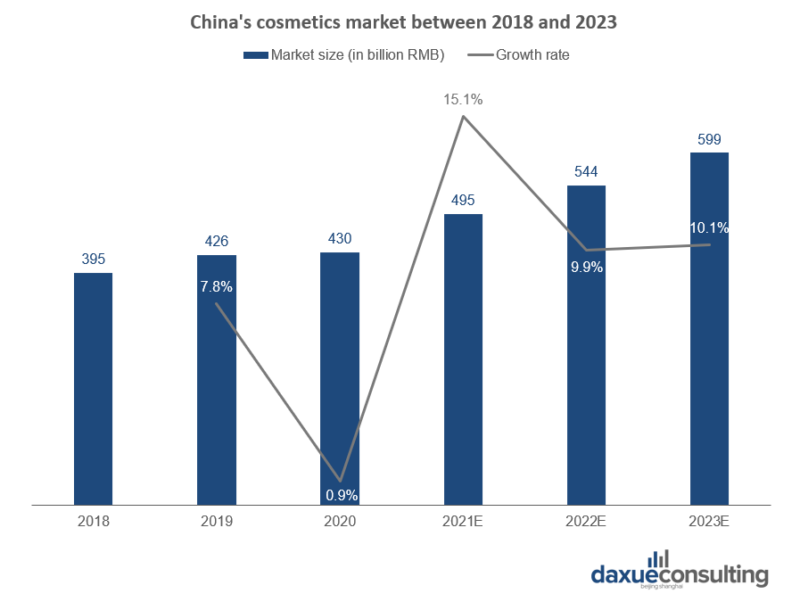

China’s cosmetic market has not stopped growing in recent years and it is estimated to generate about 495 billion RMB in 2021, vaunting a 15.1% increase from 2020. Nevertheless, China’s per capita consumption of skincare and makeup products is just 1/3 and 1/5 of that boasted by the US and Japan/South Korea respectively, showing a huge potential for further growth. Moreover, the improvement of beauty knowledge, along with their greater familiarity with cosmetics, is leading to a diversification and an upgrading of Chinese consumers’ demand in beauty products. Meanwhile, big international names are bound to suffer greater and greater competition from domestic brands. According to iResearch, Chinese cosmetics brands are expected to experience a higher growth than the overall sector, boasting a compound annual growth rate of 16.6% by 2023.

