With a user base of 495 million, larger than the population of the United States, e-sports in China is a mature consumer industry. China measures its e-sports market in two ways. The narrower figure is industry income, revenue earned by the e-sports industry itself from tournaments, broadcasters, and league operators. In 2025, this reached RMB 29.3 billion (~USD 4.0 billion), up 6.4% year-on-year.

Download our China summer sports report

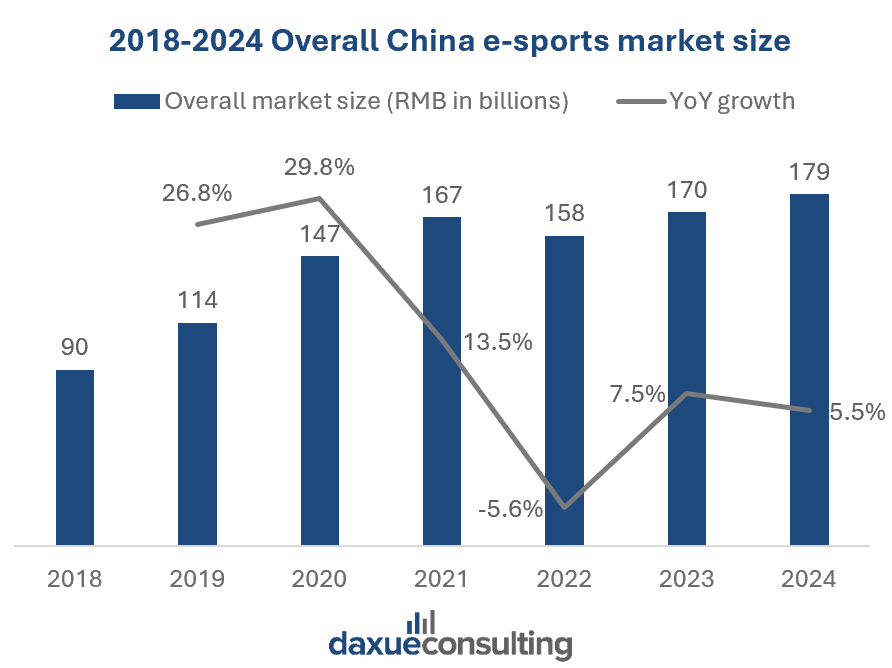

The broader, overall market size captures all consumer and corporate spending around the ecosystem: in-game purchases, fan revenue, sponsorship, advertising, and IP income. By this measure, the market stood at RMB 179 billion in 2024, growing at a 5.5% CAGR.

The broader market’s trajectory shows a familiar arc. Growth peaked through 2020 as pandemic lockdowns drove users online. In 2022, the market contracted, hit by a long freeze on new game licenses and the August 2021 restrictions on minor gaming. Growth has since returned, but in single digits, demonstrating that the market has moved out of hypergrowth and into maturity.

A market like no other

In November 2025, the Honor of Kings Pro League (KPL) Grand Finals at Beijing’s National Stadium drew over 60,000 live attendees. This set a Guinness World Record for a single e-sports match. That scale puts China at the top globally in terms of audience. However, the revenue picture is more lopsided, as North America generated the largest revenue share at 39% in 2025. Western markets rely more on revenue per user through sponsorship and media-rights deals. Meanwhile, China converts its enormous audience through volume and livestreaming. China can fill stadiums for a mobile-game final thanks to three factors absent in the West: hundreds of millions of viewers reachable inside one country and one language, state recognition that gives major events the social standing of national sporting occasions, and purpose-built arenas that treat tournaments as engines of local tourism and consumption.

Maturing on spending, not headcount

Both measures of e-sports in China now grow in the mid-single digits: industry income rose 6.4% in 2025, overall market size grew at a 5.5% CAGR in 2024. The audience has essentially stopped expanding too, growing from 489.2 million in 2021 to 495.3 million in 2025, a gain of just over 6 million across four years. As a result, future income must come from increased Average Revenue Per User rather than reach.

Two forces are picking up the slack and sustaining growth. First, professionalization and standardization. In December 2024, China implemented its first national e-sports standard governing arena operation and joined an international ISO standard. The market has moved from “experience-led” to “rule-led,” adding the stability and scalability that attract long-term capital and venue investment.

Second, mainstream legitimacy. Once dismissed as an unhealthy distraction, competitive gaming now produces national sporting moments. It is most visible when China won four gold medals at the 2023 Hangzhou E-sports Asian Games. That kind of recognition unlocks the corporate sponsorships and municipal partnerships that a market with flat user growth needs to keep expanding.

Who watches, and where the money flows

In 2025, men make up 63.4% of users and women 36.6%, with the female share rising 4.9 percentage points since 2023. The audience is also aging upward. Under-30s remain the core at 68.5%, but the over-30 share has climbed to 31.5%. The broadening is good news for advertisers reaching beyond a young-male core. However, the upward aging is a warning sign, as a market that grows older instead of renewing from the bottom might face an audience cliff.

