Amid the broader challenges facing China’s real estate market, China’s luxury home market has stood out as a bright spot. Even as the broader market cools in 2024-2025, demand for luxury homes remains robust. This creates a stark contrast with low– to mid-tier commodity housing, presenting a picture of “two worlds apart.” From a macro market perspective, from January to November 2025, national residential real estate investment totaled RMB 6.0432 trillion, a year-on-year decrease of 15%. Sales of newly built commercial housing reached RMB 7.513 trillion, a 11.1% decrease.

Meanwhile, in key cities such as Beijing and Shanghai, transactions of new homes priced between RMB 10 and 20 million per unit increased by 38% and 22% year-on-year, respectively, indicating resilience. On December 28, 2025, the CITIC City Kai Xinyue Bay project along Shenzhen Bay officially launched sales. Within just two hours, sales exceeded RMB 10 billion, with approximately 80% of the initial 156 units sold. This achievement set a new national record for luxury property sales at launch.

How big is this market?

In China, “luxury homes” are typically defined by price thresholds, traditionally referring to properties priced at RMB 10 million (USD 1.4 million) or above. According to China Real Estate Information Corporation (CRIC) data, 2023 marked the strongest year on record, with approximately 52,000 luxury homes sold across China’s top ten cities. Based on an average transaction price slightly above RMB 10 million, the annual market value of luxury residences is estimated at approximately RMB 800 billion to RMB 1 trillion. Despite a significant slowdown in market transactions in 2024, only approximately 40,000 properties priced above RMB 10 million were sold throughout the year. However, by the first half of 2025, sales of luxury residential properties priced above RMB 10 million reached 21,000 units, marking a 21% year-on-year increase. Compared to the steady monthly decline in the real estate development prosperity index since March, this indicates potential for counter-trend growth.

Market segmentation of Chinese luxury housing

Definitions of “luxury property” may vary across cities. In first-tier cities like Beijing or Shanghai, a RMB 10 million property might be considered a relatively ordinary high-end apartment, whereas in smaller cities, it signifies a true luxury residence. CRIC further segments the market into “mid-tier luxury” (RMB 10 million to 30 million) and “ultra-high-end luxury” (RMB 30 million and above).

Which cities dominate the luxury housing market?

By city tier, China’s luxury home market is highly concentrated in first-tier cities (Beijing, Shanghai, Shenzhen, Guangzhou). In 2023, sales of luxury homes priced above RMB 10 million in these four cities accounted for nearly 80% of the national total. By the first half of 2025, transactions in the four first-tier cities reached 16,000 units, still representing approximately 76% of the market. The remaining 20-25% of luxury home transactions were concentrated in a handful of affluent second-tier cities (provincial capitals and prosperous coastal cities), with only a minimal portion occurring in smaller cities.

Second-tier cities demonstrate growth potential

Nevertheless, demand for luxury homes in major second-tier cities is on the rise. In the first half of 2025, luxury home sales in 16 key second- and third-tier cities surged 37% year-on-year, far outpacing the 15% growth in the four first-tier cities. Ningbo‘s share of sales for homes priced above RMB 10 million tripled from approximately 1.9% to 6.2% by early 2025. Xiamen saw transactions exceeding RMB 30 million quadruple (from a low base). This illustrates China’s highly regionalized luxury home market: its value remains concentrated in a handful of megacities, while select second-tier cities, though contributing an increasing share, still occupy a secondary position.

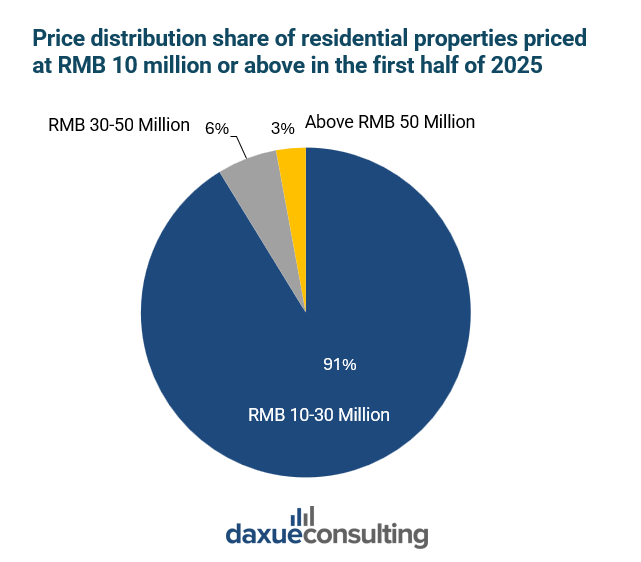

Price range-based segmentation in China’s luxury home market

In the first half of 2025, most new luxury home sales were concentrated in the RMB 10-30 million price range. Among transactions in 20 major cities, properties priced between RMB 10 million and 30 million accounted for 19,561 units, representing approximately 91% of the overall market share. Transactions for new luxury homes priced above RMB 50 million totaled 621 units, marking a significant 51% year-on-year increase. Only the segment of new luxury homes priced between RMB 30 million and RMB 50 million saw year-on-year sales declines of around 30%. This downturn primarily resulted from a high baseline in the previous year.