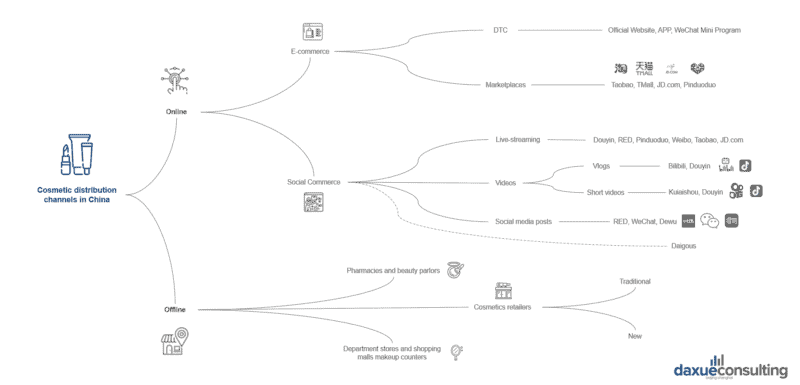

Main cosmetics distribution channels in China

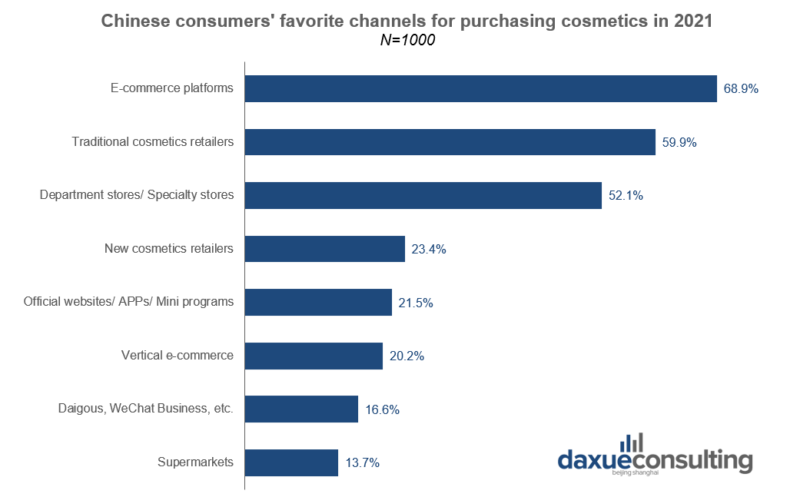

Although online channels are imposing themselves as main source of revenues for brands operating in China’s cosmetics market, brick-and-mortar stores are still among Chinese consumers’ favorite choices when it comes to purchase beauty products and rank within the top 3 sources of pre-purchase information for Chinese young cosmetics customers in 2021. Even for digitally savvy Chinese Gen-Z, offline cosmetics distribution channels in China were the second most utilized means through which purchasing skincare and beauty products during 2020, followed by short-videos platforms and brands’ owned channels.

Selling beauty products on China’s major marketplaces

The amazing success of Singles Day 2021 highlighted the great role acquired by e-commerce sales in China’s domestic market. With their tremendous amount of Monthly Active Users (MAUs) and the impressive reach and power of their marketing tools, Chinese major marketplaces such as Taobao, TMall, JD.com, and Pinduoduo have all it takes to give an impressive boost to beauty brands sales.

Taobao and TMall

Founded in 2003, Taobao was China’s largest marketplace in terms of Gross Merchandise Value (GMV) in 2019 and recorded about 674 million annual active consumers during that period. Its low entry barriers and easy-to-operate interface make Taobao especially suitable for small and medium-sized cosmetics retailers. Nonetheless, its strength is also its weakness since its loose requirements and lacking quality checks fostered the proliferation of counterfeit goods.

Unlike Taobao, only legal business entities can open a flagship store on TMall. Its database is integrated with Taobao, thereby allowing Chinese consumers in search for secure shopping to filter items by its presence on TMall. Currently over 250 beauty brands run their official store on the platform, including L’Oréal, Beiersdorf and Shiseido. In addition, through TMall Heybox, the Alibaba affiliate company helps brands to create buzz around their new launches and catch Gen-Z novelty-loving consumers’ attention. The platform announced last year planning to support 1,000 new beauty brands to surpass 10 million RMB in annual revenues.

JD.com

Boasting over 471.9 million annual active customers in 2020, JD.com can be considered TMall’s main competitor. Partly owned by Tencent, the Beijing-based e-commerce giant invested heavily in AI and hi-tech tools, and it is able to grant its customers a delivery within 24 hours. In 2021, LVMH-owned brands Benefit Cosmetics and MAKE UP FOR EVER chose this platform for launching their flagship store precisely because of JD.com’s all-stops covered delivery operations and service, which will allow shoppers to choose the delivery option that fits the most to their needs.

Pinduoduo

Founded in 2015, the team-buying APP Pinduoduo generated 2 billion USD in 2020 and received about 100 million orders per day. In 2018, approximately 65% of its user base resided in low tier cities and 70% of them were female. In 2019, the platform launched an initiative aimed at promoting 50 new local small and medium-sized cosmetics enterprises by sharing resources and lowering R&D-related cost.

Perks and flaws of the DTC model

Direct To Consumers (DTC) refers to a business model where the manufacturer deals directly with the end consumer, bypassing any intermediary. Beyond granting brand independence, this model allows companies to react faster and get access to a great amount of data. Nevertheless, on the long run, DTC is universal and easily replicable, thus businesses need to develop a strong branding strategy as well as wisely utilize customer data to improve product positioning and complementary services. Chinese local beauty brands closed 2020 with 87.9 billion RMB in DTC sales, of which 8.4 billion RMB generated on WeChat.

