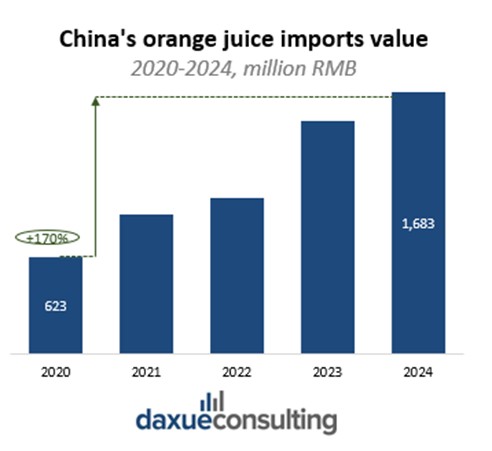

The orange juice market in China reached RMB 142.9 billion (USD 20.4 billion) in 2024, growing at a CAGR of 4.6% during the forecast period of 2025–2033. The market is rising despite a decrease in consumption volume because consumers are more concerned about product quality. They are willing to spend more per unit. In other words, value is growing even as volume falls, clear evidence of trading up. This is driven by the health-conscious trend, premiumization, and new production technology.

Download our China F&B White Paper

There are many reasons for growth in value, but a decline in volume consumption. Acceptance of higher-priced orange juice started with the introduction of differentiated products using new technology in the production process, such as NFC (Not From Concentrate), which keeps taste and nutrients better than FC (From Concentrate), which often contains added sugar, aroma, and preservatives. HPP (High Pressure Processing), or cold-pressed processing, also helps orange juice in China gain higher value. In market positioning, NFC is often the more “mainstream premium” choice (premium but more scalable), while HPP is usually priced higher and positioned as ultra-premium due to processing and cold-chain requirements. The market could not grow like this if products did not align with health-shift trends. People prioritize nutrition and prefer fresh products such as organic raw materials and low sugar.

Domestic supply gaps keep imports in the driver’s seat

The orange juice market in China is marked by a highly fragmented upstream sector, heavy reliance on imported concentrated juice, and intense competition among downstream brands and distribution channels. Raw material supply in China is not able to meet manufacturers’ processing demand at scale. This problem is caused by small farmers and low integration in the sector, which leads to inconsistent raw material supply. This becomes an obstacle when manufacturers need to purchase large volumes. Moreover, many citrus producers focus mainly on fresh consumption. Domestic production of varieties suitable for juice processing, such as Hamin and Valencia, is still limited, so imported citrus juice becomes a key solution.

China imports up to 70% of its orange juice market volume. High imports are mainly driven by strong domestic fresh consumption and limited domestic supply of juice-suitable varieties. Imports help manufacturers secure suitable product quality and lower costs through economies of scale. Brazil ranks number one for China’s citrus imports. Orange juice imported from Brazil is seen as reliable by consumers and often comes at an affordable price, such as Natural One’s purely pressed product.

High investment costs of equipment and technology also cause challenges for juice processing. Small and mid-sized manufacturers cannot maximize production capacity. In Brazil and other countries with strong orange-processing expertise, producers can maximize scale and align investment in equipment and technology, so import prices can be more competitive than domestic production.

Premium orange juice is built on health messaging and convenience

The main consumers of orange juice in China are young people, those born between the mid-1990s and around 2010. They are more likely to be health-conscious and have a strong interest in buying orange juice as an additional nutritional drink. Many consumers are in tier-one cities and the middle class with higher household incomes. They are able to choose higher-quality products that match their healthy lifestyle.

Purchasing is strongly supported by online marketing. There is a lot of online content explaining product differences between FC, NFC, and HPP orange juice. This content educates consumers and supports the premiumization trend, where consumers are willing to pay more for higher quality. Consumers increasingly want vitamin-rich products, fresh taste, and low sugar.

The shift toward health awareness among young urban consumers reinforces the growth of the premium orange juice market in China. Urban consumers often have limited time and higher-than-average income. Their behavior favors convenience and fast access to information. All these factors drive high-value orange juice growth in China.

International brands set the pace; local brands fight for share

There are several key players in the fruit juice market in China. Well-known international brands include Coca-Cola (Minute Maid) and PepsiCo (Tropicana). Together, these companies account for around 23% of the fruit juice market in China. International brands have strong brand equity and supply chains. Meanwhile, popular local players include Weichuan, Huiyuan, Master Kong, Uni-President, and Orchard Farmer. However, local Chinese brands are still fragmented, with no single brand reaching over 20% market share. Downstream players still rely heavily on imported raw materials.

Focusing on premium orange juice products, many brands serve niche consumers who demand high-quality orange juice. Even though this segment is still small compared with the total orange juice market in China, it is growing consistently. The fruit juice market in China can be divided into pure and medium-concentrate juice (considered premium), which accounts for 26% of the market, while low-concentrate juice accounts for 74%. A challenging market structure creates a large room for opportunity.

Processing tech and logistics are the next battlegrounds

The orange juice market in China faces various challenges in consumption patterns, consumer behavior, and supply chain limitations. From a market perspective, consumer demand is pushing for high-quality products such as NFC and HPP. These require advanced processing technology and stronger cold-chain/logistics capability. Consumers want vitamin-rich beverages with low sugar.

In terms of the supply chain, the market faces challenges across the whole process. Raw material issues can be divided into two main points: (1) scattered small local citrus producers, and (2) local citrus varieties that are not sufficient or suitable for orange juice production. As a result, the market relies on imports for over 70% of supply to secure stable volume and consistent quality.

There are many opportunities across the orange juice market in China. Citrus producers can adjust citrus varieties or improve raw material quality to match manufacturer needs. They can also create new processed citrus products to add value. Brands can become trendsetters for nutrition drinks by educating consumers about the functional benefits of orange juice, then introducing high-nutrition orange juice products to the market.

Opportunities exist not only for beverage businesses but also for the supply chain sector. New high-technology equipment is needed to develop the domestic orange juice market in China. The market needs reliable technology at an affordable cost to produce competitive products that meet consumer demand. Transportation is another opportunity. Higher demand for NFC and HPP premium products increases the need for cold-chain and faster transportation. Specialized logistics services are growing with demand. If logistics providers can offer lower-cost services with specific cold-chain functions, they can change the competition landscape of the orange juice market in China.

From “more juice” to “better juice”: where the next growth will be in China’s orange juice market

- Value is growing even as volume falls because consumers are trading up and paying more per unit for higher-quality orange juice.

- Premiumization is driven by technology, especially NFC and HPP. These products are positioned as fresher, healthier, and closer to “real juice” than FC products.

- China depends heavily on imports (up to ~70%) due to fragmented farming, inconsistent supply, and limited local varieties for juice production.

- Young, urban, middle-class consumers lead demand, and online education/marketing plays a major role in explaining product differences and justifying higher prices.

- Big opportunities sit in processing and cold-chain logistics: advanced equipment, scalable production, and affordable cold-chain transport will shape who wins as demand shifts to premium juice.