Consumer trends in winter shoes

Winter shoes in China are a highly season-dependent consumer product. The vast climatic differences between northern and southern China shape consumers’ distinctly different choices for winter footwear. In Northern regions with extreme cold, such as Heilongjiang, Inner Mongolia, and Xinjiang, locals prefer winter boots that are slip-resistant, durable, and highly insulated to withstand sub-zero temperatures. In contrast, consumers in the milder Southern regions view winter footwear as fashion items. On social media platforms, users showcase snow boots featuring light colors and fluffy textures during winter. The “snow boots” (雪地靴)tag alone has surpassed 2 billion views on Xiaohongshu (also known as RedNote). Related trending terms include “fuzzy slippers”(毛绒拖鞋) and “fur-lined shoes” (皮毛一体鞋)with view counts nearing 100 million and 19 million, respectively. For this segment of consumers, the fit of the shoes, as well as the texture and warmth of the leather and fur, are nearly equally important.

Download the winter sports market report:

A functional concept rather than a fixed category

Winter shoes in China do not constitute a strictly defined or standardized product category. Instead, the term broadly refers to footwear designed to enhance comfort and practicality during cold weather. This encompasses traditional snow boots engineered for extreme cold or outdoor use, as well as sneakers and casual shoes featuring thickened soles or fleece-lined interiors tailored for urban winter wear. From the consumer perspective, the definition of winter footwear hinges more on functional attributes like warmth, insulation, lining thickness, and cold resistance than on formal product classifications. Consequently, brands across various sectors, including athletic wear, outdoor gear, fashion apparel, and mass-market retailers, participate in the winter footwear market through diverse product offerings and positioning strategies.

A burgeoning segment due to more winter activities

Benefiting from the resurgence of winter shoe promotion on social media and a post-pandemic consumption rebound, winter footwear sales in China surged in late 2023. At Intime department stores, winter shoes’ revenues increased by 643% year-over-year in December. This growth was partly amplified by a base effect, as sales during the same period in 2022 were constrained by lingering pandemic-related travel restrictions and subdued consumer activity. Beyond short-term recovery effects, the boots segment shows solid structural growth potential. Moreover, China’s boots footwear market is projected to reach USD 12.20 billion in 2025, growing at a CAGR of 5.66% over the next five years.

Winter leisure activities serve as another catalyst driving winter footwear consumption. Following the 2022 Beijing Winter Olympics, the government has vigorously promoted winter sports, attracting millions of new participants to experience skiing, ice skating, and alpine tourism. Since the Olympics, over 313 million Chinese have engaged in winter sports or related leisure activities. This snow economy has fueled consumer demand for specialized winter footwear, from waterproof snow boots for tourists to insulated hiking boots for enthusiasts. Notably, nearly 80% of visitors to northeastern China’s winter destinations hail from southern regions. This indicates the winter footwear market is expanding beyond traditionally cold areas.

Design vs functionality of winter shoes

Industry research indicates that women often favor fashionable winter footwear, such as boots with faux fur lining and high-heeled ankle boots, while men tend to prefer functional outdoor shoes and sneakers even during winter. In China, this trend is particularly evident on social media: Women have spearheaded the trend for cute, fashionable snow boots on Xiaohongshu, especially driven by celebrity KOLs. They typically favor warm color palettes (chestnut, light brown, and beige) to emphasize a relaxed winter vibe. In winter, these color palettes often enhance an outfit’s aesthetic appeal, conveying an immediate sense of comfort. Men, however, prioritize practicality, leaning toward sporty, function-driven outdoor styles in their choices. Their overall palette tends toward cooler or neutral tones, projecting an image of rationality and strength.

Competitor landscape and positioning of winter shoes in China

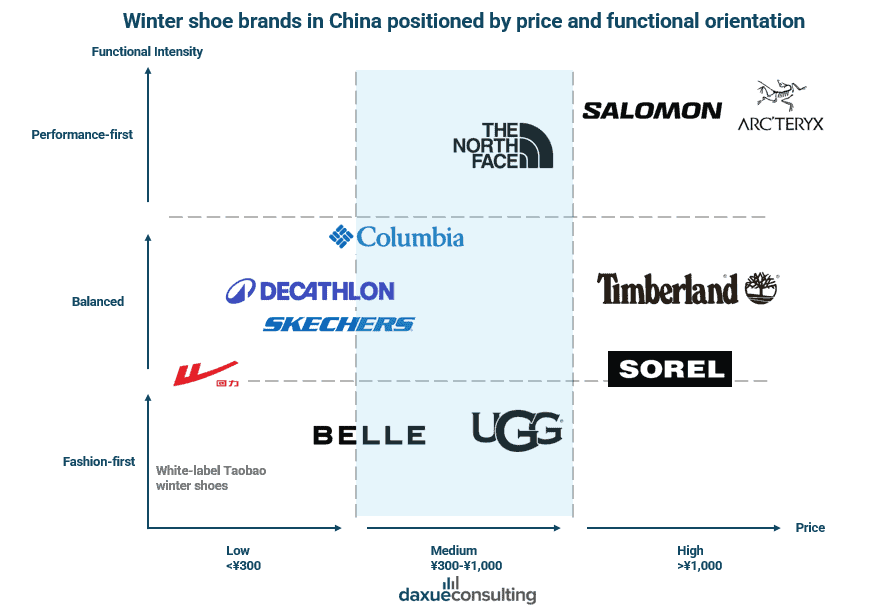

From a consumer perspective, the winter shoes in China can be broadly segmented along two key dimensions: price and functionality. The industry segmentation typically categorizes footwear products into three tiers: mass/low, medium, and high/premium for analysis. Within China’s overall footwear market, consumer demand concentrates within specific price brackets. A 2022 study revealed that the highest volume of athletic shoe purchases occurred in the RMB 301 to RMB 500 and RMB 501 to RMB700 price ranges, accounting for approximately 66% of total sales among surveyed consumers. In the low-price segment (below RMB 300), the winter shoes market in China is primarily dominated by Taobao’s white-label brands (basic boots with low cost from an independent manufacturer) and value-oriented brands, such as Huili and Decathlon. These brands emphasize basic warmth and price competitiveness rather than design or high performance.