Social commerce is key among cosmetics distribution channels in China

Brands are more and more willing to invest on social media platforms, as they have converted into key tools in marketing campaign in China. On average, brands spend about 57% of their budget on social media marketing, while both start-ups and well-established companies bet on KOLs’ recommendations.

Blogging APPs: WeChat, Xiaohongshu and Dewu

Beyond putting at their disposal its super versatile Mini programs, WeChat allows brands to create official accounts where sharing content and directly communicate with consumers through private traffic pools. With its about 1.2 billion MAUs in 2020 Q3, this multi-purpose APP provides businesses with a tremendous reach and deep penetration within Chinese audience.

Xiaohongshu, also known as RED, is a social commerce especially popular among young female consumers living in higher tier cities. Beauty, fashion and food are the hot topics on this platform. Since users tend to consider recommendations on this social media more reliable than traditional ads, Xiaohongshu reveals as the perfect place where triggering word-of-mouth and increase brand awareness, especially for smaller or less renown brands. The platform has its own e-commerce section, called RED Welfare Club.

Dewu is both a C2C and B2C marketplace where users can share pictures and impressions on their purchases, thereby fostering a strong sense of community. On this platform, consumers can purchase brand new as well as pre-owned items in a much safer way than on Taobao thanks to the APP’s anticounterfeiting efforts and its strict authentication measures. Along with Xiahongshu, Dewu is one of the most beloved platforms by Gen-Z consumers: during 2021 Q1, this resale APP vaunted a year-on-year growth of 96% in members under 24.

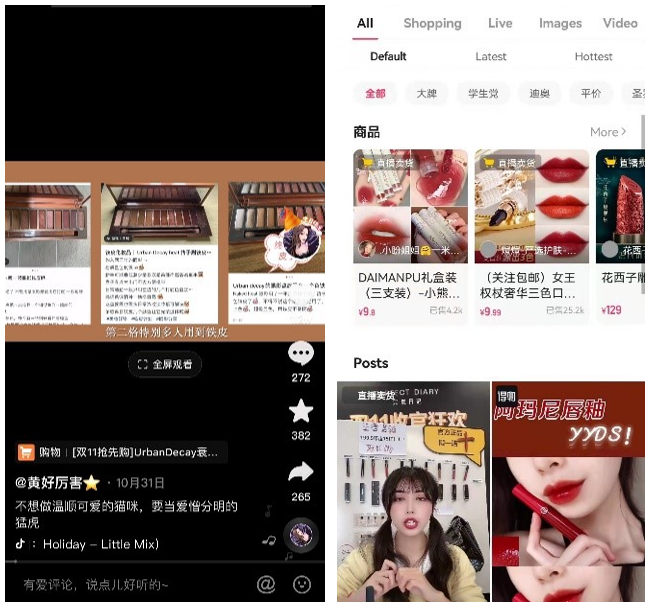

Short-video platforms: Douyin and Kuaishou

Boasting a large and young user base, the two short-video platforms are an ideal place where sharing user-generated content and gain a lot of exposure. Douyin tends to give more emphasis on quality content and vaunts a higher engagement rate, instead, Kuaishou values more authenticity and everyday life-related content. In terms of user groups, Douyin has more female users than males, whereas Kuaishou has more male users. Moreover, even though most of the two platforms’ users reside in third- and fourth-tier cities, Douyin is stronger than Kuaishou in first- and second-tier cities. In both cases, people can purchase cosmetics directly in-app or through links rerouting to JD.com or Taobao.

Gen-Z’s beloved medium-long video APP Bilibili

Bilibili is one of the fastest-growing and best-performing video-sharing community platforms in China. Like Kuaishou, male consumers hold the lion share of its consumer base, but Bilibili users are usually younger than Douyin’s and Kuaishou’s ones. Indeed, the platform’s algorithm is conducive to the creation of niche communities of kindred spirits, thereby satisfying Chinese Gen-Z consumers’ need to express their uniqueness while being part of a group. By allowing creators to upload longer videos, Bilibili is more suitable for storytelling aimed at establishing sounder emotional ties with customers and communicate brand values. According to its Q3 2020 corporate financial presentation, lifestyle topics, such as vlogging, beauty and fashion were its most popular topics.

