelers who expect a unique stay, something connected to local aesthetics, culture, or storytelling. This has opened the door for experience-led hotel brands that differentiate beyond hardware.

A prime example is Atour, which has been recognized as one of the top 10 brands in the “2024 Mid-to-High-End Hotel MBI” list. Atour developed a community model centered around cultural IP collaboration to strengthen emotional connection. Through partnerships with brands like NetEase Cloud Music, Zhihu, Tencent QQ, Hupu, and its most recent collaboration, Crayon Shin-chan, Atour created themed rooms and public spaces that resonate with its target audience and differentiate itself by providing unique value to consumers. Atour successfully built higher brand loyalty and repeat bookings in the highly competitive Chinese hotel market. It now commands room rate premiums of up to 15–20% in many cities compared to conventional midscale competitors, even in a market with intense price sensitivity.

China’s hotel market’s revenue pressure is forcing business model innovation

For years, hotels in China relied on a simple revenue model: sell rooms and, if possible, add a little income from breakfast and meeting rooms. With rising operating costs and declining pricing power, revenue from rooms alone can no longer sustain healthy profit margins. Operators in the market are now exploring new revenue streams, using existing assets more flexibly, and learning to sell more than accommodation.

Atour turned a hotel stay into a product business

Atour is also a good example in this regard. It recognized an opportunity hidden in plain sight: if guests consistently praised the quality of their sleep, then sleep itself could become a product. This insight led to the creation of Atour Planet, a retail extension of the brand that offers a range of products.

Atour’s now-iconic Deep Sleep Pillow Pro became a bestseller across Tmall and Douyin, turning what was once just part of the room experience into a national consumer product line. Today, retail accounts for more than 30% of Atour’s total revenue. Unlike traditional hotel income, they are not limited by the number of hotel rooms or occupancy rates.

Chinese luxury hotels are experimenting with new revenue models

In Zhengzhou, a five-star hotel recently went viral after opening a street food stall outside its entrance. Chefs in full uniform sold street snacks to locals, generating 30,000 RMB in a single day. The move was controversial; the hotel’s general manager defended the decision, saying, “If China’s hotel market changes, hotels must change too.”

The hotel introduced a new revenue stream to enhance cash flow. It also repaired its relationship with the local market by making the hotel feel less distant and more approachable.

Technology and policy are redefining competitive advantage in China’s hotel market

Efficiency through technology

Labor and lease costs remain high, so players are already using technology to protect margins. Self-service check-in, AI-powered customer service, and robotic delivery reduce staffing needs, while smart room systems cut energy use. Dynamic pricing engines, which are already standard at Huazhu and BTG Homeinns, are optimizing room rates automatically based on demand data, boosting revenue per available room without manual intervention.

Policy support is reshaping industry focus

The 14th Five-Year Tourism Plan encourages cultural tourism development. This benefits brands in China’s hotel market that localize guest experience through design and storytelling.

Additionally, Visa-free entry expansions and inbound tourism recovery are pushing international brands to accelerate reopening and new projects in Tier 1 and tourist cities.

Key takeaways of China’s hotel market 2025:

- Post-pandemic rebound has normalized, but pricing power is eroding under rational spending and OTA price transparency.

- Fewer hotels but more rooms reflect the rise of chain brands and the decline of independent operators lacking cost control and brand power.

- High fixed rents, rising labor costs, and heavy OTA commission dependency are compressing profitability and fueling discount wars.

- Consumers now choose based on experience and local relevance, pushing hotels to move beyond standardized business lodging.

- To offset room revenue stagnation, leading brands monetize beyond accommodation through lifestyle retail, F&B extensions, memberships, and branded collaborations.

- AI operations, smart energy systems, and dynamic pricing improve efficiency, while cultural tourism policy and visa-free entry support localized, experience-led growth.