Most crowded segment: Medium price range

In the medium-price range (RMB 300 to 1000), brands like Skechers, Columbia, and Decathlon hold relatively balanced market positions. They balance comfort, everyday practicality, and accessible pricing, making them popular among mainstream consumers. In the high-price segment (over RMB 1,000), the market shows a clear differentiation: performance-focused outdoor brands like The North Face, Salomon, and Arc’teryx emphasize professional warmth, traction, and durability for harsh winter conditions; while fashion-first brands such as UGG, Sorel, and Timberland prioritize style and visual appeal while offering moderate functionality. This indicates that as prices rise, Chinese winter footwear consumption shifts from basic utility toward either specialized outdoor performance or fashionable lifestyle positioning.

Additionally, this positioning map reveals two key findings. First, the medium-price range is the most competitive and crowded segment, with brands like Decathlon, Skechers, and Columbia balancing functionality and affordability, indicating this segment holds China’s broadest consumer base. Second, the premium market exhibits clear polarization: high prices support both professional outdoor gear and fashion-forward winter boots, signaling consumers’ willingness to pay premium prices for either ultimate performance or exceptional design, reflecting increasingly segmented consumer demands.

E-Commerce and offline distribution channels

E-commerce has become the preferred channel for many footwear consumers due to its convenience, extensive product selection, and aggressive online promotions. Recent data indicates that 57% of Chinese consumers prefer to purchase athletic shoes and related products online. Additionally, the livestreaming penetration rate in China hit 70.6% in 2024. This trend is likely reflected across the winter footwear market. Meanwhile, emerging channels are rapidly gaining traction. Douyin has captured a significant share of the fashion retail market through its integration of short videos and in-app shopping. By the first half of 2025, Douyin is projected to account for 39% of China’s online sports apparel sales and over 50% of outdoor gear sales. This means that when young consumers browse winter outfit videos on Douyin, they can instantly purchase the winter shoes featured in the videos, blurring the lines between content and commerce.

Brick-and-mortar stores still play a role in winter shoe sales

Despite the rapid growth of digital retail, offline shopping remains indispensable. Chinese consumers still prefer trying on shoes to assess fit and comfort, and foot traffic surges in physical stores during cold snaps or holidays. For instance, during the 2024 Spring Festival holiday, many large shopping malls in Beijing and Shanghai saw customer traffic increase by 40% to 80% year-over-year. Department store chains like Intime and shopping malls such as SKP meticulously curate winter zones. It allows consumers to personally test the warmth of snow boots or the traction of hiking boots.

While the surge in foot traffic may not directly translate into increased sales of non-essential items like footwear, physical stores serve as crucial touchpoints where consumers can try on winter shoes, assess fit and comfort, and build brand awareness. The final purchase, however, is often completed online or through omnichannel channels. Furthermore, thriving membership stores in first-tier cities, including warehouse-style supermarkets like Sam’s Club and Costco, alongside domestic brands, have opened new offline sales channels for winter shoes in China.

A cautionary tale comes from the parent company of the UGG brand, whose stock price plummeted following the release of its Q2 FY2026 revenue report. The primary issue stems from a significant deterioration in UGG’s direct-to-consumer (DTC) channels, exposing the brand’s lack of innovation in digital channels and its failure to adapt promptly to the resurgence of consumer spending in physical retail.

Sustainability and materials of winter footwear

China’s massive footwear industry is undergoing a green transformation, with factories adopting cleaner production processes driven by both policy incentives and cost-effectiveness. Many shoe manufacturers in Guangdong and Fujian provinces have begun using recycled rubber soles and are experimenting with biodegradable polymers for uppers.

In terms of materials, consumers with specific needs also have requirements for the composition of winter boots. Vibram (V-sole) material is a renowned Italian high-performance rubber celebrated for its exceptional durability, slip resistance, lightweight properties, and traction. Through its patented formula and intricate tread patterns, such as Carrarmato, it delivers all-weather stability, shock absorption, and flexibility, providing secure traction even on slippery rock surfaces.

Winter Shoes in China: More than just boots

- The North prioritizes functional, durable, and highly insulated boots for extreme cold. The South, driven by social media trends, treats winter footwear as a fashion item.

- “Winter shoes” is not a rigid product category but a functional concept that includes everything from heavy-duty snow boots to fleece-lined casual sneakers. Consumer choice hinges on attributes like warmth and insulation, allowing diverse brands from sportswear to fast fashion to compete.

- The market surged post-pandemic and is supported by long-term growth in the boot segment. A major catalyst is the “snow economy,” which was ignited by the Beijing 2022 Winter Olympics. It has driven millions, particularly from Southern China, to winter sports and tourism. This creates a new demand for specialized footwear.

- The market segments are clearly defined by price point, with the mid-tier being the most crowded and competitive. The premium segment shows polarization: consumers pay high prices either for technical performance (outdoor brands) or for fashion and branding (lifestyle brands).

- While e-commerce and social commerce (especially via livestreaming and Douyin’s shoppable videos) are dominant sales and discovery channels, offline stores remain vital for product trial, brand experience, and capitalizing on seasonal foot traffic. Success requires a seamless omnichannel strategy.