The dominance of luxury homes priced between RMB 10 million and 30 million in the market stems from the combined effects of both demand and supply. On the demand side, starting in 2025, the government accelerated the implementation of improved housing standards, driving developers to increase the actual floor area ratio and improve the comfort of residential properties. This aligns with the needs of high-net-worth families seeking upgraded living experiences. The recent policy of lowering loan interest rates (detailed later) has been most beneficial to this segment of buyers. Purchasers of luxury homes priced at RMB 30-50 million or more are typically ultra-high-net-worth individuals who more frequently pay in cash. For real estate developers, properties in this price range offer significantly better liquidity than those in higher price brackets, translating to improved capital turnover rates and reduced inventory risks.

Shanghai, the most important market for ultra-luxury homes

The ultra-luxury property market may have a small base, but it continues to expand as ultra-high-net-worth buyers compete to snap up the most exclusive residences. Notably, Shanghai dominates the ultra-luxury property market. In the first 11 months of 2025, the city alone accounted for approximately 76% of residential sales exceeding RMB 50 million across major cities, with 889 transactions. In contrast, Beijing, Guangzhou, and Shenzhen collectively recorded only about 279 transactions. This underscores Shanghai’s position as the epicenter of China’s ultra-high-end market. Overall, market value tends to cluster in lower price brackets due to transaction volume, yet the high-end segment remains robust and significant in absolute terms.

Where does the demand come from?

Against a backdrop of escalating global economic uncertainty, luxury real estate has demonstrated characteristics akin to gold as a safe-haven asset. Its scarcity, preservation of value, and long-term appreciation potential make it the preferred asset for high-net-worth individuals seeking to combat inflation and achieve wealth succession.

Furthermore, China real estate market is supported by clear policy guidance. Beginning in 2024, China’s real estate regulatory policies underwent a historic shift, with more than 700 measures introduced throughout the year. The market collectively refers to them as “four reductions, four eliminations, and two increases.” On May 17, 2024, the People’s Bank of China lowered the minimum down-payment ratio for first-home commercial mortgages and removed the policy floor on interest rates for both first- and second-home commercial loans.

By September 29, 2024, multiple first-tier cities rolled out a series of policies to cancel or reduce property purchase restrictions and ease credit policies. Shanghai announced in September 2024 that the down payment for first homes would be reduced to 15%, while the minimum down payment for second homes would be reduced to 25%. Shenzhen simultaneously reduced the down payment requirement for second-home commercial loans from 30–40% to 20%. This significantly lowered the upfront capital required to purchase high-priced properties, enabling buyers to more easily secure the down payment.

The luxury home market in China receives a major boost

The luxury housing market has received even more direct policy stimulus. In October 2024, Shenzhen abolished price caps on commercial housing and apartments, shifting to a system in which developers independently set reasonable prices and submit them to market regulators. By late 2024, Beijing, Shanghai, and Shenzhen successively announced the abolition of the distinction between ordinary and non-ordinary housing. Effective December 1st, “luxury homes” would no longer be defined based on floor area or total price. This allows developers to create more spacious and comfortable medium- to large units, eliminating the need to artificially reduce luxury home sizes to comply with outdated regulations.

Tax incentives have also effectively stimulated purchasing demand. Previously, Beijing, Shanghai, Guangzhou, and Shenzhen imposed additional taxes (“luxury home taxes”) on high-priced, large-unit properties, thereby increasing transaction burdens. For instance, since 2005, Guangzhou has imposed a 5.3% additional value-added tax on second-hand homes that meet luxury criteria. Effective December 1, 2024, first-tier cities ceased levying value-added tax on second-hand “non-ordinary housing,” applying uniform tax policies to luxury and ordinary homes. Industry statistics indicate that from December 1 to 5, 2024, 364,000 homebuying households nationwide benefited from deed tax incentives, with cumulative reductions totaling RMB 8.4 billion, an average savings of RMB 23,000 per household. Consequently, the abolition of the luxury home tax represents a significant boon for those upgrading their residences.

5 things to know about China’s luxury home market

- From January to November 2025, China’s overall residential sales declined by 11.1% year-on-year. However, luxury home sales bucked the trend: in the first half of 2025, transaction volumes for properties priced above RMB 10 million in 20 core cities surged by 21% compared to the same period the previous year.

- Despite a slower volume in 2024, which is around 40,000 units, demand rebounded in early 2025 with 21% YoY growth. First-tier cities such as Beijing, Shanghai, Guangzhou, and Shenzhen consistently account for 75-80% of sales.

- In H1 2025, 91% of luxury home sales were priced between RMB 10M–30M, but ultra-luxury deals (≥RMB 50M) surged 51% to 621 units. Shanghai accounted for 76% of these high-end sales, reinforcing its role as China’s capital of ultra-luxury.

- In a volatile macro climate, luxury real estate is viewed as a scarce, inflation-resistant store of wealth. China’s high-net-worth individuals favor luxury housing for value preservation, lifestyle upgrade, and wealth transfer, especially as policy and financing barriers ease nationwide.

- Beginning in 2024, first-tier cities lifted price caps and abolished the “non-ordinary” housing definition. There is also reduced mortgage down payments to 15–25%, and eliminated luxury-specific transaction taxes. These measures significantly lowered the cost and difficulty of purchasing high-end homes and directly stimulated luxury demand.