Lights and shadows of Chinese Daigous

Daigous are unofficial personal shoppers who help Chinese consumers to get their hands on exclusive or cheaper foreign luxury goods and beauty items. Their market has developed rapidly during last decade until hitting 260 billion RMB in 2018. However, such unconventional middlemen are now facing restrictions from the Chinese government. Daigous mainly operate through Taobao, WeChat, and cross-border e-commerce platforms. Brands can either benefit or get damaged by their operations. On the one hand, Daigous can target more precisely the right audience and get consumers’ feedback more quickly, while, on the other hand, fraudulent and unethical practices could deteriorate brand reputation as well as hamper the establishment of a sound customer relationship.

Special mention: Live streaming

While in the West live streaming is still associated with gaming and entertainment, in China it is a core shopping means. According to iResearch, live streaming is the fourth favorite channel where purchasing cosmetics in 2021. Indeed, during live streaming sessions, consumers can find bargain prices, limited-edition products, and coupons. Moreover, shoppers can directly interact with live streamers to get further details and clarify their doubts before taking their decision. As of May 2020, Taobao Live, Douyin and Kuaishou were China’s leading live streaming platforms, recording together a GMV of roughly 900 billion RMB.

Offline cosmetics distribution channels in China

Although the online channels hold the lion share of the domestic cosmetics market, offline cosmetics distribution channels in China provide a more comprehensive service and higher value-added for beauty consumers. In recent years, new domestic brands such as Perfect Diary and Judydoll have heavily invested in expanding their physical stores in order to enhance their brand image.

The rise of new cosmetics retailers in China

Despite ranking within top 3 most used cosmetics distribution channels in China, traditional retailers are facing the rise of a new class of multi-brand make-up stores, which are more capable to meet Chinese Gen-Z’s needs. China’s new cosmetics retailers are more open to niche brands and new brands than traditional ones, they usually pay more attention to the decoration and design of their premises, and sales assistants tend to be less pushy . Nevertheless, this class of new beauty products retailers have not built a strong brand loyalty yet and risk suffering a stiff competition in the long run since their business model is highly replicable.

The Colorist, Wow Color, Harmay and H.E.A.T. are some of the most popular new cosmetics retailers in China.

Pharmacies and beauty parlors offer unbeatable expertise and professionalism

Pharmacies and beauty parlors are usually specialized in high-end cosmetics complying with higher standards than the beauty products you can find in supermarkets and malls. That is the reason why they tend to offer a narrower array of items than other cosmetics distribution channels in China, but their quality is above the average. Moreover, the staff in pharmacies and beauty parlors can provide consumers with professional advice and recommend them the best products for sensitive skin types and allergy sufferers.

Make-up counters are alive and well

As Chinese demographic changes and household disposable income grows, young consumers are keener to spend more money at an earlier age. Chinese Gen-Z feel curious towards niche beauty brands and do not back down from purchasing luxury make-up goods. Department stores and shopping mall make-up counters are one of the main sources of skincare and beauty information for Chinese Gen-Z and, unlike they used to do in the past, they tend now to bet more on high-end products rather than on entry-level ones.

What to know about cosmetics channels in China

- Despite the Covid-19 pandemic, China’s beauty market kept growing and it is expected to generate about 495 billion RMB by the end of 2021.

- Even though now online channels hold the lion share of total sales, physical stores are still a key cosmetics distribution channel in China.

- Online channels can be classified into “e-commerce channels,” including both marketplaces and DTC platforms, and “social commerce,” composed by a rich ecosystem of social media apps which meet different needs and respond to distinct purposes.

- Offline cosmetics distribution channels in China are instead marked by the rising competition between traditional and new multi-brand make-up stores. The latter stand out for targeting a younger consumer base, adopting a more daring approach in their brand selection, and paying more attention to the interior design of their premises.

- Department stores and shopping malls remain a major source of beauty and skincare information for Chinese Gen-Z consumers, whereas pharmacies and beauty parlors specialize in providing high-standard cosmetics and professional advice.