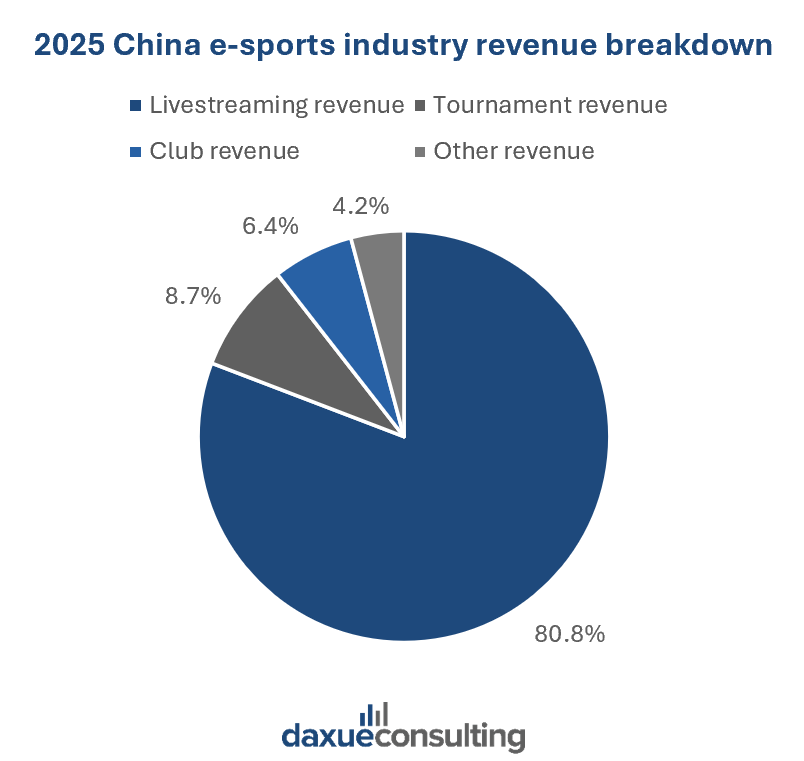

From a revenue standpoint, livestreaming generates the overwhelming majority of industry income at 80.8%, with tournaments, clubs, and other streams making up the remaining ~19%. In the West, leagues monetize chiefly through sponsorship, media rights, and tickets; in China, the creator-and-streaming layer is the business. A foreign team or sponsor that thinks in terms of event sponsorship is misdirected in a market where most money lives on streaming platforms. Furthermore, the pattern also shows how thoroughly e-sports in China is fused with its broader streaming economy, as revenue now follows continuous attention, not just tournament events.

What shapes e-sports in China

A two-track government

The Chinese state runs two parallel policies on competitive gaming, and they rarely touch. One promotes e-sports as a digital-economy asset: official recognition as a sport in 2003, the State Council’s 2018 designation of e-sports as “sports consumption,” and inclusion of the industry in the 2025 National Consumption-boosting Plan.

The other restricts gaming as a social risk: minors capped at three hours of gaming a week, mandatory real-name registration, and the “spiritual opium” rhetoric of 2021. Interestingly, the state treats addiction risk and industrial value as separable objects, governed by different incentives. The industry’s ceiling is set by how well it stays on the right side of the promotion narrative. Hence, it is why operators lean heavily on framings of tech innovation, consumption engine, and national pride.

Tencent’s structural gravity

Tencent operates the KPL and owns Riot Games (which runs the League of Legends Pro League). It also published most of the titles featured at the 2023 Asian Games. The same company can be a game’s developer, league operator, and broadcaster, a degree of vertical concentration that regulators elsewhere would scrutinize. As of 2024, Tencent holds roughly half of China’s overall gaming market. For anyone entering, Tencent is simultaneously the gatekeeper, the landlord, and the competition.

Cities as the unit of strategy

In China, cities compete to host the industry as economic development, with offline events concentrating in a handful of “e-sports cities” led by Shanghai, Chengdu, and Chongqing. Municipalities build dedicated arenas and set up industry funds, as the number of high-level tournaments hosted continues to rise. The unit of strategy is the municipality, not the e-sports team. This is why the host-city map tracks municipal investment more than audience demographics, and why municipal policy is a leading indicator of where infrastructure will cluster.

What to remember about e-sports in China

- The e-sports industry collected RMB 29 billion in 2025. Meanwhile, the wider ecosystem (including in-game purchases and sponsorships) was measured at RMB 179 billion in 2024. Most of the money is users paying inside the games, not income reaching the operators.

- The 495 million-strong audience has plateaued, so the market is monetizing existing users harder while the viewer base ages upward.

- A two-track government that simultaneously promotes the industry and restricts youth gaming. Paired with city-level industrial policy, it shapes the market in ways no Western framework predicts.

- Tencent develops the games, runs the leagues, and owns the broadcast pipeline. The result is a single point of dependency where the partner, the gatekeeper, and the rival are often the same firm.

- Geography is policy. Audience matters, but among China’s largest cities, it is municipal investment that decides where the industry actually locates.